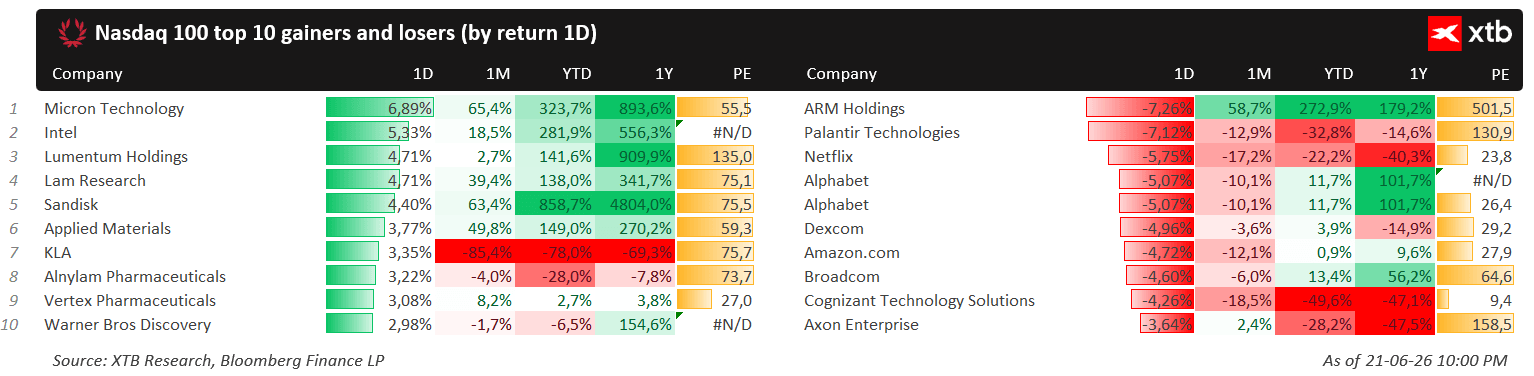

In recent weeks, a clear deterioration in the condition of technology companies has been visible, with the exception of semiconductor manufacturers. Returns on the latter’s stocks since March this year have been in triple digits, while all hyperscale companies have lost, from a few to several dozen percent of their market value, over the last month alone.

Shouldn’t the moves of these entities be linked in the context of investment in AI?

Problems with monetization

Massive AI investments by U.S. technology sector leaders require a strong justification in the form of monetization. It must be real in order to keep indices near their highs. It is precisely this wavering belief in monetization that is putting pressure on markets. How?

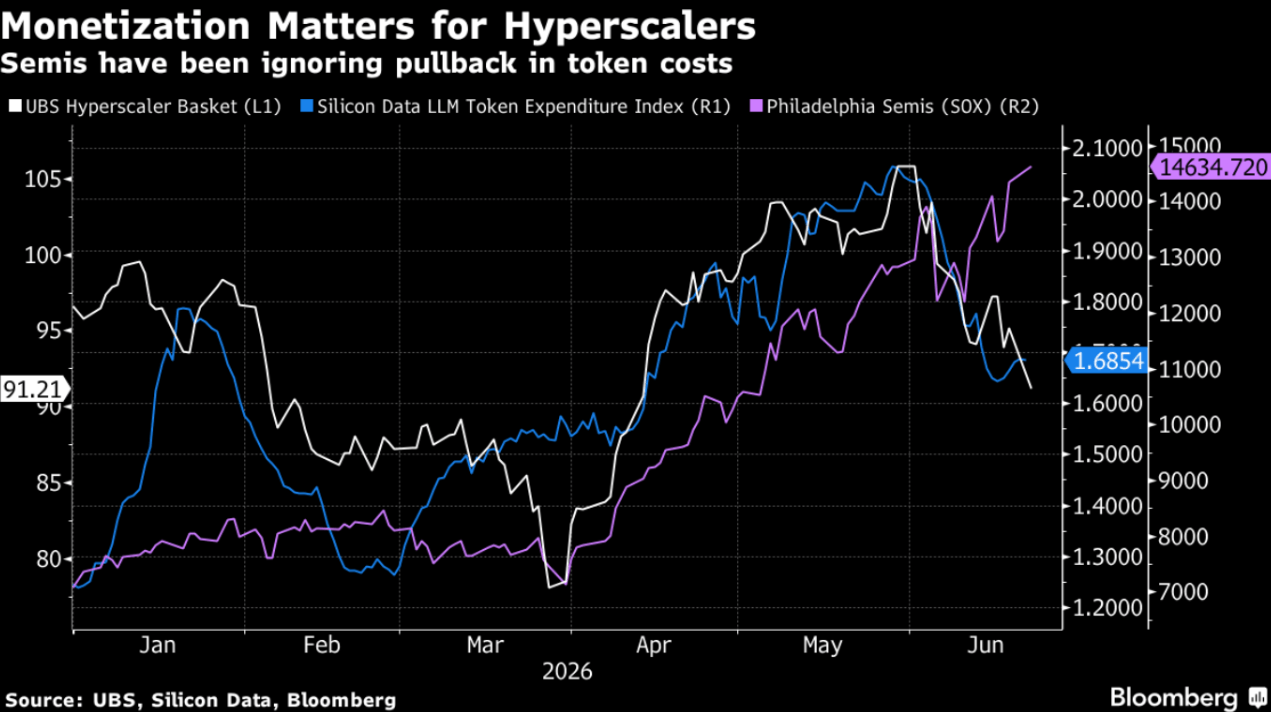

Until the next financial results are published, most of the market is forced to speculate; however, specialized data aggregators already exist today that indicate where and to what extent monetization is failing. One of them is the Silicon Data LLM Spending Index.

