Market sentiment at the start of the session

The market opened Thursday clearly influenced by a global rotation out of the AI/tech sector—gold and silver are leading the gains (up 0.79% and 1.10%, respectively), serving as safe-haven assets, while WTI and Brent crude are down more than 0.4–0.55%, continuing their worst quarter since 2020. Bitcoin is down 0.41% amid the general risk-off sentiment, and European indices are opening mixed—the DE40 is up a symbolic 0.03%, while the UK100 and US100 are slightly in the red, signaling investor caution ahead of this afternoon’s NFP report.

The greatest volatility is seen outside the main CFD table—the KOSPI opened with a drop of as much as 5–6%, triggering a trading halt (“sidecar”), while Samsung Electronics and SK Hynix lost over 7–9% at the open after the chip sell-off on Wall Street directly impacted Korean memory manufacturers. The Nikkei 225 is reacting more moderately (about -1% to -1.2%), and the Japanese yen, at a 40-year low (USDJPY 162.37–162.38 on our platform), is fueling speculation about intervention by the Japanese Ministry of Finance, especially given Friday’s low liquidity due to the U.S. holiday.

What to Look For—Today's Top Stories

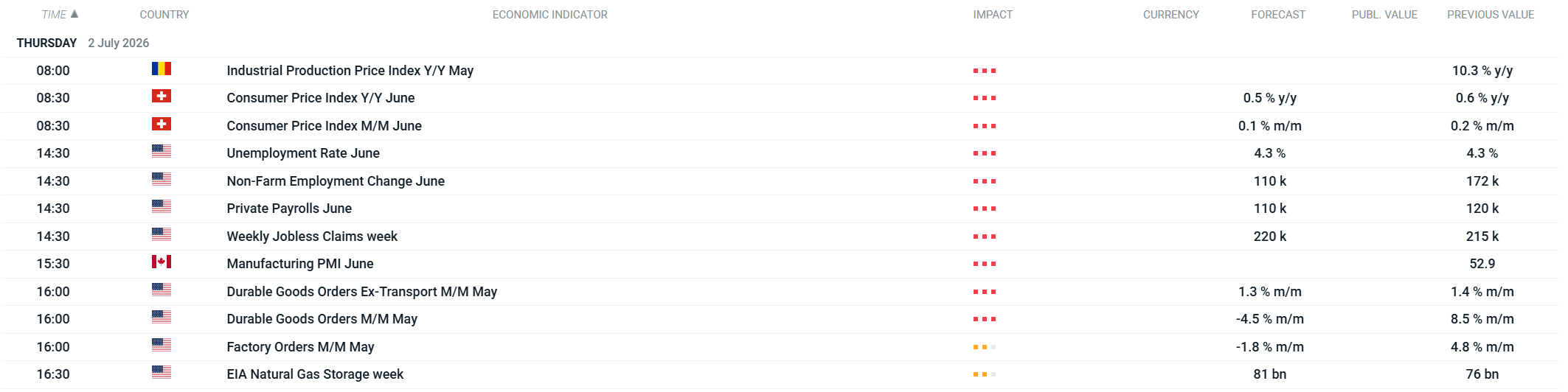

The key event of the day will be the June NFP report at 2:30 p.m. – the consensus is 110,000–115,000, compared to 172,000 in May, with the unemployment rate stable at 4.3% – and the wide range of forecasts (25,000–200,000) suggests a potentially sharp reaction from the USD and yields. It’s also worth keeping an eye on this afternoon’s data on durable goods orders and weekly jobless claims, which could further influence expectations regarding the Fed’s September decision.

It’s also worth keeping an eye on the CPI data from Switzerland (8:30 a.m.) and durable goods orders from the U.S. (4:00 p.m.).

Today's Macro Calendar. Source: xStation

📉 US100 loses 1.5%

EURUSD: Fed Pushback Keeps Dollar Supported Despite Softer Inflation Data

Economic calendar - Europe's Inflation and US Housing Market in Spotlight

Morninga Wrap: Wall Street Under Pressure. AI Loses Momentum, Netflix Disappoints, and the Persian Gulf Erupts

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.