We conclude Tuesday with declines across nearly all major stock indices. This is primarily the fallout from the sell-off of semiconductor sector companies, initiated by SK Hynix during the early hours of Asian trading.

Stock Market

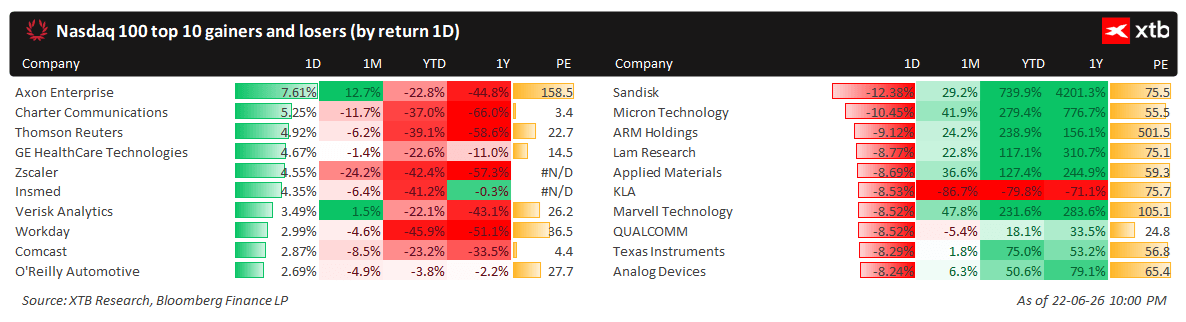

The Korean technological giant, shortly after becoming the country's most highly capitalised company, experienced a sharp correction exceeding 12%, which led to a temporary suspension of trading on the KOSPI. American giants followed suit, including Sandisk (-13%), Micron (-11.2%), ON Semiconductor (-10%), and Marvell (-9%).

Figure 1: Winners and Losers on the Nasdaq 100 (23.06.2026)

Source: Bloomberg, 23.06.2026

Source: Bloomberg, 23.06.2026

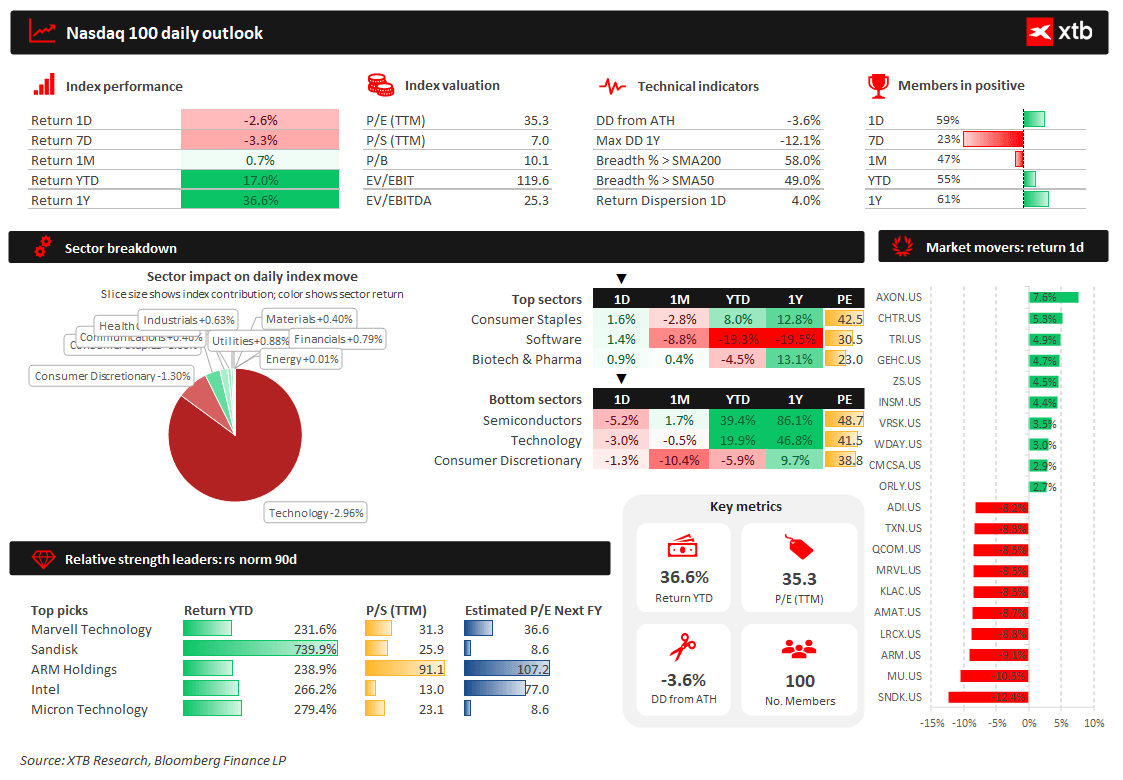

Consolidation following such a rapid upward movement earlier in the year does not seem unwarranted. The question remains regarding the further direction of movement, as increasing questions arise concerning companies' generated profits and profitability.

