Today's key data from the American economy: the USA's Consumer Price Index (CPI) inflation data! A slight rebound in the main inflation is expected mainly due to the fading base effect. From the Fed's perspective, however, the core inflation will be crucial. Today's reading will provide a bit more certainty regarding the potential decision on interest rates in September. What are the expectations for today's data? How might EURUSD react?

-

The market consensus anticipates an increase in inflation to 3.3% YoY with a monthly increase of 0.2% MoM. Previously, for June, these figures were 3.0% YoY and 0.2% MoM, respectively.

-

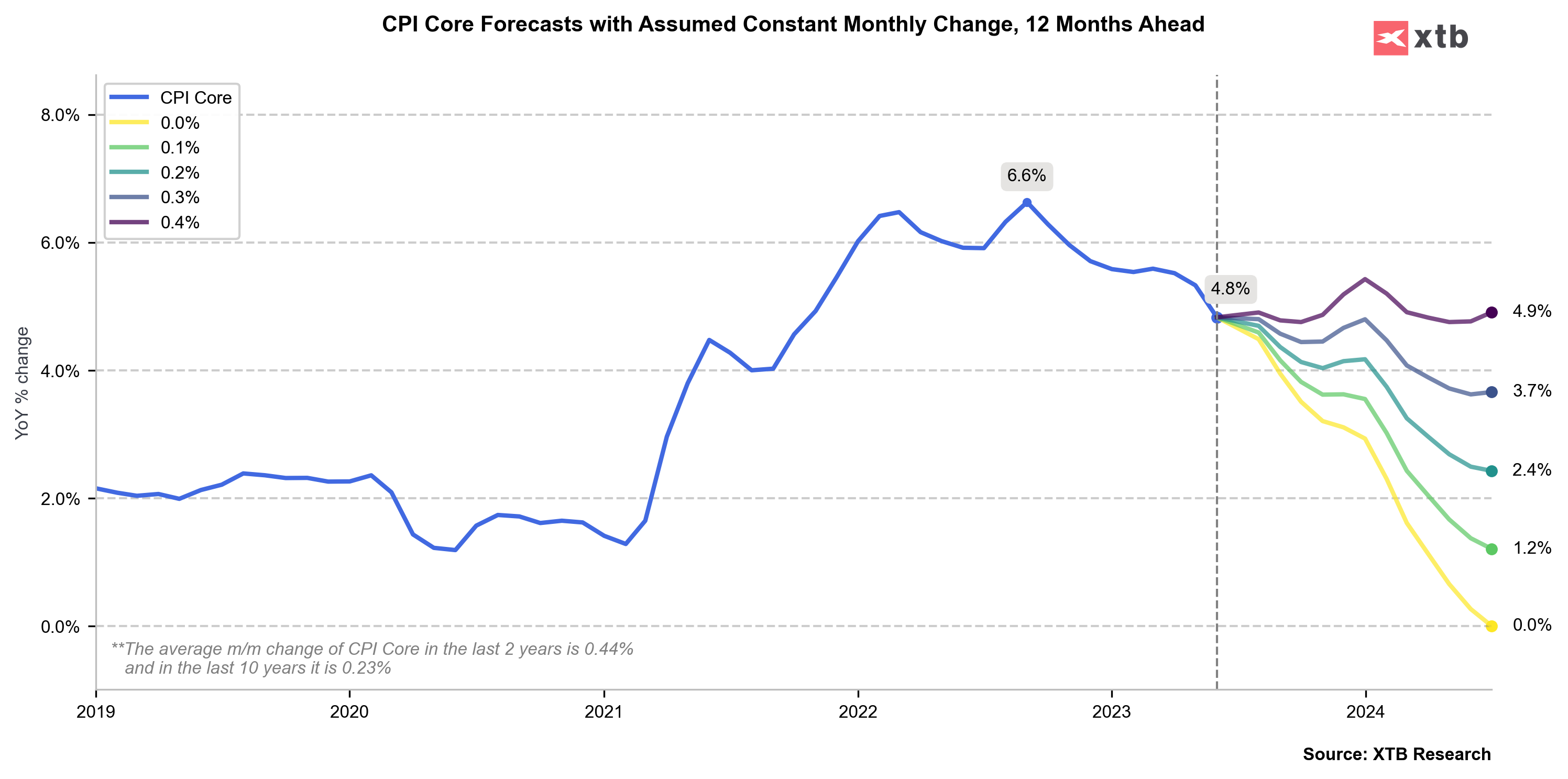

Core inflation is projected to come in at 4.7% YoY with a monthly increase of 0.2% MoM. The previous figures were 4.8% YoY and 0.2% MoM.

-

The 0.2% monthly growth aligns with the Federal Reserve's long-term inflation target (2025). This also represents the long-term average monthly inflation growth.

-

However, based on the significant rise in fuel prices in July, there might be a faster increase in monthly inflation to 0.3% MoM, as indicated by Bloomberg Economics. Alongside the increase in fuel prices by approximately 7% in July, energy bills have surged due to the heatwave, impacting electricity costs. Natural gas prices have also risen.

-

A similar energy cost situation might occur in August as well. According to Bloomberg Economics, energy costs in August could add 0.3 percentage points to monthly inflation!

-

On the other hand, Goldman Sachs points out a notable slowdown in inflation related to rent equivalence, used car prices, and non-housing service inflation.

The Fed places significant emphasis on core inflation. They understand the recent energy price rebounds are beyond their control. Hence, even with a potential rebound in the main CPI, the Fed's decision will hinge on core inflation. If the Fed observes progress toward its target in this regard and no detachment of inflation expectations is apparent, they might raise interest rates once more this year, particularly if the core inflation remains stable and the monthly increase exceeds 0.2%.

While everyone is focused on the sharp decline in the main CPI inflation, the Fed's attention is directed towards core inflation. The outlook for the coming months appears relatively favorable. With a monthly increase of about 0.2%, core inflation will continue to drop and only rebound slightly towards the end of the year.

On the other hand, the main inflation largely influences consumer inflation expectations. Recent energy price rebounds could complicate matters in the following months, and the situation might worsen by year-end if oil and fuel prices remain at or above current levels. This would have a positive impact on the annual contribution to inflation.

Market Reaction:

Undoubtedly, markets will initially scrutinize the main reading. A higher reading could boost the dollar while causing a retreat in Wall Street contracts. However, the sustainability of this movement will depend on core inflation. It's unlikely for surprises to occur in this aspect. Thus, considering expectations for core inflation, the market should lean towards more risk-taking behavior, moving away from the dollar and re-entering the stock market. This scenario might not unfold if the core CPI rises by more than 0.2% MoM or remains at 4.8% YoY.

EURUSD:

The EURUSD pair is breaking above the descending trendline and retesting the vicinity of the 1.1000 level. A short-term resistance zone lies around 1.1040. If inflation comes in lower than expected, especially with a decline in core inflation as predicted, EURUSD should attempt to breach the 1.1050 level. Conversely, if inflation surprises with stronger growth, EURUSD might quickly drop below 1.10 and head towards the ascending trendline formed after the local lows in early July and early August. Source: xStation5.

Chart of the Day: EURUSD Higher, but Still a Game of Expectations, Not a Trend

NOK surges following Norges Bank's rate hike

Economic Calendar: Markets Focused on German Data and Central Bank Speakers

BREAKING: Strong data from the German manufacturing sector!

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.