- AUD and NZD gain the most against other G10 currencies.

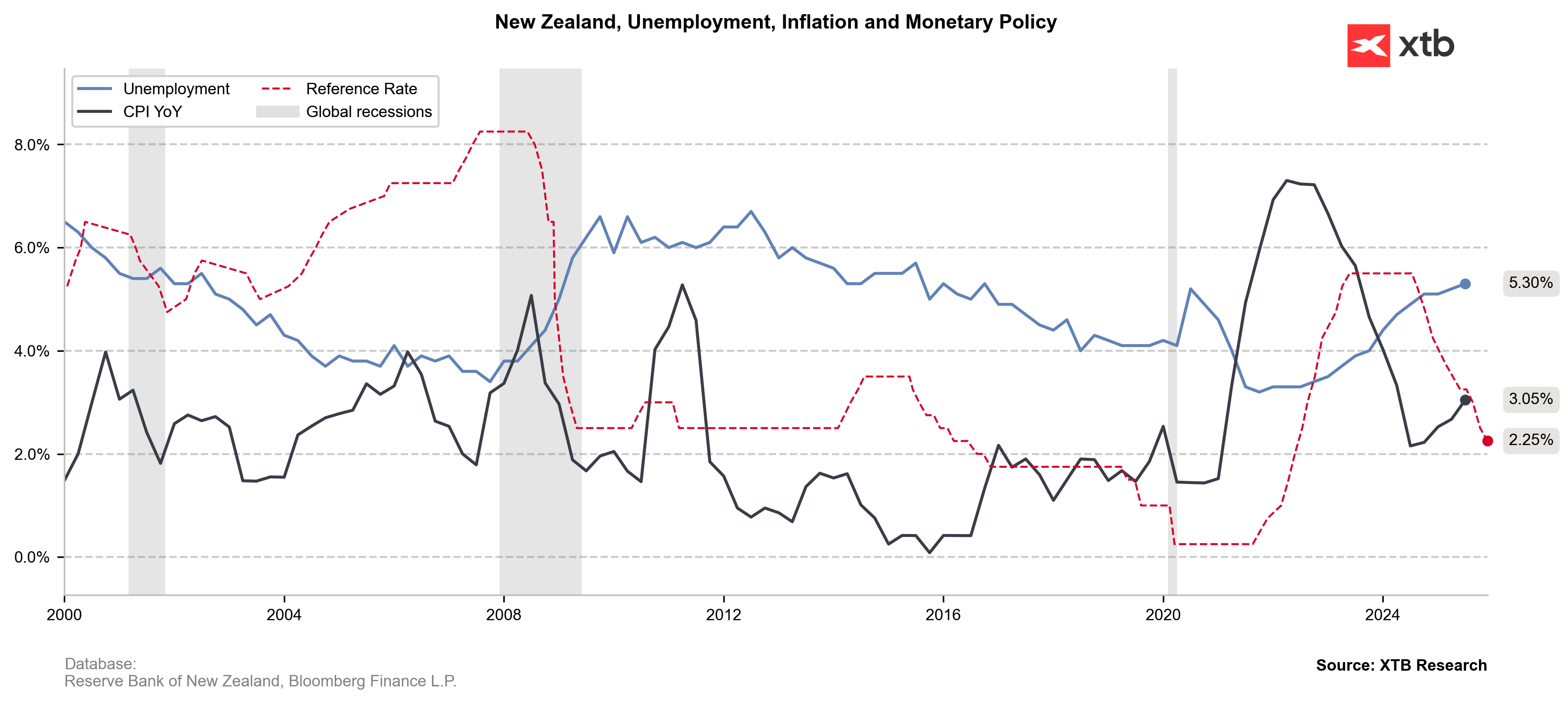

- RBNZ lowered its Official Cash Rate to 2.25%, with lower inflation estimates suggesting the end of an easing cycle.