Source: Bloomberg Finance Lp.

As you can see, in recent months this chart has shown a very high correlation with hyperscale companies’ valuations. This index is one of the indirect gauges and leading signals regarding AI spending. Recently it has fallen sharply, dragging the technology sector down with it. At the same time, semiconductor companies are doing well, because they earn money from delivering hardware, not from AI itself.

In the AI industry, a “two-speed” segmentation can currently be observed—“low” and “high” or “frontier” intelligence. Analyzing trends in the prices and capabilities of LLM models, it can be seen that while “high-end” AI capabilities (e.g., Fable, Mythos, ChatGPT 5.5, etc.) are impressive, their prices are equally high. “Low-end” models, meanwhile, are experiencing deliberate price hyperdeflation. As a result, companies are increasingly limiting the use of “high-end” AI in favor of “low-end” AI, which is sufficient for most applications.

Precedent and forecasts

Switching to cheaper models and optimization are not new phenomena, this is visible in the chart attached earlier. Sharp rises and falls could already be observed in the first quarter of this year, which corresponded with sell-offs in hyperscale companies.

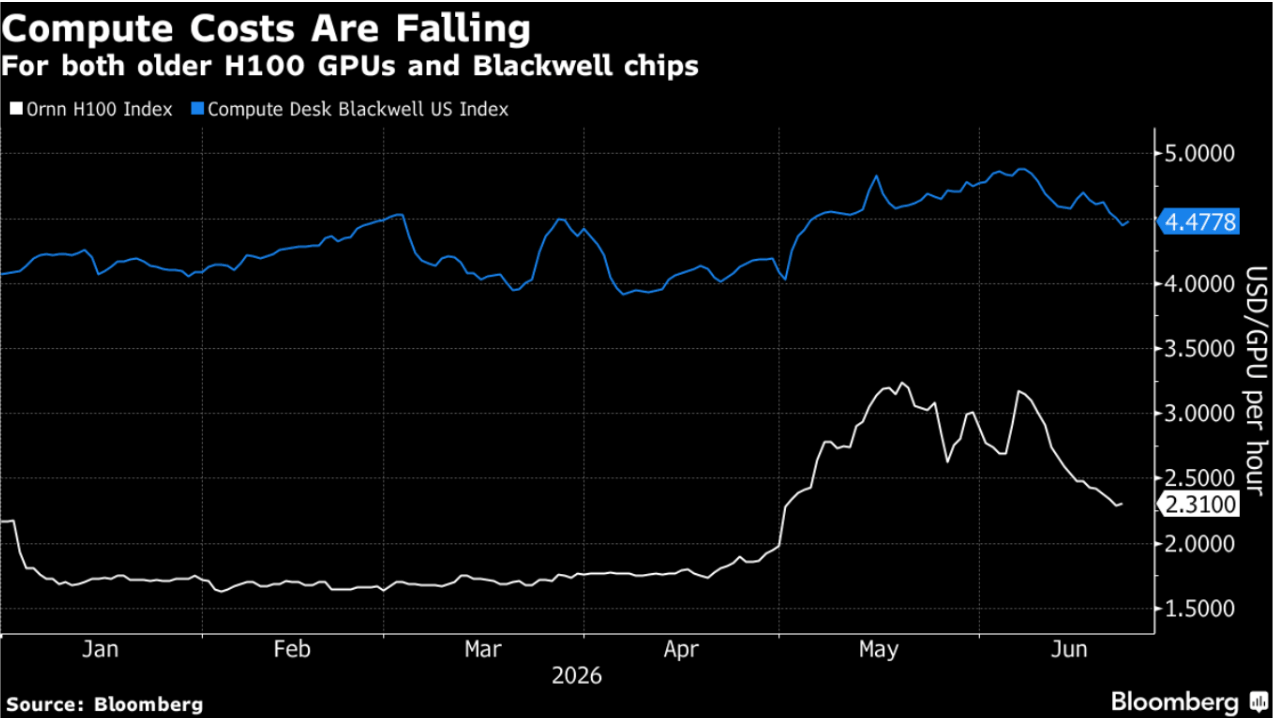

One characteristic feature of supply and demand is that, in the absence of external variables (such as logistics), as the price approaches zero, demand grows toward infinity. AI tokens are an ideal example of a good that, in practical terms, comes closest to such theoretical considerations.

Source: Bloomberg Finance Lp.

