🌍 Geopolitics – The Middle East remains in the spotlight

-

The conflict in the Middle East is escalating: over the weekend, the Houthis launched missile and drone attacks against Israel, while Israeli strikes caused temporary blackouts in Tehran and the surrounding area.

-

The United States continues to build up its forces in the region—several hundred special forces personnel (Rangers, SEALs), thousands of Marines, and the 82nd Airborne Division are already in the area, giving Trump the option of a ground operation.

-

Pakistan has announced that it will host direct talks between the U.S. and Iran in the coming days; Trump has signaled both progress in the negotiations and the possibility of seizing Iranian oil infrastructure, including Kharg Island.

-

Donald Trump said that negotiations with Iran are going well and that the Iranians have agreed to most of the 15 points proposed by the Americans.

-

Israel confirmed via Channel 12: In the event of a potential U.S. ground operation in Iran, the Israeli military will not participate on the ground.

🛢️ Oil and raw materials

-

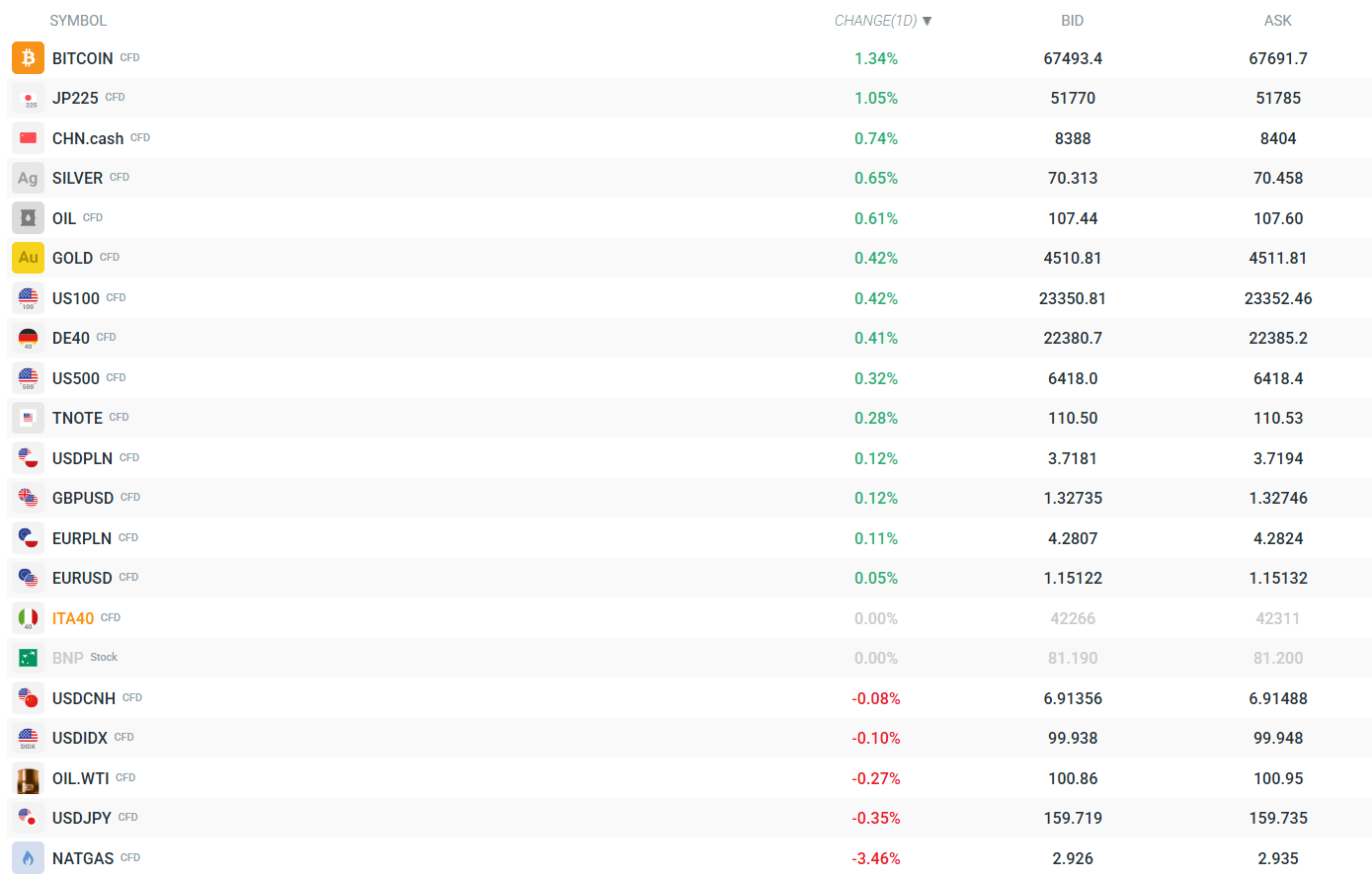

Brent crude opened the week significantly higher (~$107.7/bbl, +0.84%), but retreated after an initial rally, reflecting the uncertain ground built on both hopes for de-escalation and the real risk of a blockade of the Strait of Hormuz.

-

The market is closely monitoring tanker traffic—Trump noted that Iran has allowed 20 tankers to transit the Strait of Hormuz.

-

Gold continues its upward rally, trading at $4,514/oz (+0.49%), while silver is up 0.77% to $70.4/oz – demand for safe-haven and inflation-hedging assets remains strong amid the risk of war.

-

Natural gas (NATGAS) is down 3.23% to $2.93/MMBtu, while wheat on the CBOT is heading for its fourth gain in five sessions as higher energy and fertilizer costs weigh on the outlook for agricultural production.

🏛️ The Bank of Japan and the yen

-

The BoJ maintains its course of monetary tightening: The Summary of Opinions indicates a readiness for further rate hikes, although oil-driven inflation and the risk of stagflation are still cited as dampening factors.

-

Deputy Finance Minister Atsushi Mimura threatened "decisive action" against speculative moves in the yen—a clear escalation in interventionist rhetoric, backed by Governor Ueda’s remarks on the growing importance of the exchange rate for inflation.

