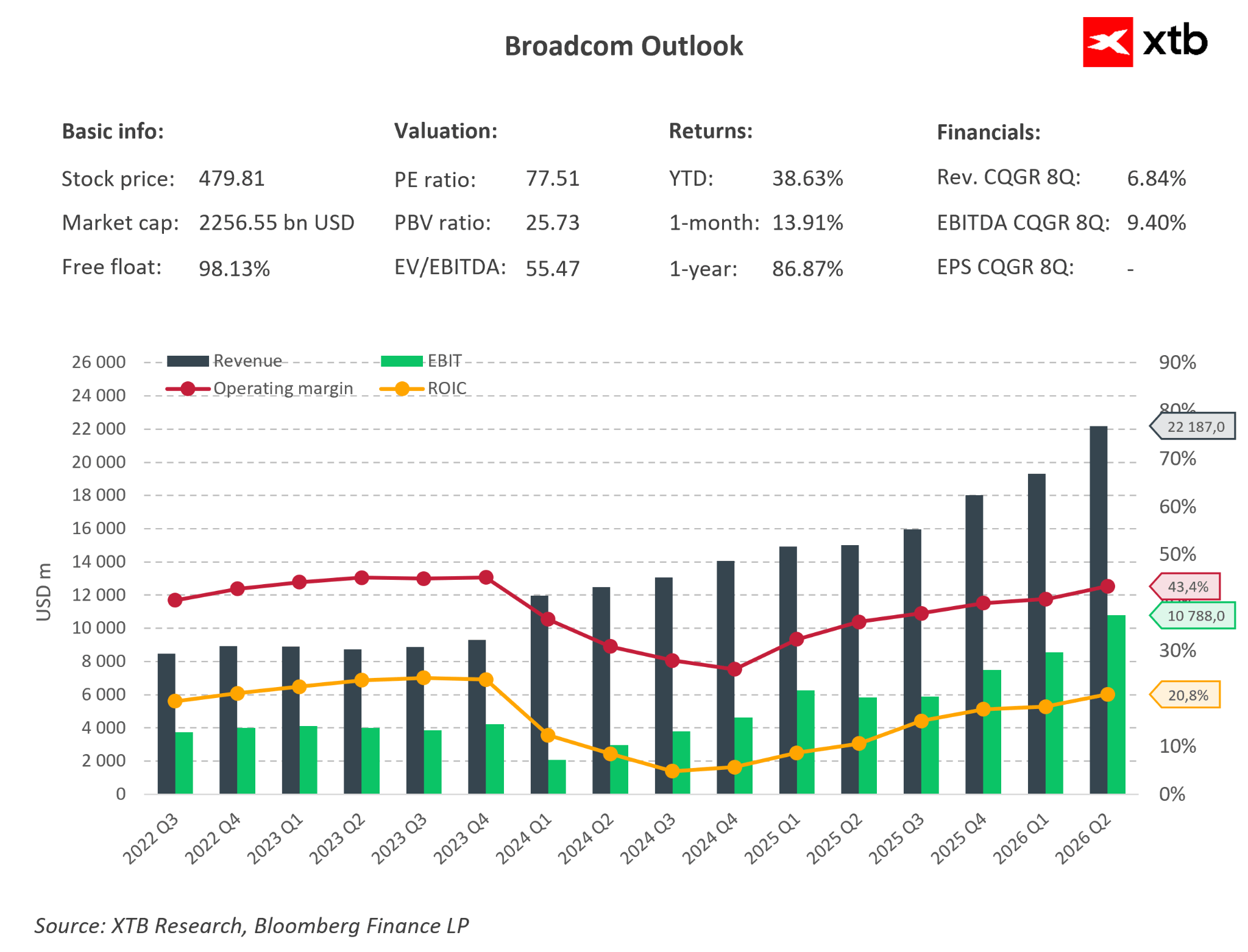

Strong financial results driven by AI

Broadcom reported very strong results for the second quarter of fiscal 2026, confirming that it remains one of the main beneficiaries of the boom in AI infrastructure. The company’s revenue rose 48% y/y to USD 22.19 billion, slightly above consensus, while adjusted EPS came in at USD 2.44 versus expectations of USD 2.40.