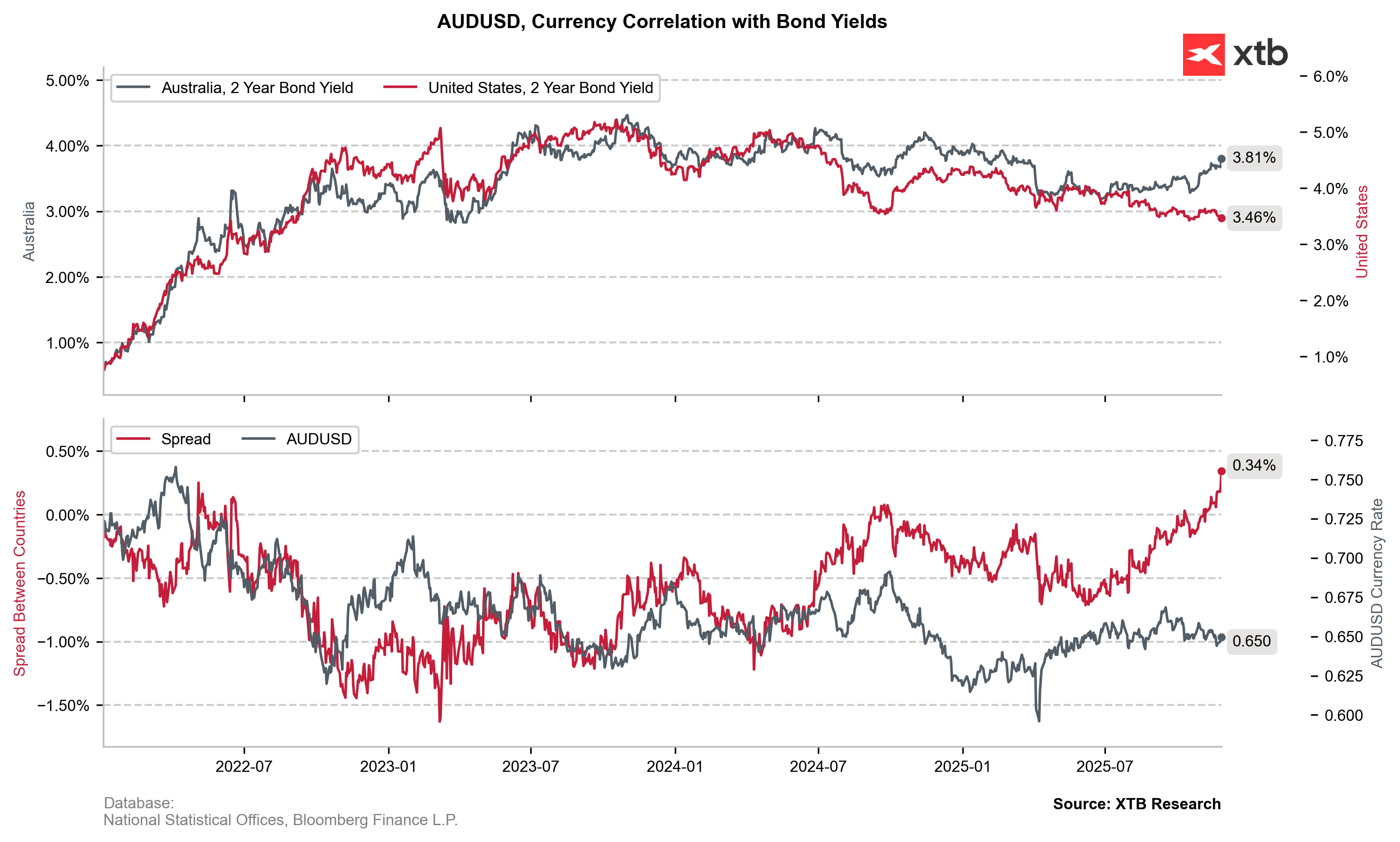

- Australia's CPI surprised again on the upside, delaying RBA rate cut prospects.

- AUD and NZD gain the most against other G10 currencies.

- RBNZ lowered its Official Cash Rate to 2.25%, with lower inflation estimates suggesting the end of an easing cycle.

- Australia's CPI surprised again on the upside, delaying RBA rate cut prospects.

Antipodean currencies are dominating today’s FX session in response to new monetary policy prospects in the region. Central banks in Australia and New Zealand are facing very different inflation dynamics, yet the latest Australian CPI data together with the tone of the Reserve Bank of New Zealand’s (RBNZ) decision have reinforced hawkish expectations in both economies.

The NZD is leading gains across the G10 today, strengthening by around 1% against the dollar and the euro despite today’s interest-rate cut in New Zealand, which lowered the Official Cash Rate to 2.25%, its lowest level in more than three years. The AUD is also gaining—up 0.5% vs the dollar and 0.4% vs the euro—in reaction to another inflation print that exceeded expectations.

After breaking out from an almost eight-month low, the NZDUSD pair has moved above the 10-day EMA (yellow) and is currently testing the 30-day EMA (light purple). Despite the bullish momentum, the RSI remains neutral, leaving room for further upside amid shifting expectations toward the RBNZ. Source: xStation5

The easing cycle that began in August 2024 consistently pushed the kiwi dollar into a downward trend, which deepened in 2025 due to a pronounced economic slowdown. Although retail sales rebounded strongly in Q2 (+2.3% y/y), this was largely driven by base effects after declines from Q2 2022 to Q3 2024. The main concern has become unemployment, which is at its highest level since 2016 (5.3%) and is contributing to a rise in outward migration, especially among young people of working age.

Today’s rate cut in New Zealand was well priced in, but market expectations adjusted to the RBNZ’s revised inflation forecasts. The central bank projects inflation to return to around 2% by mid-2026, a meaningful relief compared to the latest 3% reading. Reduced concerns about meeting the inflation target (the 1–3% range) in the medium term, combined with Governor Hawkesby’s neutral tone (“all options on the table”), were interpreted as a potential end to aggressive easing—providing long-awaited support for the NZD.

Given the current level of CPI, the RBNZ appears to be acting pre-emptively to prevent further economic slowdown in New Zealand. Source: XTB Research

The gains in the AUD, meanwhile, stem from yet another stronger-than-expected monthly inflation reading. CPI unexpectedly accelerated from 3.6% to 3.8%, with the trimmed measure—which excludes the most volatile fuel and energy prices—rising from 3.2% to 3.3%. The RBA halted its easing cycle in August at 3.6%, suggesting that negative real rate combined with inflation running above the RBA’s projections further delay prospects of rate cuts in Australia.

The Australia–US 2-year yield spread is at its highest level since June 2022. Source: XTB Research

Daily summary: Nervous anticipation, SaaS sell-off and weak macro data

“SaaS-pocalypse” continued

Three Markets to Watch in the Week Ahead (10.04.2026)

US OPEN: The market calms down ahead of earnings season

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.