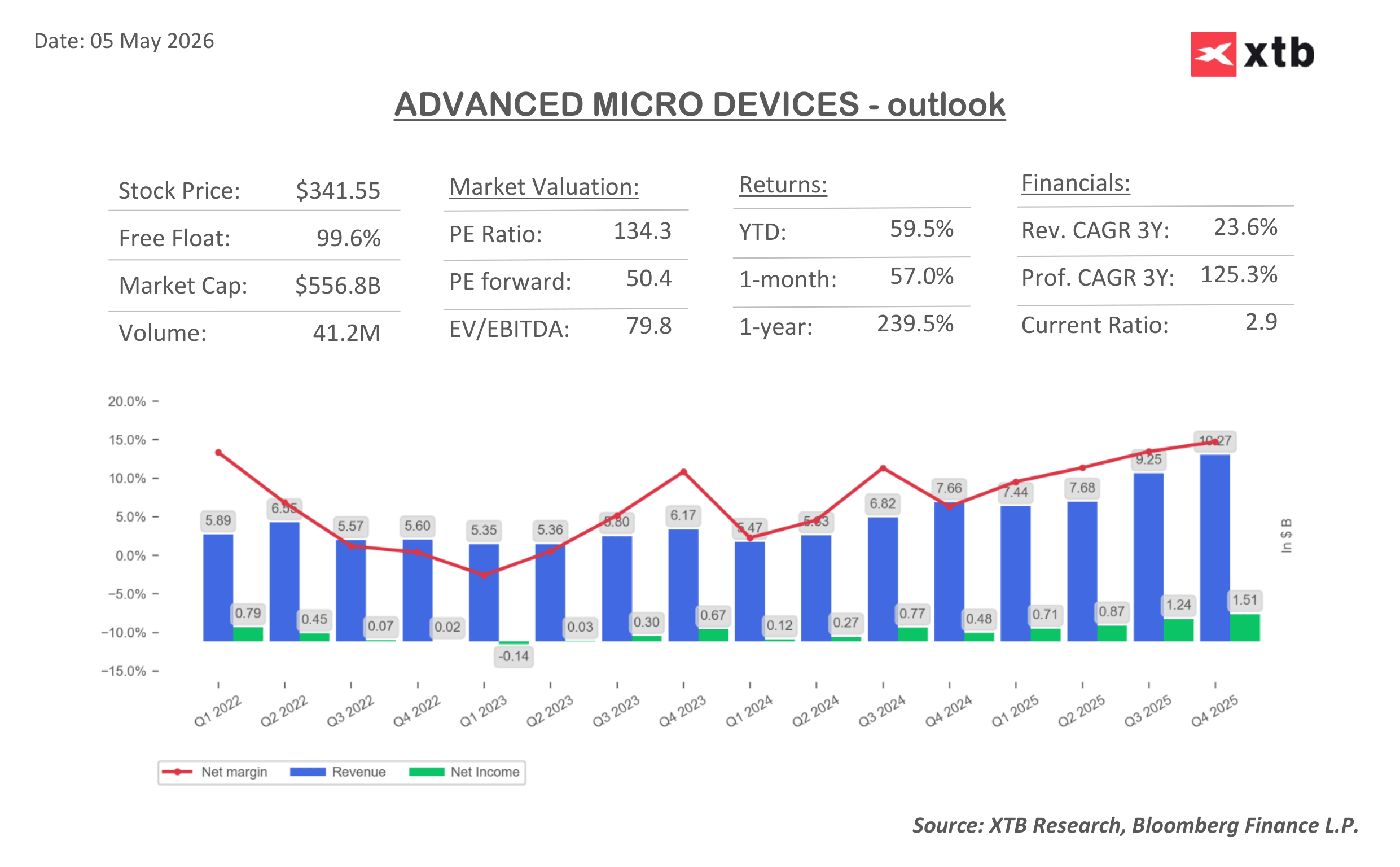

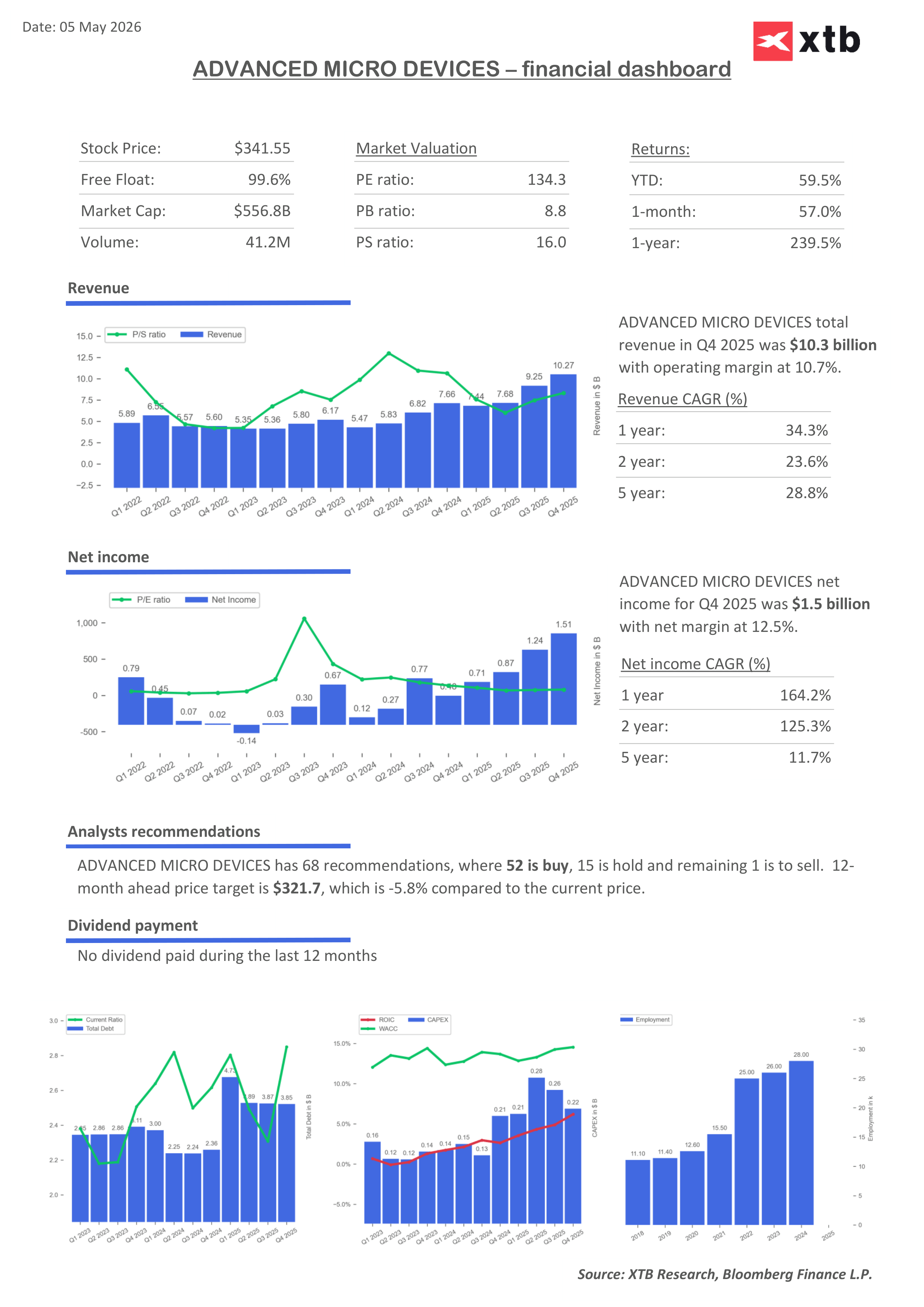

Advanced Micro Devices enters its Q1 2026 earnings release at a point where the company is increasingly navigating a more demanding phase of the investment cycle. On one hand, it is benefiting from one of the strongest demand impulses in history in AI-driven computing infrastructure. On the other hand, it is under pressure to demonstrate that it can translate this demand into durable and scalable market share in the highest value-added segments.

The market no longer views Advanced Micro Devices purely as a traditional semiconductor manufacturer whose performance is driven by the PC or server cycle. Instead, the company has been absorbed into a broader narrative around the global artificial intelligence race, where data center infrastructure and the ability to supply computing power to the largest technology platforms have become the key drivers. As a result, each earnings report is now less an assessment of historical performance and more a test of whether AMD is strengthening its position in the most strategic part of the AI market.

