- US equity indices extend gains, led by another strong rally in technology stocks, while European stocks lag on higher oil prices

- US producer inflation (PPI) came in below expectations, with producer prices unexpectedly falling 0.3% month over month.

- The US dollar is edging slightly lower, although the USD Index continues to hold above the key 100 level.

- US equity indices extend gains, led by another strong rally in technology stocks, while European stocks lag on higher oil prices

- US producer inflation (PPI) came in below expectations, with producer prices unexpectedly falling 0.3% month over month.

- The US dollar is edging slightly lower, although the USD Index continues to hold above the key 100 level.

The technology sector is once again driving gains across global equity markets, as investors try to reconcile a very strong earnings season with rising geopolitical risks in the Middle East. Market attention is focused simultaneously on AI-related corporate results, oil prices, and the outlook for Federal Reserve policy following weaker-than-expected US CPI data. The latest US PPI report reinforced yesterday’s CPI signal, with producer prices falling 0.3% month over month and the annual increase coming in below expectations.

- European stocks lag with lower weight of technology stocks. Euro Stoxx 50 is traded mostly flat, while German DAX drops 0.5%

- Nasdaq 100 futures are up 0.5%, while S&P 500 futures gain 0.25%, supported by very strong results from semiconductor companies.

- ASML shares are rising nearly 8% after the company raised its sales outlook and announced plans to increase production of chipmaking equipment used in AI infrastructure.

- SK Hynix is gaining 9%, catching up with the earlier rise in the memory producer’s US-listed ADRs.

- Brent crude is advancing for a third consecutive session and is trading at around $85.60 per barrel following another wave of US strikes on targets in Iran and Donald Trump’s pledge to intensify military action.

- Despite the geopolitical tensions, oil prices remain well below the earlier highs above $100 per barrel, while investors are increasingly turning their attention to the corporate earnings season.

- The yield on the 10-year US Treasury is edging 1 basis point higher to 4.60%, with a similar move also visible across European bond markets.

- The US dollar remains relatively stable, while markets have largely ruled out a Fed rate hike at the next meeting but continue to price in a high probability of a move in September.

US producer price inflation unexpectedly fell by 0.3% month over month, compared with expectations for a 0.1% increase, while the annual rate came in at 5.6%, below the 6.2% forecast. Core PPI also slowed more sharply than expected, to 4.7% year over year versus a 5.1% forecast, while the NY Empire State index delivered a clear positive surprise, rising to 15 compared with expectations of 9.

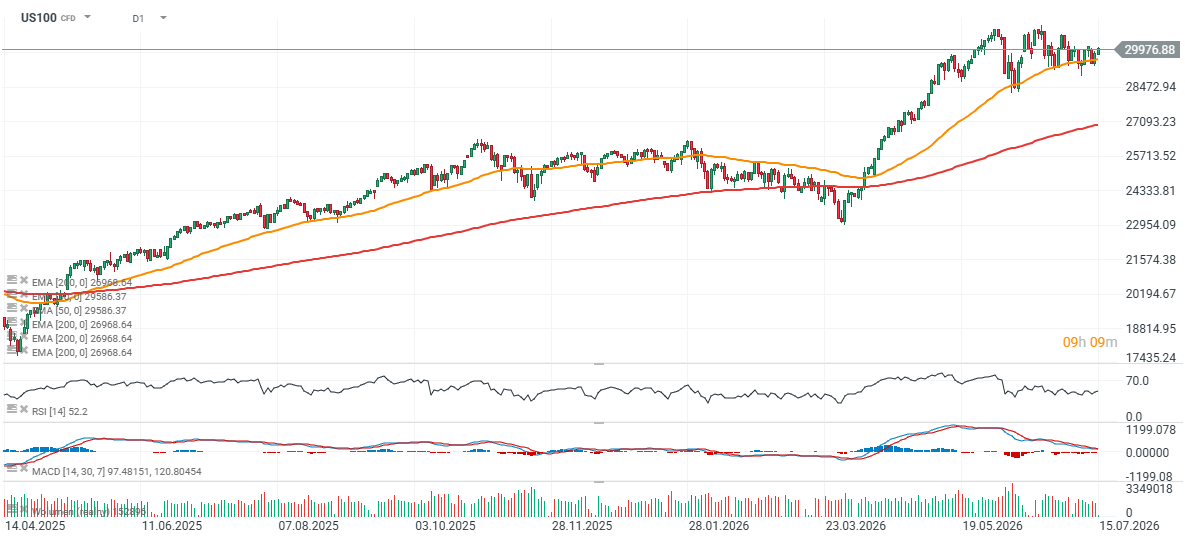

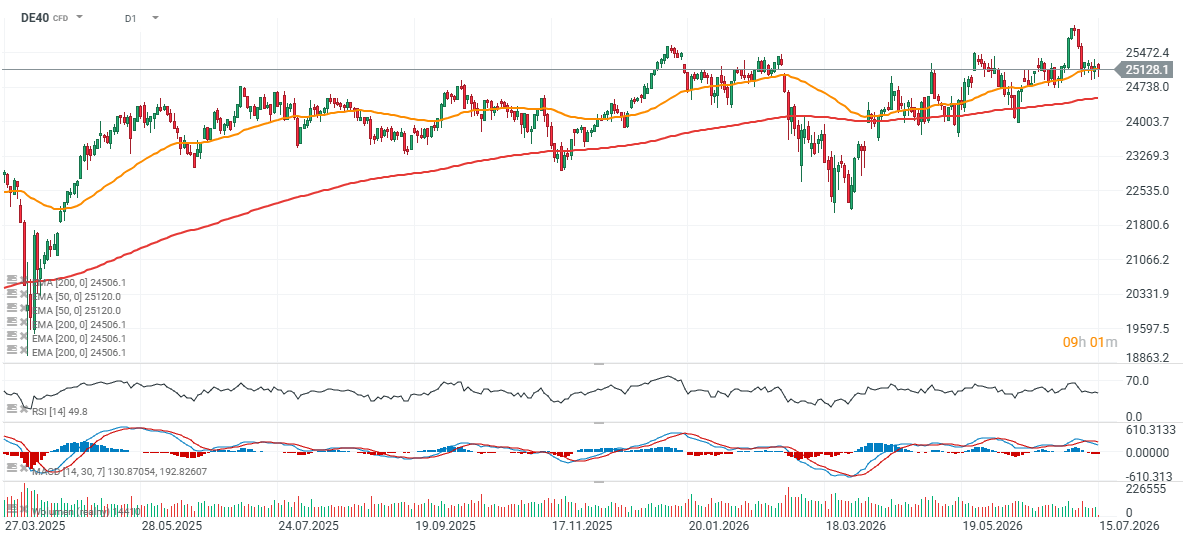

US100, DE40 (D1 interval)

The US100 contract is moving toward the 30,000-point level and is trading above the 50-day exponential moving average, marked by the orange line, at around 29,960 points. Investors continue to buy stocks linked to AI infrastructure, supporting overall market sentiment.

Source: xStation5

Futures on German DAX are slightly down today, testing the 25,000 - 25,1000 pts level, near to the support from EMA50 (the orange line).

Source: xStation5

Netflix disappoints Wall Street 🚩 Stock drops 9% after disappointing outlook

Economic calendar - Europe's Inflation and US Housing Market in Spotlight

Morninga Wrap: Wall Street Under Pressure. AI Loses Momentum, Netflix Disappoints, and the Persian Gulf Erupts

Daily Summary: 📉 A Red Day Across Markets. AI Sector Weighs on Wall Street, Precious Metals Under Pressure

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.