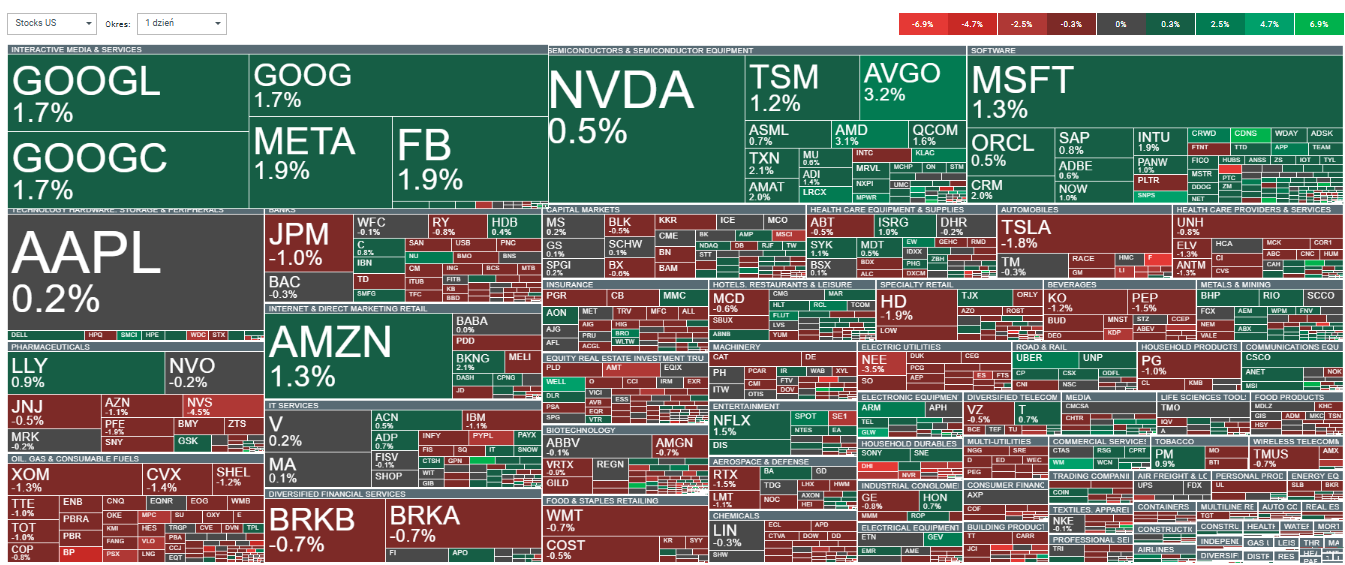

- U.S. stock indexes are having a mixed session today, but the technology sector is gaining, supported by shares of software and semiconductor companies. The market is waiting for the results of AMD, Visa and, most importantly, Alphabet, which will be known after today's US session. AMD shares gain more than 3% ahead of the report, and Alphabet 1.5%

- Currently, the US100 is gaining 0.8%, but other US benchmarks like the US30 and US500 are losing marginally. The pullback in the dollar following weaker-than-forecast JOLTS data supported gains in gold, which is gaining almost 1% today and reaching a new ATH at $2770 per ounce.

- PayPal shares lost 3.5% today despite better-than-expected earnings per share and 6% year-on-year revenue growth, which was in line with expectations. The company reported EPS of $1.20, above the $1.07 expected on Wall Street, but the increase in profitability (and margins) was offset by slightly more mixed forecasts, signaling pressure on earnings realization.

- McDonald's shares lost more than 3.5% after Q3 results. Comparable sales fell in Q3 quarter-on-quarter more sharply than expected, by -1.5% vs. -0.67% expectations. Operating profit fell 1% y/y.

- Pfizer's shares lost 1.5% despite the strong results, after Wall Street analysts said the main component of the better results was the sale of the next tranche of Covid vaccines, but other aspects of the company's business remain uncertain.

- The number of job openings (JOLTS) in the US, in October, was 7.443 million versus 8 million forecast and 8.040 million previously. Yields on 10-year U.S. bonds fell to 4.28% today, down from above 4.31% before the JOLTS data was released. EURUSD gains 0.07%

- The U.S. House Price Index rose 0.3% m/m vs. 0.1% expected and 0.1% previously (4.2% y/y vs. 4.5% previously).

- US 20-year Case/Schiller index was 5.2% y/y vs. 5.1% y/y and 5.9% y/y previously

- US Redbook (sales growth at large retail stores in the US) was 5.6% y/y vs. 4.6% previously.

- US wholesale inventories m/m were -0.1% m/m vs. 0.1% m/m and 0.1% previously

- US retail inventories excluding automobiles were 0.1% m/m vs. 0.5% expected and 0.5% previously.

- The overall data, despite weaker JOLTS, point to stronger consumer demand, with wholesale inventories falling, a higher pace of comparable sales growth in the US Redbook, and a higher-than-expected average house price index.

- Agricultural commodities on the Chicago Stock Exchange gained slightly today, supported by a weaker dollar. Wheat on the CBOT rose more than 2%, while cotton contracts on ICE stopped near $70.7 a bale. Cocoa contracts rose the strongest, over 4%

- Gold is gathering the main attention of the precious metals market, but silver also gained more than 2% today. Aluminum and platinum are also trading noticeably higher. Industrial metals, on the other hand, reported a weak performance, despite initial gains in the Chinese stock market

- The prospect of an additional $1.2 trillion stimulus package in China initially supported investor sentiment, but Chinese benchmark contracts have now completely erased the initial gains. Ultimately, China is expected to announce a decision on additional treatments to support the economy at a meeting of the Standing Committee of the National People's Congress in early November.

- Sentiments of the cryptocurrency market have been very successful. Bitcoin has gained almost 4% and approached the $73,000 mark today, where the ATH from spring, this year, is located.

- Dogecoin is gaining more than 12%, supported by positive sentiment around memcoin, as well as Tesla and Elon Musk, indirectly against the backdrop of Donald Trump's growing lead in the polls ahead of the US election

The software and semiconductors sector stands out today against the broad stock market, which is posting mixed results. Source: xStation5

Daily Summary: As a ceasefire drifts away, markets lose ground

UnitedHealth Group earnings: Healthy growth

US Open: Macro Up, Tensions Down!

Defense sector earnings: RTX, Thales and Northrop Grumman

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.