If the price drops, as the next generation of “Blackwell” processors is supposed to enable (SemiAnalysis analysts speak of cost reductions of around 99%), one can expect that business will, over time, adapt to the new realities. AI-based solutions will move higher up the value-creation chain, improve margins, and over time allow for further waves of spending on tokens. However, this process will take time—time many investors do not have. The lag of valuations relative to the AI spending index itself is also visible on the chart.

Concerns about AI monetization may persist, and room for further declines still exists. However, the current sell-off episode is more of a speed bump for the AI bull market than a wall. A real verification of the thesis supporting investments in AI will likely take place at the end of this year or at the beginning of the next. Key in this process will be the IPO prospectuses of Anthropic and OpenAI, which may reach investors within a few weeks.

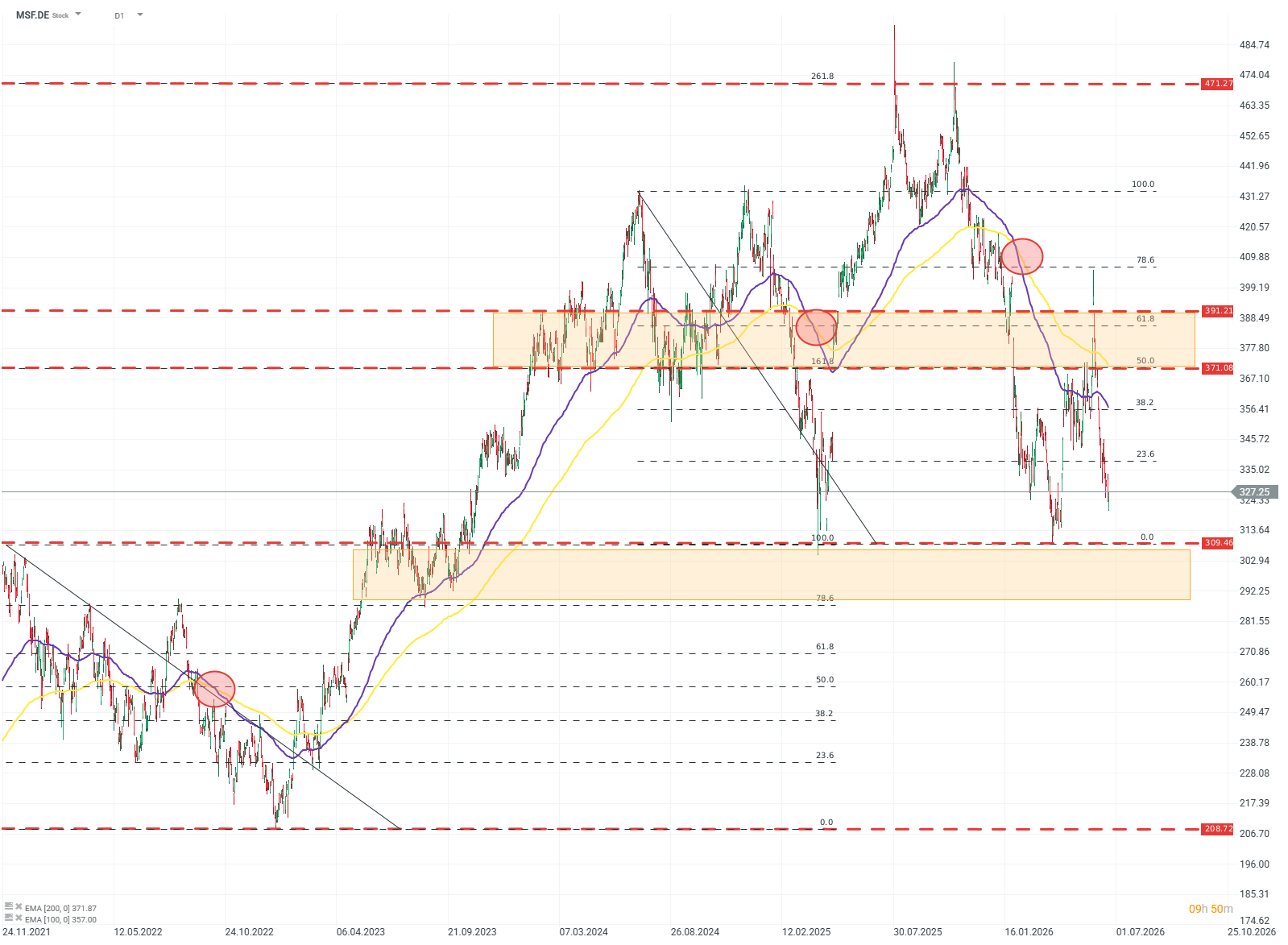

MSF.US (D1)

Microsoft shares are now only about 5% away from an extremely important resistance level around $300. These are levels tested during the declines at the beginning of 2025 and 2026. Looking at the history of price behavior, one can note the “death cross,” which is a strong bearish signal. In Microsoft’s case, however, it appeared near the end of the decline wave rather than signaling a deeper drop. Given the relative strength of resistance around $300, one can expect this to be the case again this time.

Source: xStation5

Kamil Szczepański

Financial Market Analyst at XTB

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.