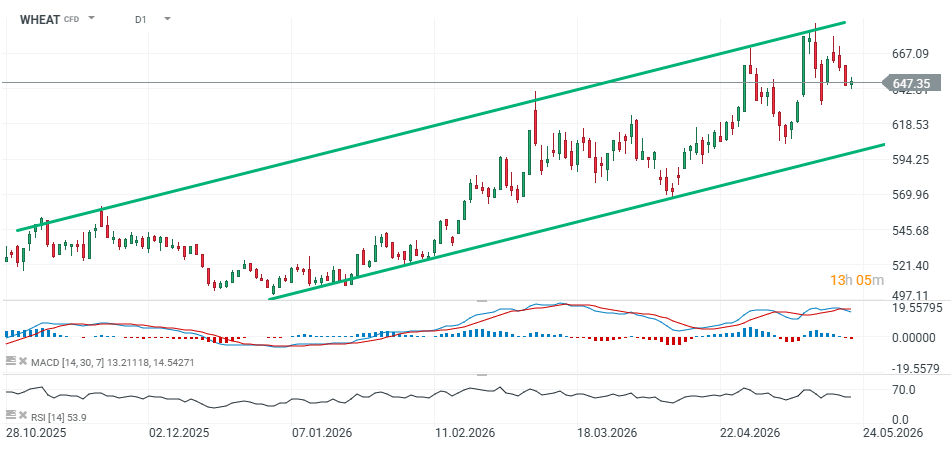

The wheat market recently entered a phase of very dynamic gains after the US Department of Agriculture (USDA) released exceptionally weak forecasts for the 2026/27 winter wheat crop. The scale of the downward revisions surprised even the most bearish market participants and triggered a strong rally in futures markets. Despite this, CBOT wheat futures have recently fallen back below the 650 level.

- On the other hand, according to ADM Investor Services, the arrival of rainfall in key US growing regions has largely neutralized earlier concerns over tightening grain supplies. Potential buying interest from China is currently being more than offset by improving weather conditions across the United States.

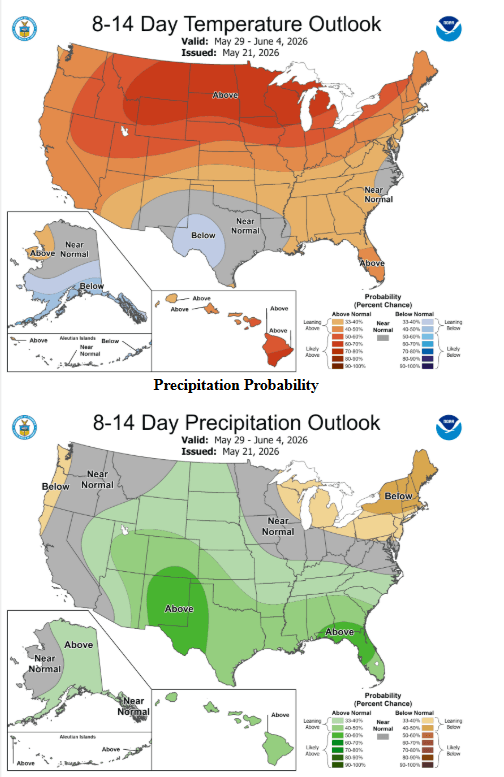

- The US Climate Prediction Center (NOAA) forecasts above-average rainfall across the Great Plains over the next 8 to 14 days, improving crop prospects. Meanwhile, AgResource notes that large speculative traders are reducing long exposure ahead of the weekend and amid ongoing political uncertainty.

Crop problems and speculative activity?

The biggest issue remains the catastrophic weather situation across the southern US Plains. Months of drought have severely affected regions responsible for hard red winter wheat production, particularly western Kansas, eastern Colorado, and the Panhandle area. USDA projects total US winter wheat production at just 1.048 billion bushels, down 25% from the previous season and the lowest level since 1965. Importantly, the initial USDA estimate came in around 160 million bushels below the average analyst forecast.

- Hard red winter wheat has been hit the hardest. Production for this segment is estimated at 514.8 million bushels, down as much as 36% year-over-year. In Kansas — the key state for US wheat production — USDA expects average yields of only 37 bushels per acre, compared to 51 bushels a year earlier.

- The market had been reacting to deteriorating crop conditions since the beginning of the year, but the May USDA report triggered the latest leg higher. If supply prospects continue to worsen, the market may attempt to extend the bullish move further.

- Fundamentally, the market has also received support from the global supply-demand balance. USDA expects smaller harvests not only in the US, but also among major exporters such as Argentina, Australia, and Canada. As a result, global wheat stocks are projected to decline by around 1.5%, while US ending stocks are expected to fall 17% to 775 million bushels — the lowest level in three years.

- Paradoxically, however, higher prices are beginning to reduce the competitiveness of US wheat on export markets. The spring rally pushed US winter wheat prices well above Russian offers. USDA forecasts that US wheat exports in the 2026/27 season will decline 15% from the five-year highs recorded a season earlier, falling to 762 million bushels.

- At the same time, USDA estimates that the average price received by US farmers will rise to USD 6.50 per bushel, USD 1.50 higher than in the 2025/26 season. For producers, this creates attractive selling opportunities.

Current price movements are largely being driven by speculative fund activity. Many funds previously held significant short positions in wheat, and aggressive short covering can trigger extremely volatile price action. Nevertheless, history shows that rallies in wheat often fade relatively quickly, as funds are usually reluctant to maintain long positions for extended periods.

WHEAT (D1 interval)

Source: xStation5

Source: NOAA

NZD the strongest currency after a hawkish surprise from the RBNZ 📄

Economic Calendar: Richmond Fed Index and interesting companies' results ahead 🔎

Morning wrap (27.05.2026)

Daily Summary: Semiconductors lift Nasdaq to new highs; DJIA under pressure

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.