Figure 2: Dashboard for the Nasdaq 100 (23.06.2026)

Source: XTB Research, 23.06.2026

Source: XTB Research, 23.06.2026

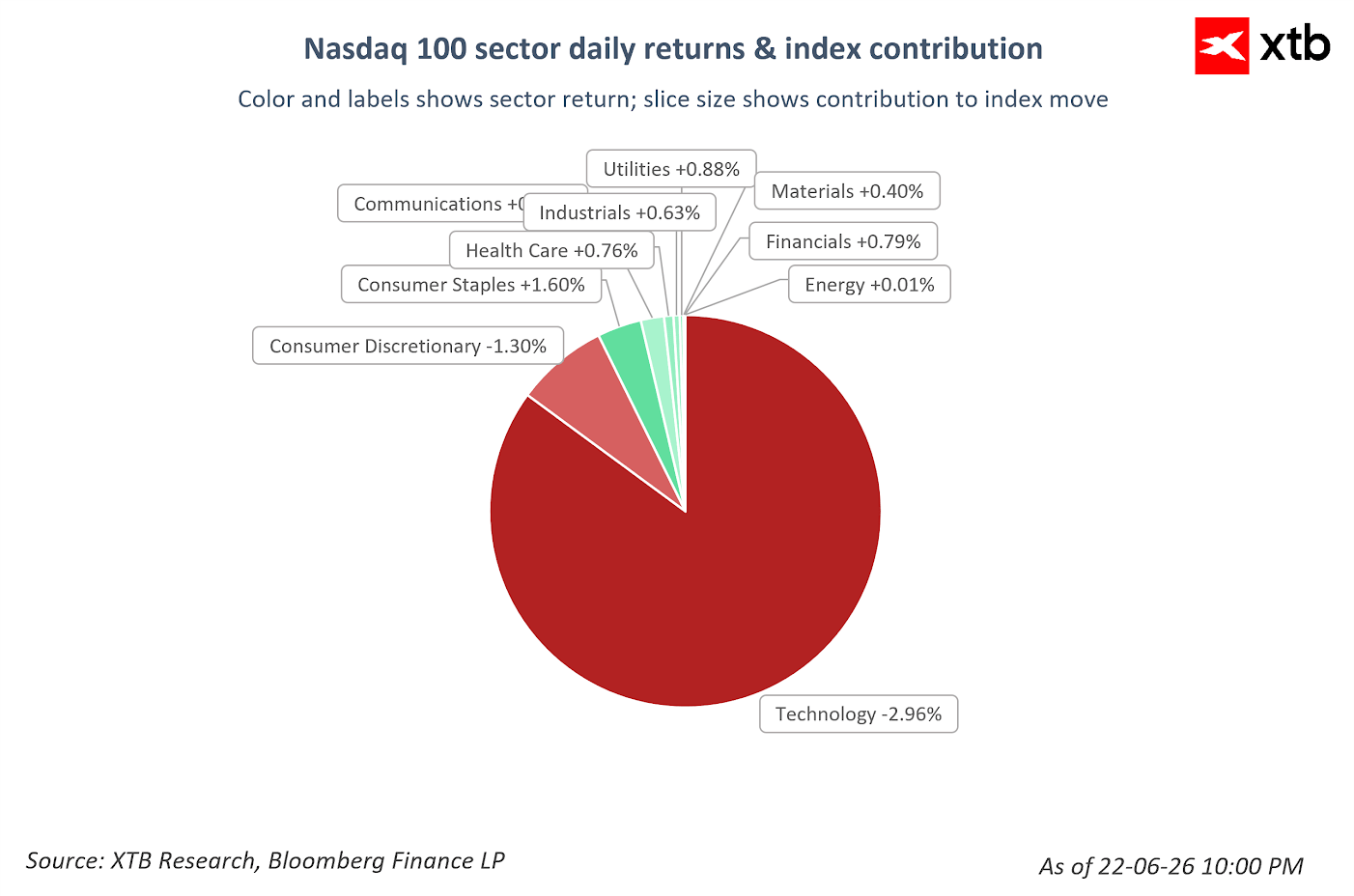

Figure 3: Sector Quotations for the Nasdaq 100 (23.06.2026)

Source: XTB Research, 23.06.2026

Source: XTB Research, 23.06.2026

European stock markets are also in the red today, where companies from the technology sector were likewise the main losers.

