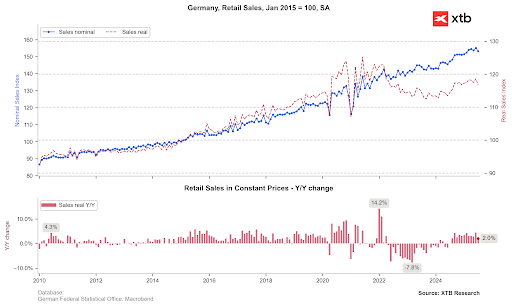

EURUSD began today's session with a degree of weakness, following the release of poor German retail sales data and lower producer inflation (or rather, deflation). German retail sales fell by 1.5% month-on-month and rose by only 2.0% year-on-year, a significant slowdown from the nearly 5% growth seen in June. Such weak data undermines the narrative of a robust European consumer.

Additionally, data from France and Spain was released. French inflation remains extremely low at 0.9% year-on-year, although it did see a monthly increase of 0.4%. In Spain, CPI inflation remains elevated at 2.7% year-on-year but failed to rise as expected to 2.8%.

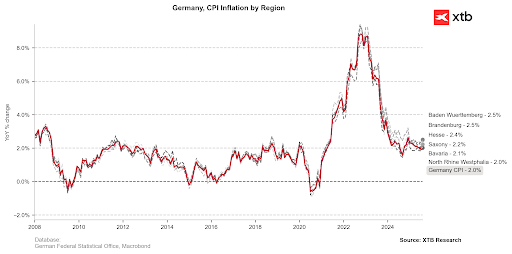

However, we have seen a significant surprise from individual German states, where data has come in notably above expectations, suggesting a considerable rebound in August's CPI inflation. These figures will be released in the early afternoon. For instance, inflation in Brandenburg rose to 2.5% year-on-year from a previous reading of 2.2%. Almost all states saw inflation come in higher than previous levels, though there were virtually no month-on-month changes after the last strong rebound.

Expectations for German inflation point to a rebound to 2.1% year-on-year from 2.0%, with a month-on-month reading of 0.0%. However, there is room for an upside surprise, which should reinforce the ECB's stance to hold interest rates at its upcoming meetings.

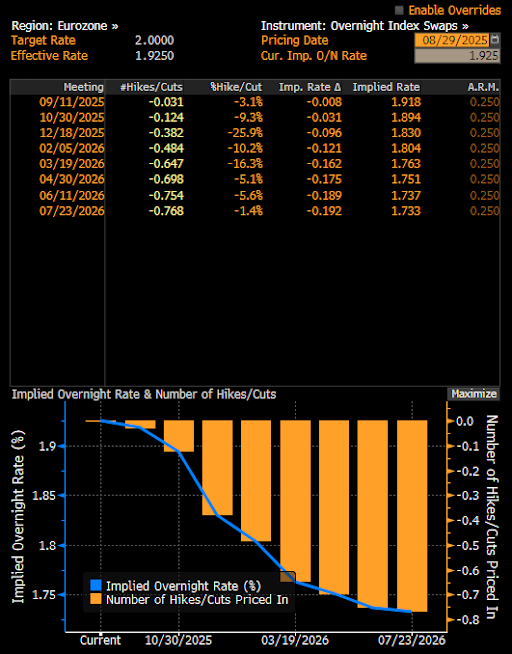

Expectations indicate an almost zero probability of a rate change at the September meeting. For December, the market is pricing in just under a 40% probability. Source: Bloomberg Finance LP, XTB

EURUSD has recovered almost all of its morning weakness thanks to the higher data from the German states. It is worth noting that the pair has reacted to the 1.1600 level four times in recent weeks. Nonetheless, at 1:30 PM BST today, we will see the US PCE inflation data, which could set a new tone for the pair. If inflation proves to be higher than expected, it could temper the strong market expectations (85%) for a Fed rate cut in September. Conversely, if it turns out that tariffs do not have as much of an impact on consumer prices as some Fed members have suggested, confidence in a September move could increase. This might encourage the pair to re-test the 1.17 level, which marks the upper boundary of the descending trend channel.

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Economic Calendar: Industry’s condition in the shadow of oil prices

Chart of the Day 🚩OIL Pulls Back to Test $92.5 per Barrel (24.07.2026)

Morning Wrap: Will the market rebound after Thursday's sell-off❓

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.