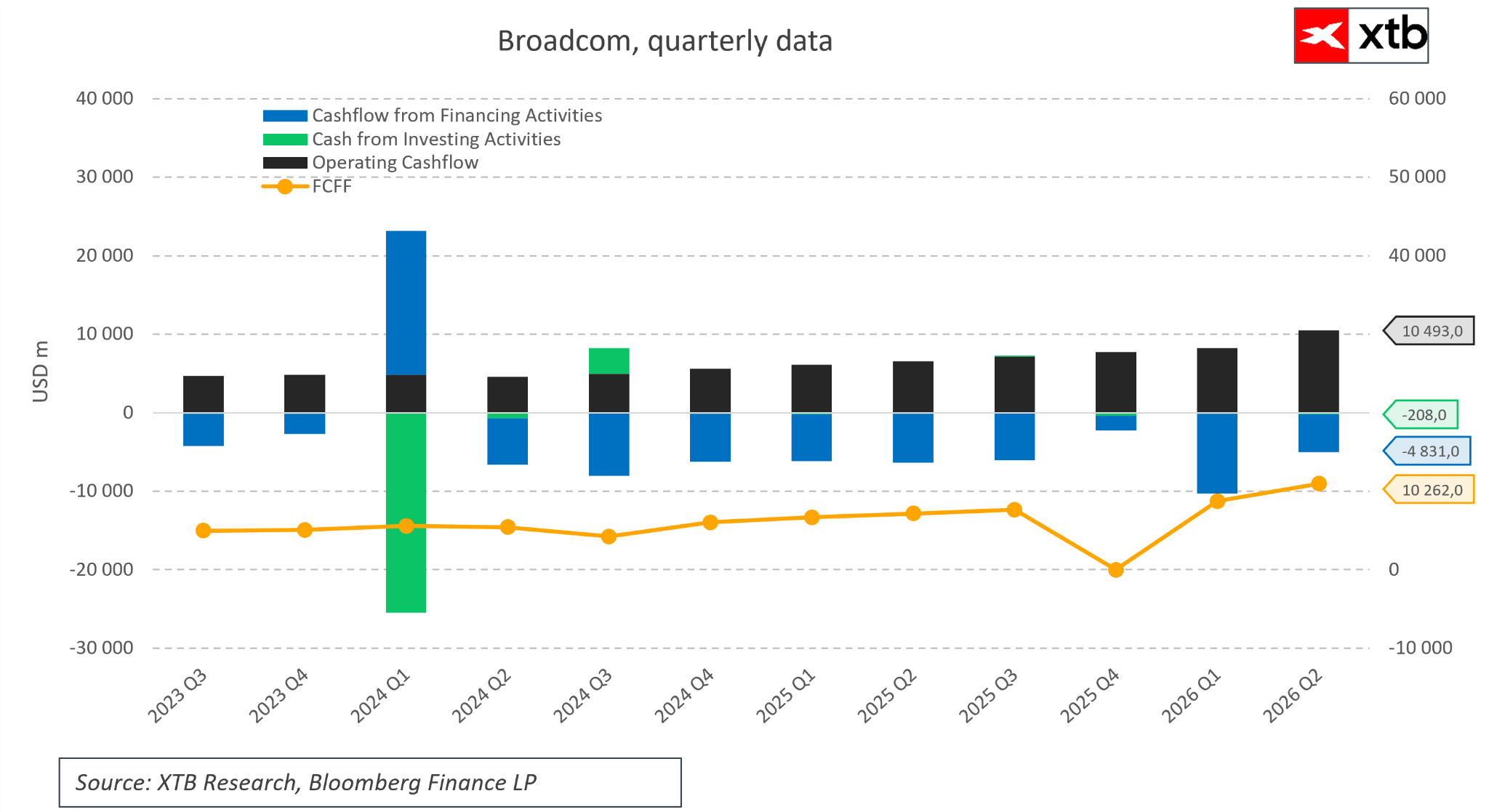

The cash flow side looked particularly strong: free cash flow increased 60% y/y to USD 10.26 billion, equivalent to as much as 46% of revenue. The key growth driver was the semiconductor segment, where revenue rose 79% y/y to USD 15.0 billion, including AI chip sales, which increased 143% y/y to a record USD 10.8 billion. The weaker point in the report was the infrastructure software segment, which grew 9% y/y to USD 7.18 billion, but came in slightly below unofficial, elevated market expectations.