- The German DAX weakened by 1% today,

- the French CAC40 by 0.7%,

- and the pan-European Euro Stoxx 50 by 1.3%.

The British FTSE 100 is down by only 0.1%, awaiting developments on the political front following the resignation of Keir Starmer on Monday.

Politics

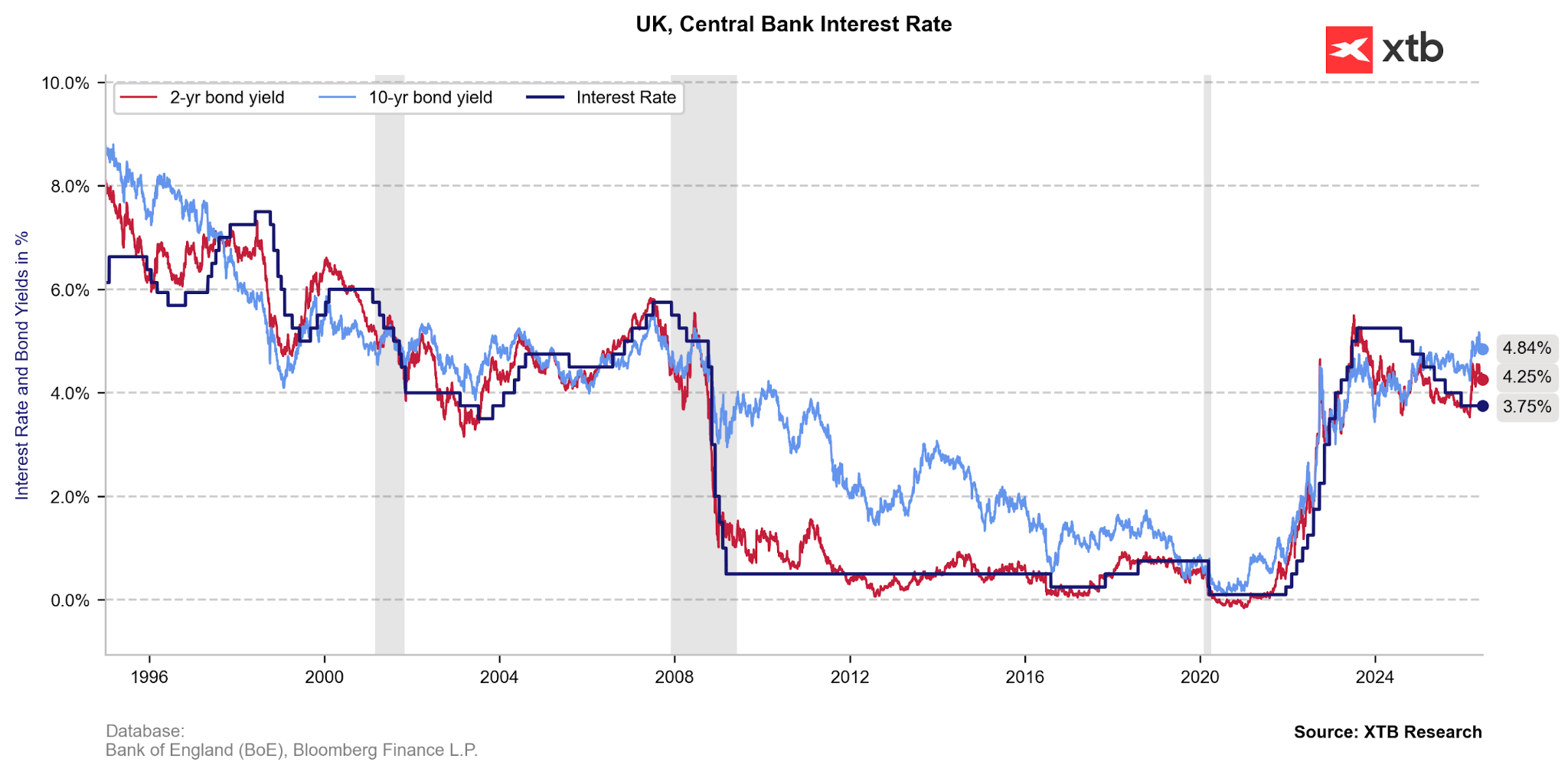

Investors have little doubt that Andy Burnham, the former Mayor of Manchester, will become the country's new Prime Minister. The party appears to understand that it requires swift consolidation, and Burnham's highly convincing victory in Makerfield has demonstrated his ability to win back voters from both Reform UK and the Greens. Should no opposing candidate with sufficient internal party support come forward by 16 July, Burnham will be announced as the new Prime Minister as early as 18 July.

