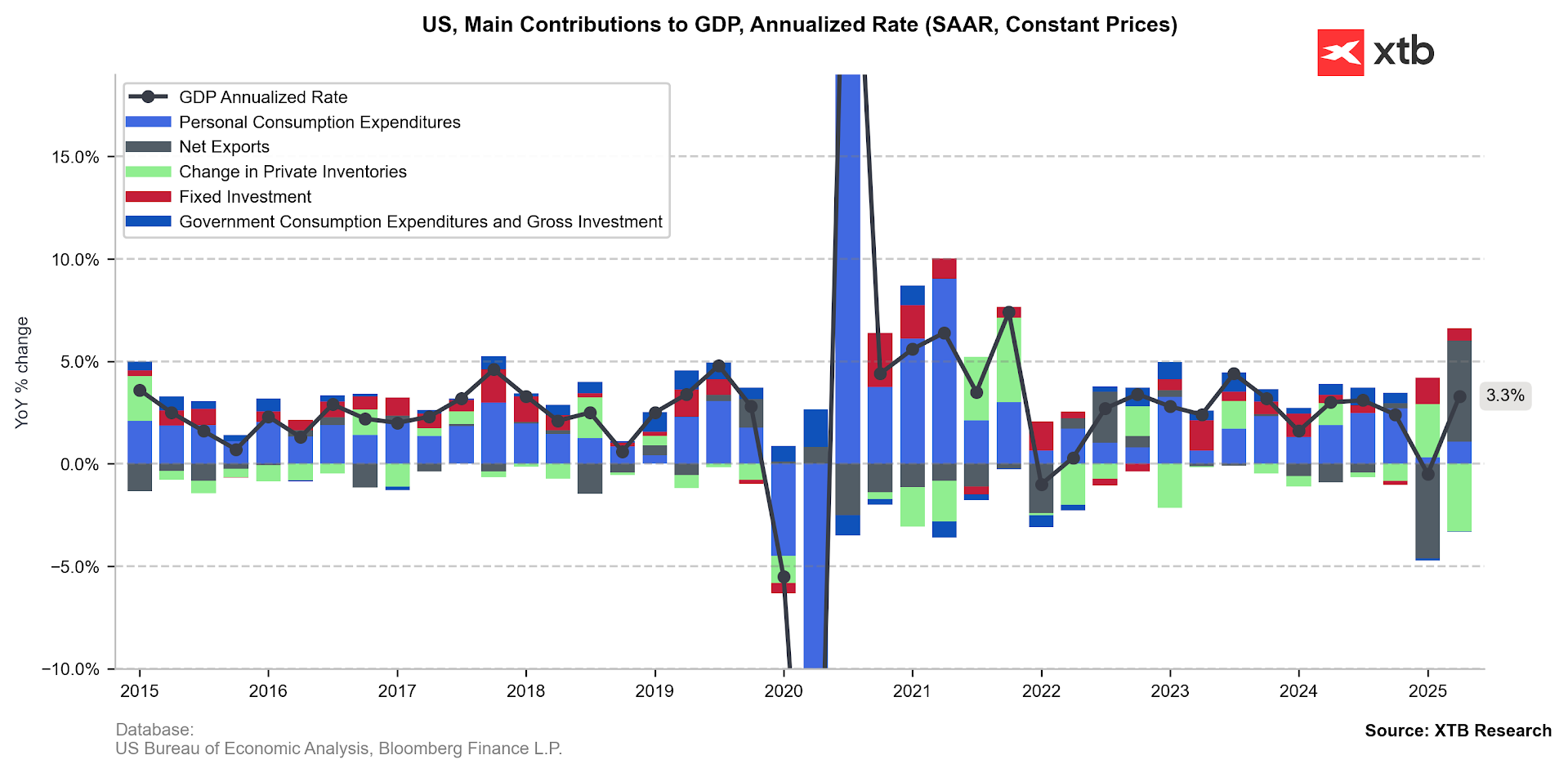

- Final Q2 GDP is revised up to 3.8% (expected: 3.3%; previous reading: 3.3%, Q1: -0.5%). Data was revised up mainly due to net exports that came out even better than in previous readings.

- GDP Price Index in Q2: 2.1% (expected 2.0%; previous: 2,0%, Q1: 3,8%).

- Core PCE Prices in Q2: 2.6% (expected: 2.5%; previous 2.5%, Q1: 3.5%)

- Initial Jobless Claims: 218k (expected: 233k; previous: 232k)

- Trade balance for August: -$85,5B (expected: -$95.7B; previous: -$103,6B)

- Durables Goods Orders for August: 2.9% MoM (expected: -0.3% MoM; previous: -2.7% Mom)

- Core Durables Goods Orders: 0.4% MoM (expected: -0.1% MoM; previous: 1.1% MoM)

Strong US Data Fuels Dollar Rally, Challenges Fed Rate Cut Outlook

A powerful set of US economic data was released, led by a significant upward revision to second-quarter GDP growth. The trade balance came in much better than expected, and initial jobless claims are returning to previous low levels, suggesting the spike from two weeks ago was a one-off event.

Furthermore, durable goods orders showed a strong rebound. While this was largely influenced by transportation orders, core orders also recovered, pointing to broader economic resilience.

Overall, the data paints a very positive picture of the US economy. The dollar strengthened considerably in response, now testing the 1.1700 level. This has also triggered a sharp pullback in US index futures, indicating the market is interpreting the data as hawkish. Given the economy's underlying strength, some members of the Federal Reserve may now question the justification for two interest rate cuts this year, especially since inflation continues to be a problem.

Growth is driven mainly by net exports but there is also a positive contribution from consumption and fixed investment, which indicates that even without tariffs turbulence, the change should be positive. Source: Bloomberg Finance LP, XTB

EURUSD has decreased significantly today due to strong data package from the USD which undermines probability of further Fed cuts this year. Source: xStation5

Market is not sure about future cuts from the Fed after very positive data from the US economy. US500 is below opening price after recent roll-over. Source: xStation5

Daily Summary: Trump's War Threats Weigh on Markets. Wall Street Sinks into the Red

Tensions around Iran weigh on markets!

US Open: Alphabet and Tesla Weigh on Wall Street, While Oil Prices Renew Investor Concerns

Wheat climbs to the highest level since May 2024 🚜 Black Sea export risks fuel rally

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.