Apple Inc. is entering its Q2 2026 earnings at a point where the market no longer values the company purely as a stable hardware-and-services business, but increasingly views it as a lagging participant in the global artificial intelligence cycle. This fundamentally changes how results are interpreted, as the focus shifts from the question of “is Apple delivering” to whether “Apple is returning to a phase of innovation-driven growth.”

At the same time, this quarter is also transitional from a product and strategic cycle perspective. Apple is operating between its traditional model built around the iPhone and services, and a new growth architecture that is gradually being built around AI, refreshed hardware, and potential new device categories.

Key market expectations for Q2 2026

-

Revenue around 109.7 billion USD

-

EPS around 1.96 USD

-

iPhone around 57 billion USD

-

Mac around 8.1 billion USD, supported by a new product cycle

-

Services around 30.4 billion USD, a stable high-margin segment

-

China around 18.9 billion USD, a key demand-sensitive region

-

Margins supported by product mix, but under pressure from memory costs

-

CapEx moderate, but gradually increasing due to AI and hardware investment

Market expectations and positioning

The market is pricing in another solid quarter of growth driven by a new product cycle, where the key contributors are the iPhone 17e, refreshed Mac lineup, and new iPads. The MacBook Neo is particularly important as it pushes Apple further into a more mass-market price segment and may expand volumes beyond the traditional premium core.

At the same time, investors assume the company remains partially exposed to memory cost pressures, which could limit margin expansion despite a favorable product mix.

Against this backdrop, the market is no longer evaluating Apple purely on a beat-or-miss basis, but increasingly on the quality and durability of its product cycle.

AI as the missing element of the growth narrative

Artificial intelligence remains a central but still incomplete part of Apple’s story. The company is gradually introducing AI features into iOS and its broader ecosystem, but the market still views these developments as incremental improvements rather than a fundamental shift in how the company operates.

In practice, AI is currently seen as a potential driver of higher device upgrades, a factor that strengthens ecosystem stickiness, and a foundation for future product categories such as wearables, smart home devices, and fully AI-driven hardware. However, there is still no clear evidence that AI is directly generating a new layer of revenue monetization.

Memory costs and margin pressure

A key short-term factor remains pressure in the supply chain, particularly in memory components. Unlike in previous cycles, this is no longer a secondary issue, as it is beginning to affect both product pricing and production capacity.

This means that even with stable demand, Apple may face limitations in further expanding gross margins, which increases the importance of product mix and the Services segment as a stabilizing profit buffer.

Services as a stabilizer, not the main re-rating driver

The Services segment remains one of the most important components of Apple’s business model, generating high-margin and recurring cash flows. However, its role in the current cycle is more stabilizing than growth-driving.

Unlike in previous years, Services is no longer the primary driver of valuation re-rating. Instead, the key factors now are the hardware cycle, artificial intelligence, and potential entry into new product categories.

Management transformation and strategic regime shift

An additional key element is the change in leadership structure, with John Ternus taking over as CEO while Tim Cook transitions to the role of chairman.

John Ternus is viewed as a more product- and engineering-focused leader, which the market interprets as a potential shift toward faster product decisions and a higher willingness to take technological risks. Tim Cook, meanwhile, remains a stabilizing force in operational and geopolitical areas, reducing the risk of abrupt strategic shifts.

High expectations and limited room for error

Apple is currently one of the most fully priced companies among large-cap technology stocks, meaning the market is no longer pricing in stability alone, but rather a renewed acceleration in growth.

As a result, even solid earnings may fail to generate a lasting positive reaction unless they are supported by a clear shift in the forward-looking narrative. The key areas of market sensitivity include the durability of the iPhone and Mac cycle, the impact of memory costs on margins, and the pace of AI integration and monetization.