In such an environment, even solid financial results do not guarantee a positive market reaction if they are not accompanied by an improvement in the quality of revenue composition. Investors are increasingly distinguishing between growth driven by cyclical recovery and growth resulting from a genuine shift in AI market share. This distinction has become a central component of the company’s valuation.

Q1 2026 Market Expectations

-

Revenue: 10 billion dollars

-

Earnings per share (EPS): 1.28 dollars

-

Data center segment: 5.61 billion dollars

-

Gaming segment: 668 million dollars

-

Client segment: 2.73 billion dollars

-

Embedded segment: 868 million dollars

-

Gross margin: 55.1%

-

R&D expenses: 2.26 billion dollars

-

Capital expenditures (CapEx): approximately 215 million dollars

The consensus points to a relatively stable quarter with moderate growth. However, in the current macro and sector environment, it is not the pace of growth that matters most, but its internal composition. Once again, the primary focus is on the data center segment, which has become the core driver of the investment narrative and the main source of potential re-rating.

Data Center and AI as the Main Growth Engine

The data center segment remains the central pillar of AMD’s investment story. It is here that the market is trying to determine whether the company is genuinely increasing its share in the most valuable part of the AI market or remains primarily a secondary beneficiary of the broader infrastructure investment cycle.

The pace of adoption of the Instinct platform and the scalability of its deployment in a highly competitive environment are key variables. At the same time, the EPYC server CPU business continues to play an important stabilizing role, although its importance is increasingly seen as foundational rather than the primary driver of future growth.

In this context, a key question is whether AMD is moving into the most value-dense layers of the AI market, including large-scale model training and high-margin inference workloads, or whether it remains positioned more as a second-tier infrastructure provider.

CPUs as a Stabilizing Factor

CPU products continue to serve as a stabilizer for results, benefiting from rising investment in server infrastructure and a partial recovery in enterprise demand. This segment provides predictability and a revenue base, but it is no longer the primary source of re-rating for the company.

Increasingly, artificial intelligence is becoming the dominant growth vector and the key driver of valuation. At the same time, the PC segment remains under cyclical and structural pressure, partly due to constraints in the memory supply chain, which redirect production capacity toward AI infrastructure at the expense of traditional applications.

Hyperscaler CapEx as the Cycle Backbone

The entire cycle remains heavily dependent on capital expenditures from the largest technology companies, which act as the leading indicator for demand in computing infrastructure. Sustained high levels of data center investment create a favorable demand environment, but at the same time intensify competition for allocation within those budgets.

In practice, this means AMD operates in an environment of structurally strong demand, but not automatically rising market share. This gap has become one of the main sources of volatility in the investment narrative.

Quality of Growth as the Key Metric

In the current market regime, the importance of growth itself is diminishing, while the focus on its source and durability is increasing. Investors are not only analyzing the pace of expansion, but also how much of it comes from genuine gains in AI-related segments versus cyclical rebounds in more traditional businesses.

As a result, AMD is increasingly being valued not as a pure growth company in the traditional sense, but as a participant in a structural race to define the architecture of future computing infrastructure.

Key Takeaways

-

AMD is in a transitional phase where AI-driven growth must be converted into durable market share rather than remaining a cyclical boost

-

The data center and AI segments are becoming the primary source of potential valuation re-rating, while CPUs act as a stabilizing factor

-

The key question is no longer the pace of growth, but its quality and exposure to the most valuable parts of the AI ecosystem

-

Hyperscaler CapEx remains the main demand catalyst, but it does not guarantee proportional market share gains for AMD

-

The PC segment remains under structural pressure and has limited relevance for the company’s current investment narrative

-

The main sensitivity for the market lies in whether AMD is truly moving up the AI value chain or simply benefiting from its overall expansion

Space stocks surge as Wall Street awaits SpaceX IPO 📈

US Open: Wall Street continue to rise despite US - Iran tensions 📈 Micron Technology rises 10%

Nvidia challenges Intel and AMD in the CPU market

Market Wrap: European stocks heading south ⬇️What’s driving the markets today❓

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.