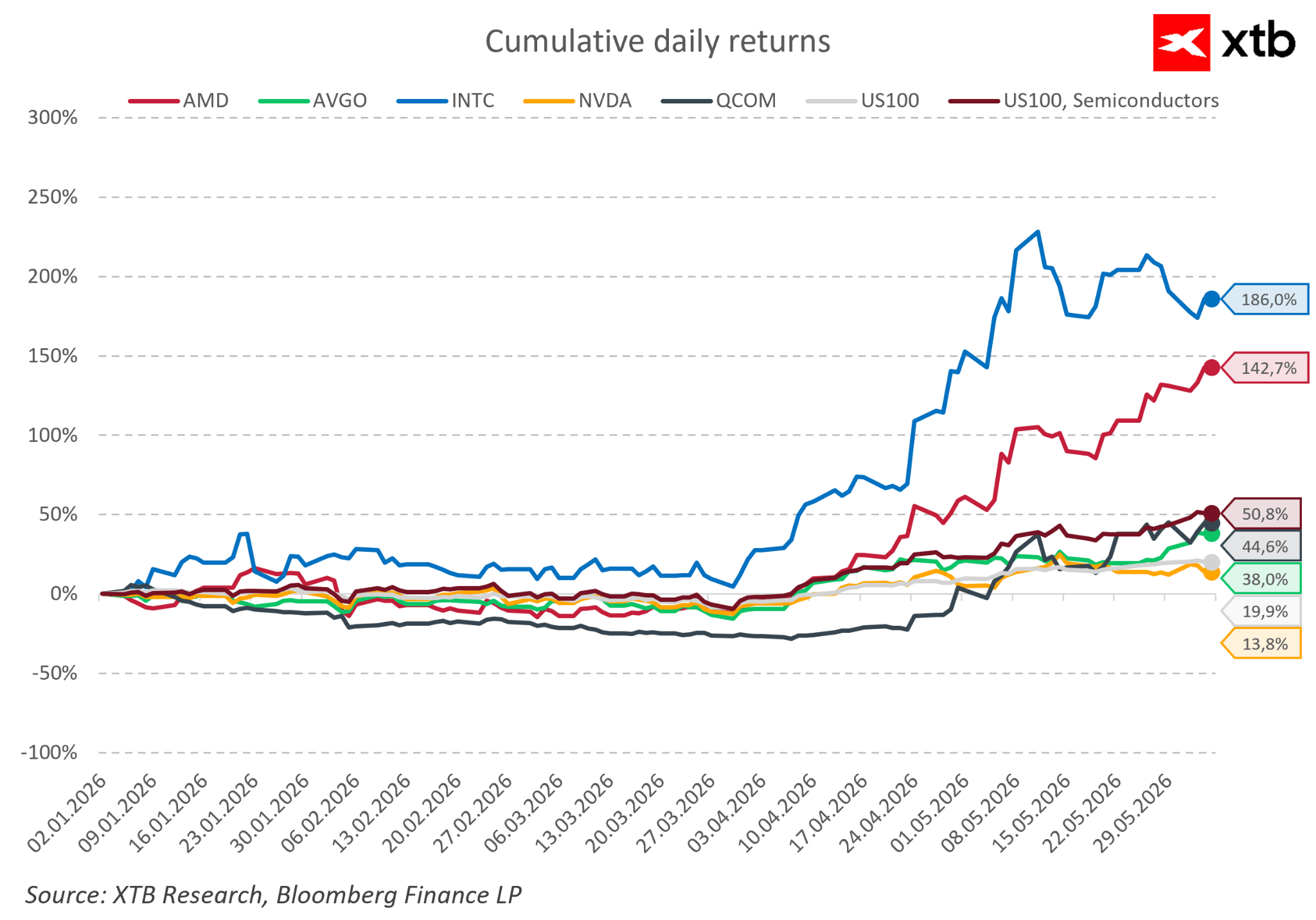

Broadcom compared with competitors

Compared with major semiconductor companies, Broadcom looks solid, although it is not the leader in year-to-date returns. Since the beginning of the year, AVGO shares have gained around 38%, although this figure does not yet include the nearly 13% decline in after-hours trading following the quarterly results. For comparison, the US100 has risen by around 20%.

