Henry Hub natural gas (NATGAS) contracts are falling to their lowest levels since late autumn last year, testing a key technical support area near $2.95. While forecasts point to significant heat building over the next 10 days, demand remains muted due to currently mild conditions across most of the United States. More importantly, strong domestic supply and elevated storage levels continue to weigh on market sentiment, offsetting both rising LNG exports and weather-driven demand projections.

Prices are now hovering near the critical technical level of $2.972, and a decisive breakdown below it could pave the way for deeper declines — potentially toward $2.885, a price zone not visited in several months.

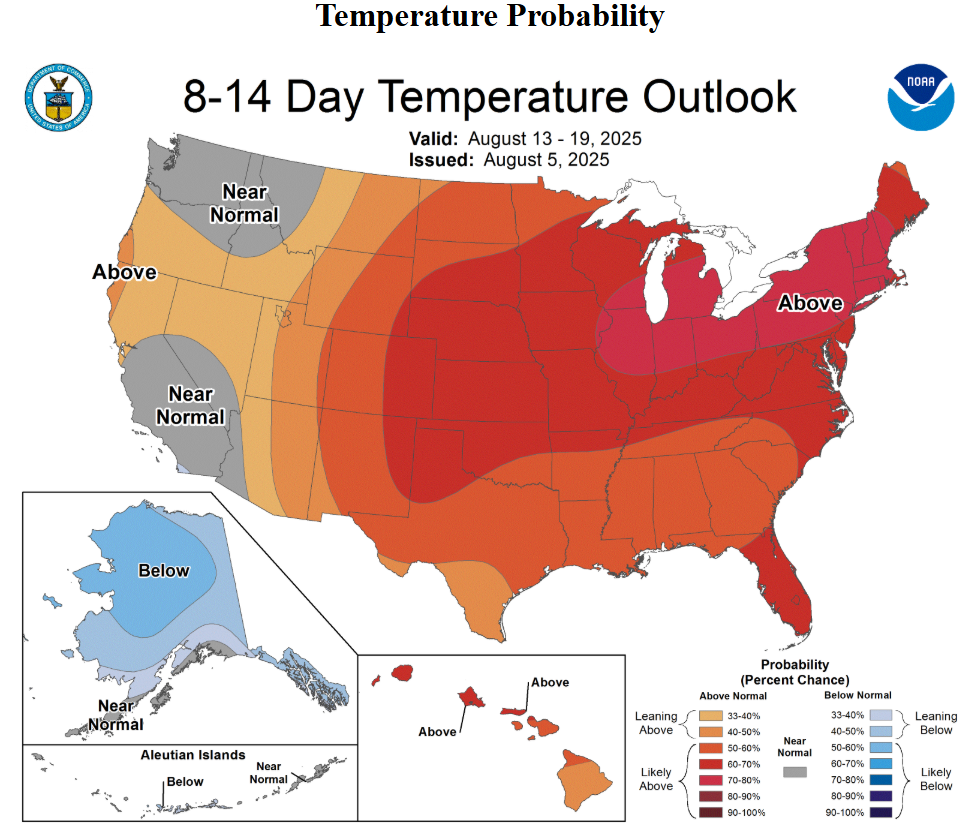

Despite meteorological models predicting a heatwave between August 9–17, with widespread temperatures in the 90s and 100s °F (30–40°C), current conditions remain too mild to spark significant cooling-related gas demand. Much of the U.S. is experiencing seasonally moderate temperatures, with limited air-conditioning loads outside the Southern states and California.

-

A stronger uptick in electricity demand is expected later in the week, driven by the South and West Coast.

-

For now, near-term weather remains a weak catalyst, and futures markets are showing clear skepticism, signaling a lack of conviction that the heat will be long-lasting or impactful enough to shift fundamentals.

Source: NOAA, CPC

Supply Continues to Dominate the Narrative

Fundamentally, production growth continues to outpace consumption in the U.S., even with the usual summer fluctuations. According to recent data (August 1), dry gas output in the Lower 48 reached 108.1 billion cubic feet per day (Bcf/d) — up 3.4% year-over-year.

Meanwhile, total U.S. gas demand has fallen to 76.1 Bcf/d, marking a steep 13% year-over-year decline. This widening imbalance continues to pressurize prices.

-

LNG exports have improved, climbing to 15.2 Bcf/d, and while that provides some relief, it’s insufficient to balance the market in light of strong domestic supply.

-

Baker Hughes reported an increase of two active gas rigs last week, bringing the total to 124 — the highest in two years, reflecting producer confidence and expectations of sustained upstream activity.

-

U.S. regulatory policy is also leaning toward encouraging continued production, adding to the oversupply picture.

Storage Builds Reinforce Bearish Momentum

Further downside pressure came from last Thursday’s EIA storage report, which indicated a +48 Bcf injection for the week ending July 25 — well above the market consensus of +41 Bcf and nearly double the five-year seasonal average of +24 Bcf.

-

Current inventories now stand 6.7% above the five-year average, though still 3.9% below last year’s levels.

-

While total U.S. power generation was up 8.1% year-over-year, the bullish impact of that data was muted by the overwhelming supply and inventory narrative.

NATGAS (D1 Chart)

From a technical perspective, weather may hint at a bullish setup, especially across the Central and Eastern U.S., but the market is pricing fundamentals not forecasts. The prevailing sentiment remains that oversupply is the dominant force, and price action reflects that reality.

-

The RSI on the daily chart approaches oversold territory, hinting at possible short-term exhaustion among sellers.

-

Resistance levels remain clearly defined at $3.14 (recent price reaction zone) and $3.38 (Fibonacci retracement).

-

A sustained drop below $2.90 could open the door to a deeper correction, extending bearish momentum into late summer (before the seasonality catalysts).

The natural gas market remains pinned down by structural oversupply, even as short-term weather forecasts promise stronger demand. With production running at near-record levels, LNG export growth unable to absorb the excess, and storage building faster than expected, whether alone may not be enough to turn the tide. Until a structural rebalancing emerges through production cuts, stronger exports, or prolonged heat prices may continue to test the patience of the buyers.

Source: xStation5

Three Markets to Watch Next Week: USDJPY, US500, OIL (01.05.2026)

Market Wrap – Data Confirms BoJ Intervention. Waiting for US ISM (05.01.2026)

Chart of the Day: Intervention on the Yen? Tokyo Challenges Speculators (01.05.2026)

Morning Wrap- Wall Street Records and Oil Stabilization (01.05.2026)

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.