-

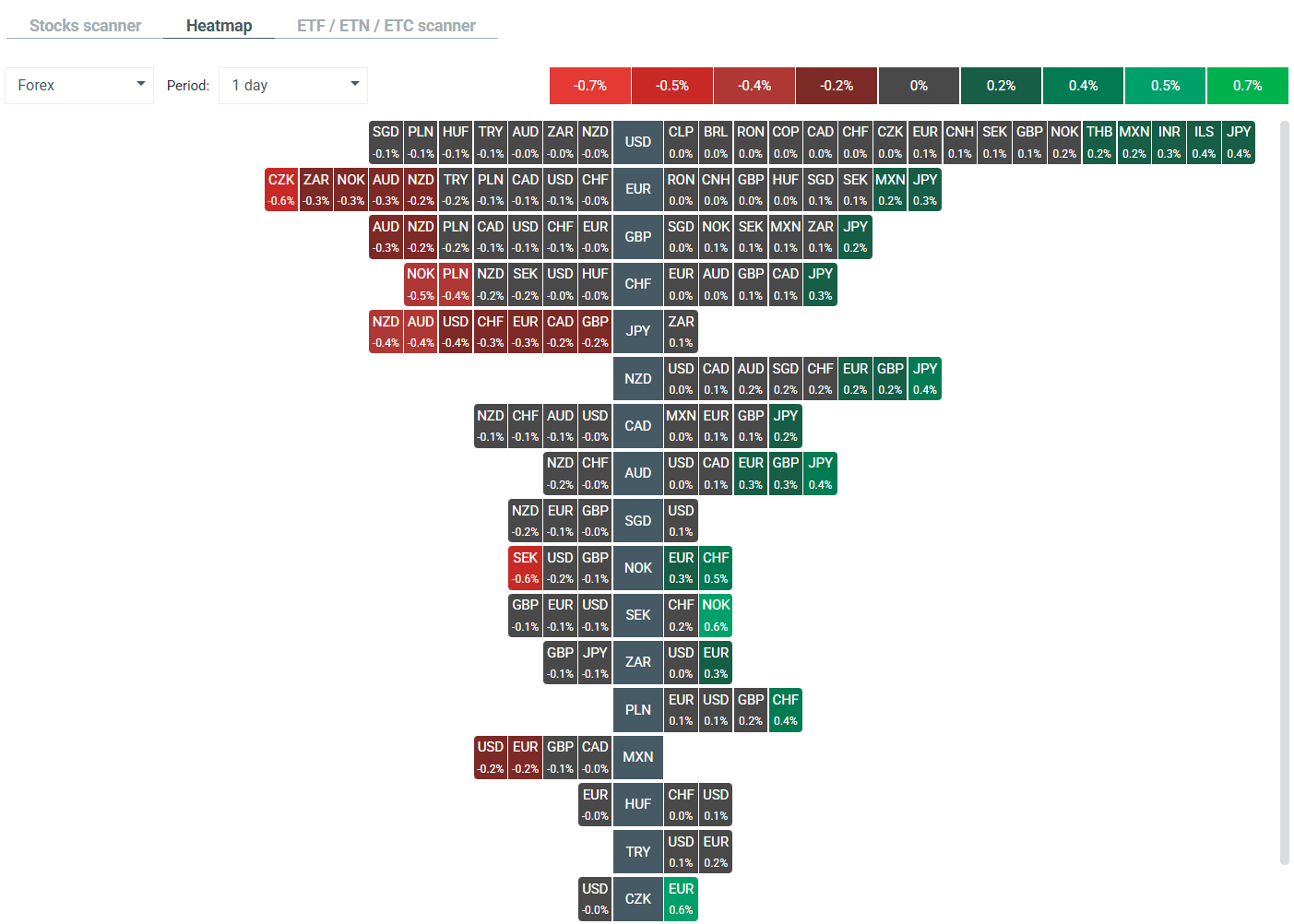

USD/JPY has slipped from around 160.50 to ~159.72 (-0.35%) – the yen is the strongest currency on the forex market today; the USDIDX dollar index has fallen below 100 points (-0.11%). The currencies of the Antipodes and the CAD are performing the weakest.

Heatmap of current volatility in the FX market. Source: xStation

📊 Asian markets and indices

-

The JP225 (Nikkei) is up +1.02% to ~51,757 points, recouping some of its earlier losses; regional markets are rebounding as the conflict did not escalate significantly over the weekend.

-

The CHN.cash (Chinese index) is up 0.90% to 8,401 points; the PBOC set today’s USD/CNY fixing at 6.9223—slightly above market expectations (6.9205)—causing the yuan to depreciate slightly.

-

European futures for the DAX (DE40) point to an opening near 22,380 points (+0.41%); the S&P 500 (US500) is up 0.33% to 6,419 points, and the Nasdaq (US100) is up 0.43% to 23,353 points.

Source: xStation

₿ Cryptocurrencies

-

Bitcoin stands out during the trading session: up 1.36% to ~$67,506 – the cryptocurrency is benefiting from both inflationary pressures and the broader "risk-on" market rally.

📅 In the spotlight this week

-

Friday: Key U.S. NFP report, along with ISM Manufacturing and Retail Sales data—these figures will determine the Fed’s path amid war-related uncertainty.

-

Eurozone: Preliminary CPI for March (Villeroy signals the ECB’s readiness to act, but says it is too early for specific decisions)

-

Australia: RBA Minutes – Following the government’s decision to cut the fuel tax, Morgan Stanley warns of a supply shock in the fuel market and upside risks.

-

BoJ Tankan (Q1 2026) – a key indicator of Japanese business sentiment following weeks of interventionist rhetoric.

Daily Summary: Trump, Inflation, Threats, and Persian Gulf Tensions Cast a Shadow Over Wall Street

Powell Signals Fed Patience, but Inflation Risks Are Rising!

Powell Speaking: Markets Watch Fed Policy

US Open: A Tentative Start to the New Week on Wall Street!

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.