16:30 - EIA, change in U.S. oil inventories:

- Crude oil inventories: -8.26M (Expected: -3M; Previous: -7.23M)

- Gasoline inventories: -0.91M (Expected: -1.4M; Previous: +0.19M)

- Distillate inventories: +0.95M (Expected: -0.2M; Previous: -0.2M)

The release shows short-term growth impulse for oil. The key signal is the combination of a large drop in crude imports and very high refinery runs, which results in sharp decline in commercial inventories.

The U.S. reserve buffer is becoming critical at a time when the market is already pricing in the best possible scenarios regarding the Iran-U.S. conflict.

The sharp inventory draw is a combination of a steep fall in crude imports, down by 754k barrels per day, and strong refinery utilization: crude runs rose to 17.2M barrels per day, and refinery utilization reached 96.7%.

U.S. commercial crude inventories, excluding the Strategic Petroleum Reserve, fell by 8.3M barrels to 418.2M barrels, already about 6% below the five-year average.

- Gasoline inventories fell by 0.9M barrels and are also about 6% below the five-year average.

- Distillate inventories rose by 1.0M barrels, but remain as much as 13% below the five-year average.

- Total crude inventories including the SPR fell by 17.2M barrels, with the strategic reserve alone down by 8.9M barrels. Although the decline is large, most of it is not “market-driven.”

- The decline in commercial crude inventories is visible in two key regions: the Gulf Coast (down about 4.8M barrels) and the Midwest (down about 4.5M barrels).

The EIA also assumes that the Strait of Hormuz remains effectively closed in the short term, and tanker traffic only gradually returns from Q3 2026, while fuller normalization of production and flows may take until 2027. The agency also estimated very large global inventory declines in Q2 and Q3 2026, and a drop in OECD inventories to the lowest levels since 2003.

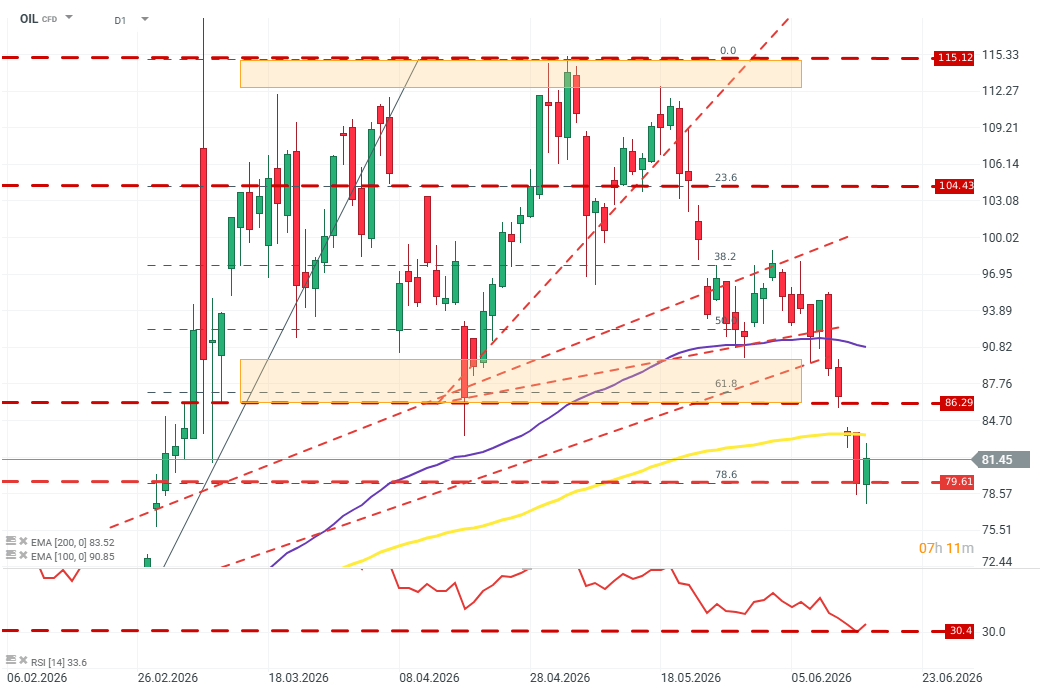

OIL (D1)

The RSI on oil contracts is currently in extreme overbought territory (around 30). Price bounced off the 78.6% Fibonacci level and may attempt to move back above the 200 EMA. If sellers shift into consolidation around these levels, the next target could be around $87. Source: xStation5.

📉 US100 loses 1.5%

EURUSD: Fed Pushback Keeps Dollar Supported Despite Softer Inflation Data

Economic calendar - Europe's Inflation and US Housing Market in Spotlight

Morninga Wrap: Wall Street Under Pressure. AI Loses Momentum, Netflix Disappoints, and the Persian Gulf Erupts

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.