- U.S. equity futures edge higher despite rising oil prices.

- The conflict between the United States and Iran is escalating once again.

- China's June CPI inflation came in slightly below market expectations.

- U.S. equity futures edge higher despite rising oil prices.

- The conflict between the United States and Iran is escalating once again.

- China's June CPI inflation came in slightly below market expectations.

- Asian equities surrendered most of their earlier gains and are now up just 0.1%, as the rally in semiconductor stocks lost momentum. Despite this, U.S. equity futures are moving higher, with the US100 up 0.6% and the US500 gaining 0.3%, while European index futures point to a stronger open.

- Brent crude is up more than 1% to around USD 79 per barrel, marking its third consecutive daily gain following another wave of U.S. strikes on Iran. Government bonds continue to decline across Japan, Australia and New Zealand as markets increasingly price in further Fed rate hikes in response to rising inflation risks.

- The yield on the U.S. 2-year Treasury approached its highest level of the year on Wednesday, although Treasuries traded broadly stable during the Asian session. Meanwhile, the U.S. dollar index is edging lower, while Bitcoin has rebounded to USD 62,500.

- Gold is falling for a fourth consecutive session to around USD 4,050 per ounce, while silver is down nearly 1%, slipping below USD 58 per ounce, as higher interest rate expectations continue to reduce the appeal of non-yielding assets.

- Shipping through the Strait of Hormuz has slowed to a near standstill following a second consecutive day of U.S. strikes on Iran. This has reinforced concerns over disruptions to one of the world's most important energy shipping routes, although equity markets are not yet pricing in the risk of prolonged supply disruptions. The U.S. has also revoked a waiver that allowed Tehran to sell oil globally following attacks on tankers in the Strait of Hormuz.

- China's June CPI rose 1.0% YoY, below the 1.1% consensus and down from 1.2% in May. Meanwhile, PPI accelerated to 4.1% YoY, in line with expectations and up from 3.9% a month earlier. Hong Kong's Hang Seng Index fell more than 1%.

- Nearly 400 S&P 500 companies closed lower yesterday, although the benchmark recovered part of its losses after Donald Trump suggested he does not expect the war to resume.

- The semiconductor sector outperformed after reports that China may allow its leading AI companies to purchase a limited number of Nvidia H200 processors.

- Apple is expanding its partnership with Broadcom, with the value of the agreement for U.S.-made components expected to exceed USD 30 billion. Meanwhile, Meta plans to invest approximately USD 10 billion in its first data center in Canada, further expanding its AI infrastructure.

- Iranian state television reported eight explosions near the city of Bandar Abbas. According to the reports, two projectiles struck Sirik Port, while another two detonated at Jask Port. There were also reports of a bridge being destroyed in northeastern Iran, although these claims have not been independently verified. Tehran warned of potential attacks on U.S. bases across the Middle East, while U.S. officials indicated that the next wave of strikes on Iran could be even more intense.

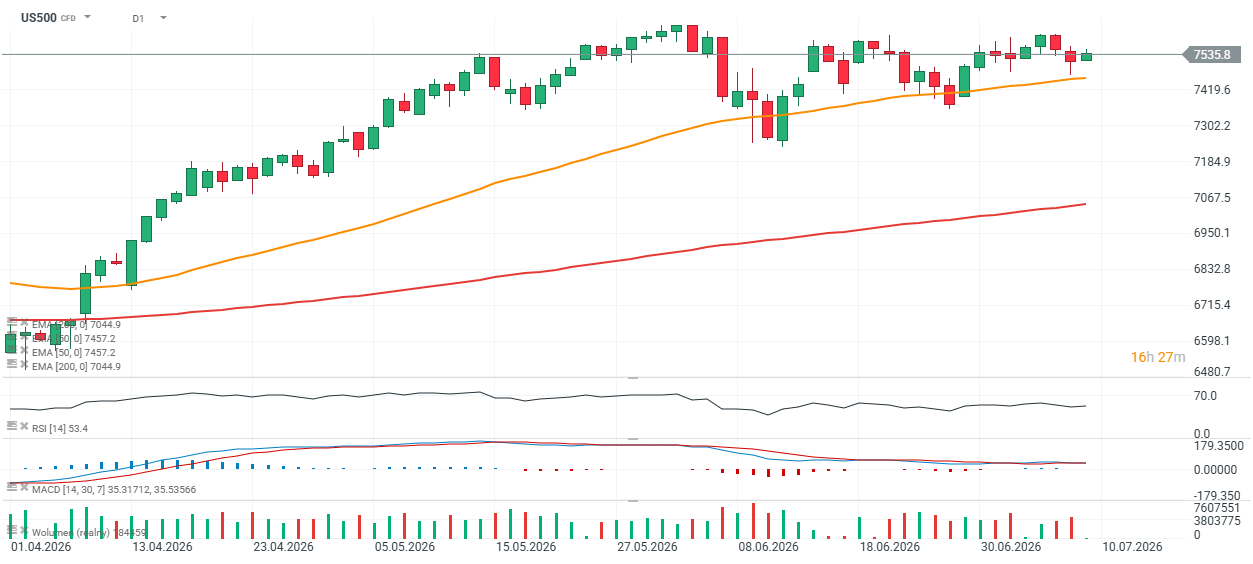

US 500 (D1 chart)

S&P 500 futures have once again rebounded from the 50-day exponential moving average (EMA50, orange line), which provided support during yesterday's session. During the two stronger corrective moves in June, the benchmark briefly traded below this level before recovering. The key support remains around 7,460 points, while the nearest resistance is defined by the recent local highs near 7,650 points.

Source: xStation 5

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

⬆️TTF gas rises over 6% near 58 EUR

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.