His interventionist approach to the economy may concern the markets, including suggestions that the UK should not be "at the mercy of bond markets." However, he has recently distanced himself from these comments. He has also appointed Andy Haldane, the former Chief Economist of the BoE, and Richard Hughes, the former Chair of the OBR, as key advisors. We view this as an attempt to reassure market concerns in the face of a still very tense situation in the bond market.

Figure 4: BoE Interest Rates and UK Bond Yields (1994 - 2026)

Source: XTB Research, 23.06.2026

Source: XTB Research, 23.06.2026

Commodities

The lack of negative headlines from the Middle East is leading to further decreases in energy commodity prices.

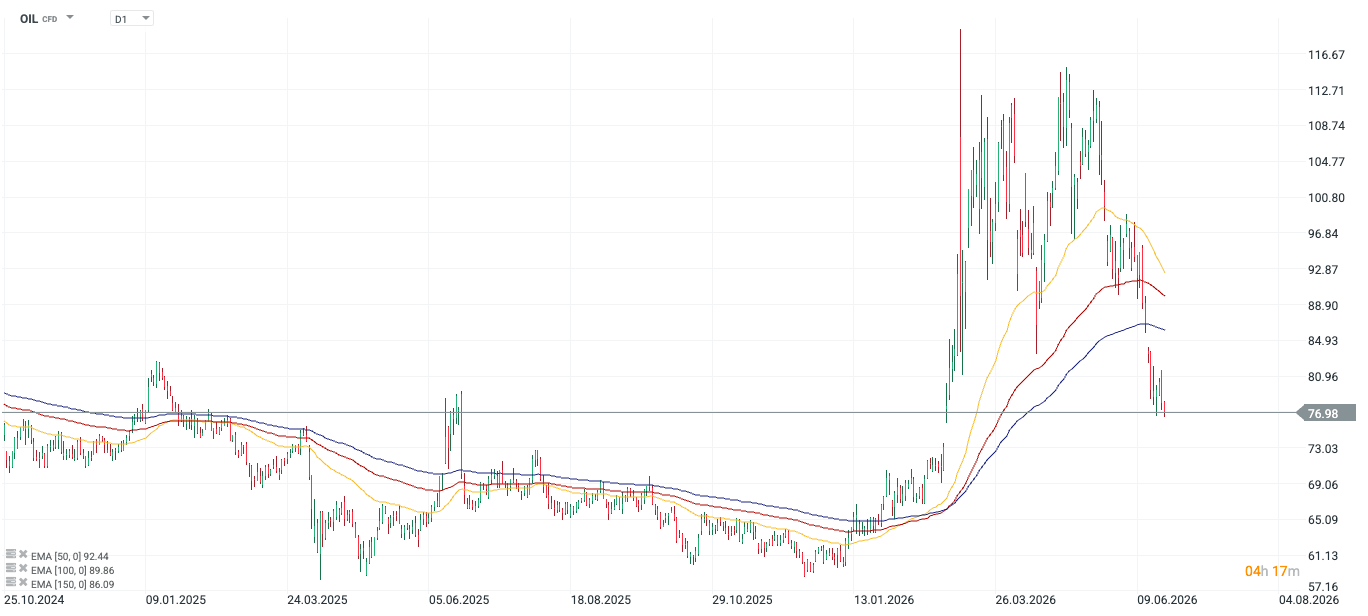

Crude Oil:

- A barrel of Brent is priced at $77 today (a decrease of 1.2%).

- A barrel of WTI is priced at $73 (a decrease of 1.1%).

Figure 5: OIL [D1] (25.10.2024 - 23.06.2026)

Source: xStation, 23.06.2026

Source: xStation, 23.06.2026

Natural Gas:

- NATGAS is down by 3.2% to $3.15.

- TTF remains largely unchanged, around $42.2.

Precious Metals:

- A troy ounce of gold is currently priced at approximately $4132 (-1.4%), and silver at $62 (-4.7%)

Macroeconomic Data

Market attention today was focused on the release of the June PMI data. What did we learn?

- The service sector in European countries remains weak, while manufacturing is faring slightly better (though even here, we can speak of modest growth at best).

- Data from the UK was particularly disappointing—both measures were significantly below consensus.

Currencies

In the foreign exchange market, the dollar's position remains unshaken, as it continues the appreciation initiated by the latest hawkish FOMC meeting. The EURUSD pair broke the 1.14 level today. All other currencies in the G10 group are weakening against the US dollar. This is particularly true for those with high beta, namely SEK, NOK, AUD, and NZD.

—

Michał Jóźwiak, Financial Markets Analyst at XTB

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Three markets to watch next week (07.08.2026)

Chart of the Day: What will drive the US stock market? (07.08.2026)

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.