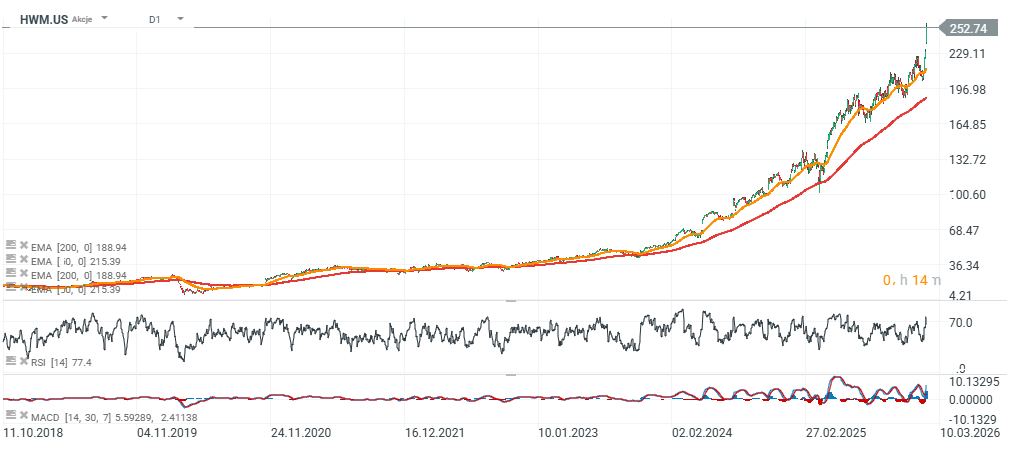

Howmet Aerospace (HWM.US) is at the heart of one of the strongest aerospace & defense upcycles in recent years. The company has delivered a total return of more than 80% year-over-year, and its latest quarterly results have only reinforced the momentum. Fundamentals remain solid: cash flows are rising, the balance sheet is disciplined, and the market is now pricing in an almost flawless execution of the growth strategy.

In Q4, Howmet reported:

-

Non-GAAP EPS: $1.05 (vs. $0.97 consensus)

-

Revenue: $2.2bn (+16% y/y)

-

Commercial Aerospace sales: +13% y/y

The market reaction was clearly positive, with the stock up nearly 10% following the release. The company also issued constructive guidance for 2026, calling for:

-

Revenue: approx. $9.1bn

-

Adjusted EPS: approx. $4.45

-

Free cash flow: approx. $1.6bn

On a full-year basis:

-

Revenue: +11% y/y to $8.25bn

-

Adjusted EBITDA: +26% y/y to $2.4bn

-

Adjusted EPS: +40% y/y to $3.77

-

Free cash flow: $1.43bn

At the same time, Howmet reduced its net debt-to-EBITDA ratio to 1.0x, paid down part of its debt, executed share buybacks, and raised its dividend significantly—underscoring the quality and resilience of its cash generation.

Fundamentals: strong demand in a cyclical environment

Howmet’s growth is supported by:

-

Sustained demand in commercial aviation and high product quality

-

A dynamic defense segment (Defense Aerospace +21% y/y in 2025)

-

Rising defense budgets in the US and Europe

-

Operating leverage alongside double-digit revenue growth

At the same time, the company is maintaining elevated capital expenditure, which may limit near-term FCF growth but strengthens its competitive position over the longer term. With 2026 EPS expected around $4.45–$4.50, the market values Howmet at over 50x forward 12-month earnings, while the trailing P/E exceeds 60x. These multiples are typical of high-growth technology names rather than a traditional aerospace components manufacturer—even one operating with exceptional efficiency. Assuming long-term EPS growth in the high-teens, current multiples still imply a very optimistic scenario of a continued upcycle with limited disruption.

Key risks to monitor

-

Potential volatility in defense spending

-

Risk of slower deliveries in key programs (e.g., the F-35)

-

Competitive pressure in aerospace components

-

Elevated capex if the cycle weakens

-

Escalation of trade tensions and the impact of tariffs

Technical picture and sentiment

Momentum remains exceptionally strong, with the stock at all-time highs and clearly above long-term moving averages. Such a setup often attracts momentum capital and can sustain the trend even at premium valuations. On the other hand, a significant distance from the 200-day moving average increases vulnerability to a correction if sentiment turns.

Howmet Aerospace remains one of the leaders of the current aerospace & defense cycle. Fundamentals are strong, the balance sheet is healthy, and earnings growth is robust. However, the valuation requires continued near-perfect execution and a supportive macro and defense-budget backdrop. From an analytical perspective, this is a high-quality operator—but at current multiples, the market has already priced in much of the upside scenario. The next leg for the stock will likely depend on the durability of the commercial and defense aviation cycle and Howmet’s ability to sustain its current pace of earnings growth.

Source: xStation5

USA Rare Earth Acquires Key Brazilian Rare Earth Metal Mines ⛏️

US OPEN: Return of geopolitical concerns hits markets 💥

New Player in Google’s Ecosystem? Marvell Triggers Market Reaction

Will Wall Street reach new record high?🗽Highlights from S&P 500 earnings season

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.