Over recent quarters, a dominant narrative has taken hold on Wall Street that the “Magnificent 7” are driving the bulk of earnings growth across the S&P 500. However, first-quarter 2026 data suggest a more nuanced picture. While large technology companies continue to grow faster than the broader market, FactSet indicates that this advantage largely disappears once Nvidia is excluded. This is an important signal for investors, as it shows that the strength of this group is not as broad as it may appear.

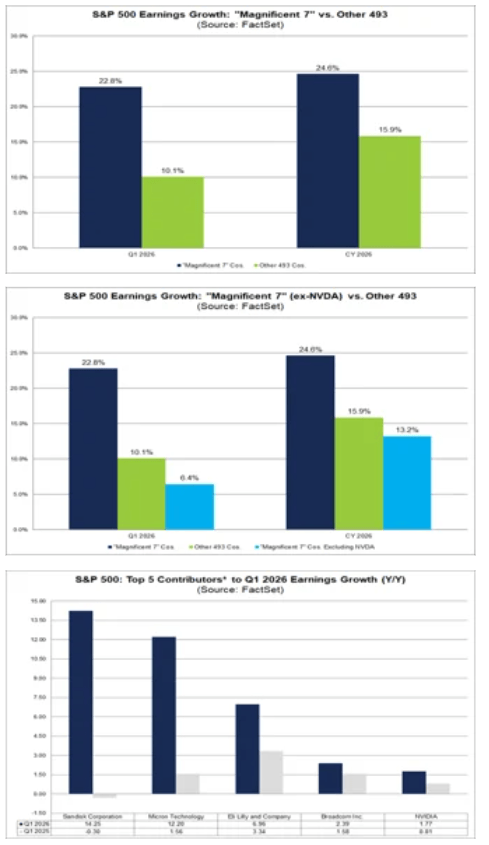

On an aggregate basis, the “Magnificent 7” still outpace the rest of the index

Estimates for the first quarter of 2026 suggest that the “Magnificent 7” will deliver earnings growth of 22.8% year over year. By comparison, the remaining 493 companies in the S&P 500 are expected to post growth of 10.1%. On a headline level, the largest technology firms still appear to hold a clear advantage.

This aligns with trends seen in previous quarters, when the seven largest technology names accounted for a disproportionately large share of total index earnings growth. The issue is that this seemingly broad dominance is now increasingly driven by a single company.

Nvidia is the key driver of earnings growth not only within the “Mag 7,” but across the entire S&P 500

The most important takeaway from the data is straightforward: Nvidia remains the largest single contributor to earnings growth both within the “Magnificent 7” and across the S&P 500. It accounts for a significant portion of the gap between megacap tech performance and the rest of the market.

Excluding Nvidia, projected earnings growth for the “Magnificent 7” in Q1 2026 drops from 22.8% to just 6.4%. This implies that without Nvidia, the rest of the group would actually grow more slowly than the broader index, which is expected to expand by 10.1%. In other words, the outperformance of the “Magnificent 7” becomes far less convincing once the largest beneficiary of the AI boom is removed from the equation.

The rest of the market may not be as weak as the dominant narrative suggests

This is where the interpretation begins to shift. For some time, markets have operated under the assumption that earnings growth is largely concentrated in a handful of large technology companies. However, the data suggest that once Nvidia is excluded, the remaining 493 S&P 500 companies are growing faster than the rest of the “Magnificent 7.”

This is not just a statistical detail. It indicates that earnings growth may be gradually broadening beyond the most obvious names. Among the next-largest contributors to S&P 500 earnings growth after Nvidia are Micron Technology, Eli Lilly, Broadcom, and Sandisk. This alone suggests that the market story is no longer limited to a small group of technology giants.

Source: XTB Research

The same pattern holds for full-year 2026 estimates

The full-year outlook reinforces this dynamic. For calendar year 2026, the “Magnificent 7” are expected to deliver earnings growth of 24.6%, while the remaining 493 S&P 500 companies are projected to grow by 15.9%. At first glance, the advantage again appears substantial.

However, Nvidia once again plays a decisive role. Excluding the company, projected earnings growth for the “Magnificent 7” drops to 13.2%, below the expected growth rate for the rest of the market. This suggests that even over a longer horizon, the group’s advantage is less broad than headline figures imply.

Concentration of growth is becoming a growing risk for the market

From an investor perspective, the key takeaway is that earnings growth in US equities is becoming increasingly concentrated. When a single company accounts for such a large share of overall improvement, the market becomes more vulnerable to disappointment.

This is particularly relevant in an environment where valuations of large technology companies remain elevated and expectations are high. The more growth is concentrated in one name, the greater the risk that weaker results or more cautious guidance could trigger a broader shift in sentiment.

Nvidia’s performance and market implications

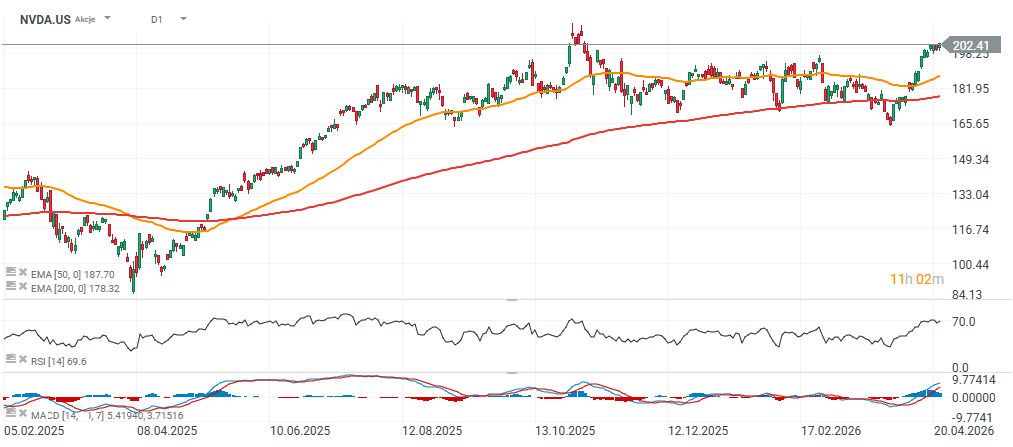

The simplest conclusion is this: the “Magnificent 7” still appear strong, but their strength is increasingly a story about Nvidia rather than broad-based dominance across the group. This does not mean the remaining companies are weak. It does mean that their advantage over the rest of the market is no longer as clear. For investors, this represents an important shift in perspective. Rather than treating the “Magnificent 7” as a uniform growth block, there is a growing need to analyze individual companies more closely. First-quarter data and full-year 2026 forecasts clearly show that without Nvidia, the narrative of overwhelming dominance begins to weaken. Nvidia shares are trading above $200 and have moved roughly 8% above the 200-day EMA (red line), increasing the likelihood of a breakout above the previous highs seen in autumn 2025.

Source: xStation5

Market wrap: ASML and Infineon support sentiments in Europe

PDD shares plunge over 7% following earnings report⏰

Nvidia and 150 Billion Reasons Why Taiwan Is Becoming the Center of the AI World

Space stocks surge as Wall Street awaits SpaceX IPO 📈

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.