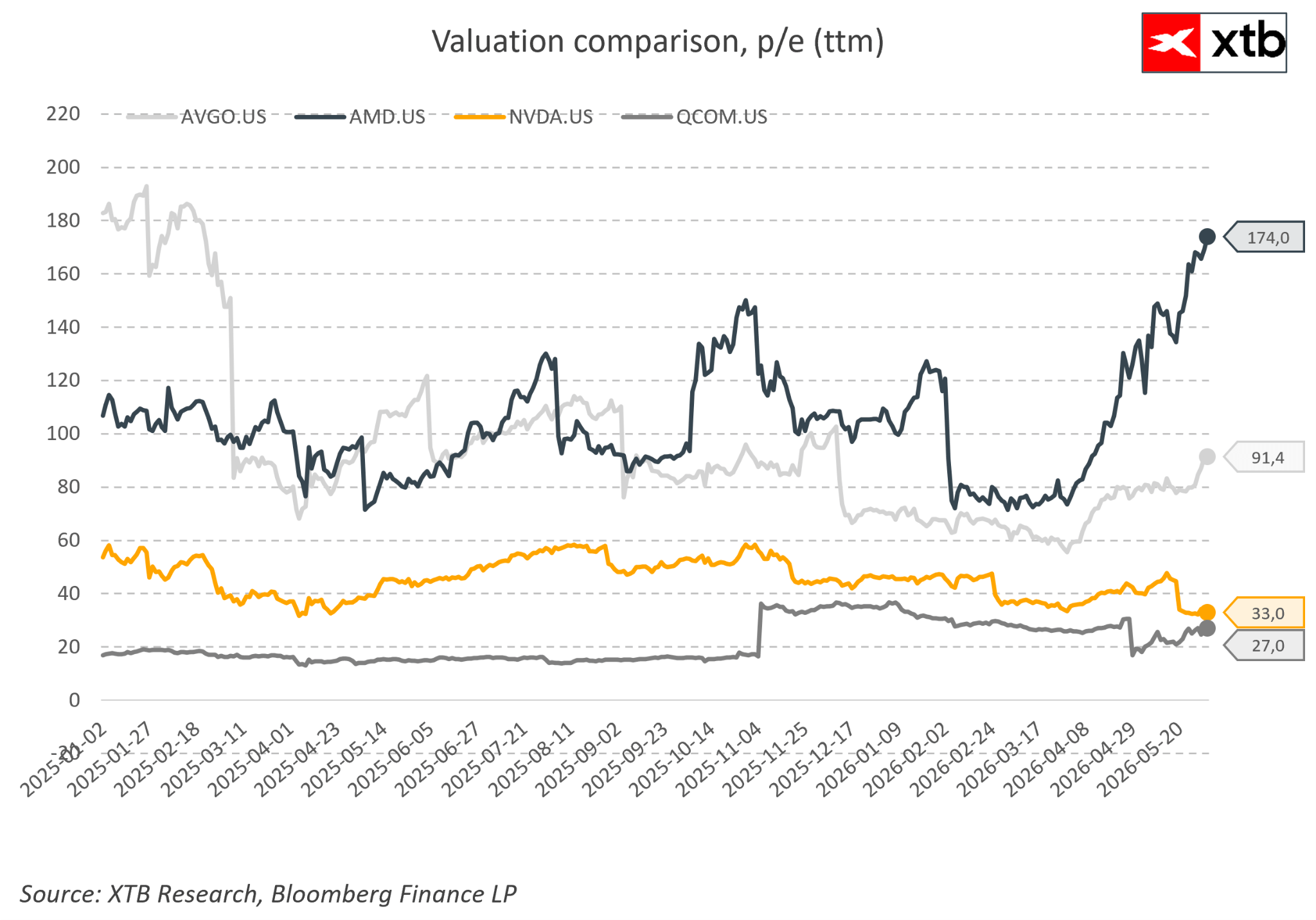

Broadcom’s valuation remains demanding

Broadcom trades at a clear premium to some of its competitors — AVGO’s TTM P/E ratio stands at around 91x, significantly higher than in the case of Nvidia and Qualcomm. AMD is the exception here. This is an important context for the reaction after the results: even a very strong financial report and high guidance may not be enough if the market had already priced in a very optimistic scenario beforehand.

Management highlights record demand for AI chips

Management’s commentary was clearly optimistic, especially in the area of AI. CEO Hock Tan emphasized very strong demand for custom AI chips. New AI chip orders in the quarter exceeded USD 30 billion, significantly above the actual sales delivered during the period. Management also pointed to the high value of shipments and production capacity secured through 2028. Broadcom confirmed strategic relationships with the largest technology clients, including Google, Anthropic, OpenAI and Meta, as well as its participation in the AI XPV platform, which aims to finance and deploy large-scale computing capacity for AI laboratories.

An important part of the message was also the emphasis that Broadcom does not intend to compete in the ready-made server rack segment, but instead focuses on the most specialized and margin-rich part of the value chain: ASICs, XPUs and networking solutions.

The outlook remains strong, but the valuation leaves no room for error

The outlook presented by the company remains very strong, although the market reaction showed that expectations for Broadcom were already extremely high. For the third quarter of FY2026, the company forecasts revenue of around USD 29.4 billion, above the previous consensus, with an adjusted operating margin of around 67%. Key assumptions include:

- around USD 20.5 billion in semiconductor revenue,

- around USD 16.0 billion in AI semiconductor revenue, representing growth of more than 200% y/y,

- around USD 8.9 billion in infrastructure software revenue,

- maintaining the annual AI chip revenue forecast for FY2026 at USD 56 billion and the target of exceeding USD 100 billion in FY2027.

Despite the very strong results, Broadcom shares fell almost 13% in after-hours trading, which can be interpreted more as the result of profit-taking and overly high expectations than a deterioration in the company’s fundamentals. The market reacted negatively, among other things, to the slight disappointment in the software segment, the lack of an upgrade to the long-term AI forecast for FY2027, and the clear reduction in share buybacks compared with the previous quarter.

US OPEN: The market extends losses as investor concerns grow

What's next for Brent crude❓Traffic in the Strait of Hormuz at its lowest level in three weeks🚢

Market Wrap: European indices decline amid US - Iran tensions📉 Semiconductors under pressure

📉 US100 loses 1.5%

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.