Key takeaways

-

Apple is in a phase where maintaining growth is no longer sufficient, and a re-acceleration is required

-

The product cycle, including iPhone 17e and MacBook Neo, supports results but does not yet reshape the long-term growth structure

-

Artificial intelligence remains the most important missing element of the investment narrative

-

Memory cost pressure limits further margin expansion

-

The market expects Apple not only to remain stable, but to re-establish its ability to deliver high-quality growth rather than just steady performance

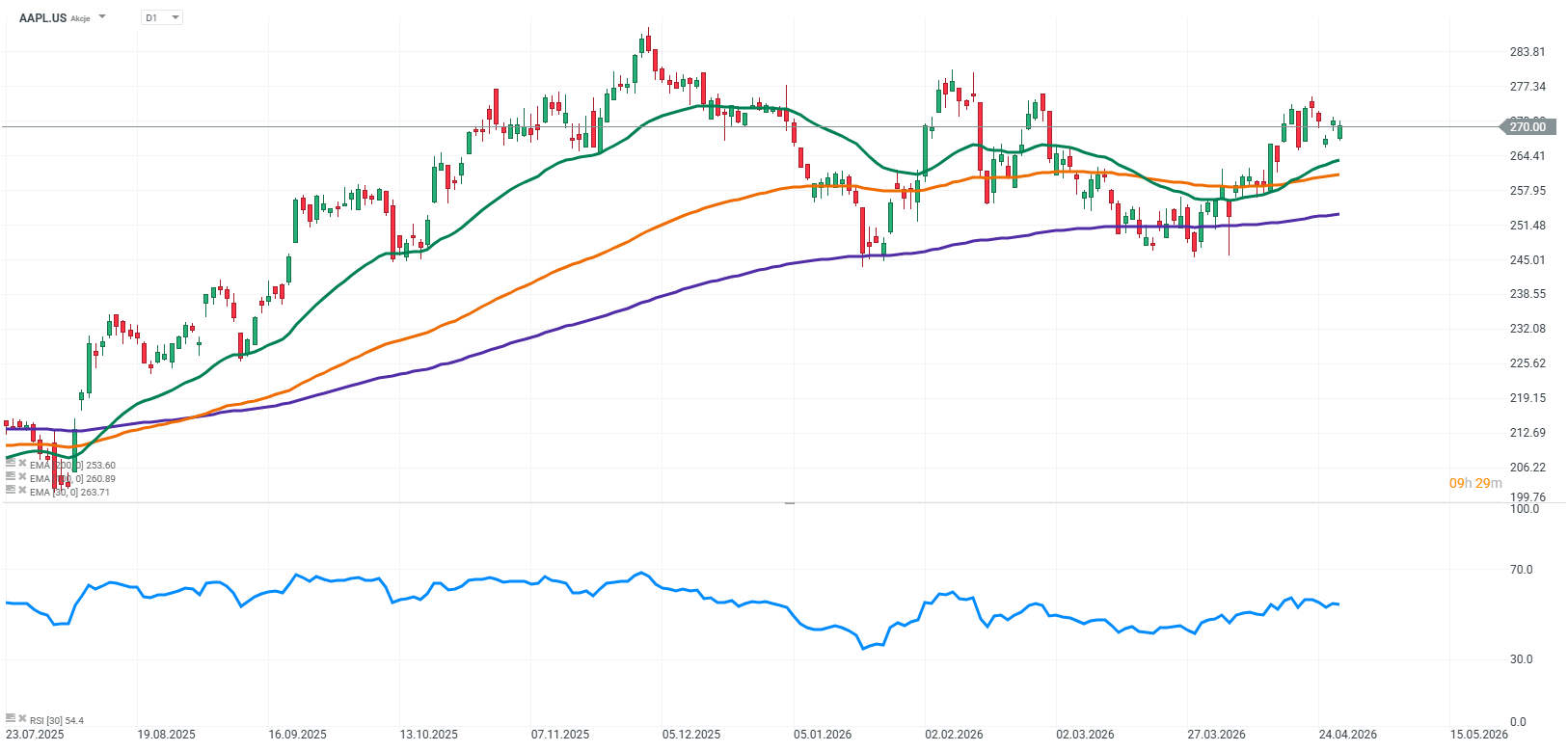

Source: xStation5

Market wrap: ASML and Infineon support sentiments in Europe

PDD shares plunge over 7% following earnings report⏰

Nvidia and 150 Billion Reasons Why Taiwan Is Becoming the Center of the AI World

Space stocks surge as Wall Street awaits SpaceX IPO 📈

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.