Rivian is a (still) new, relatively small player in the e-mobility market, yet with enormous potential. Are the risks facing the company just as enormous?

Electric vehicles, regardless of individual investors’ personal attitude toward them, will remain an indispensable part of automotive and transportation for many years, if not decades. The rivalry between Tesla, BYD, and traditional automotive companies is at the center of market interest and research. However, despite the scale of these players and the intensity of their competition, it does not mean that everything has already been said when it comes to business models.

Both Tesla and BYD are focused on chasing economies of scale, which pushes margins in the sector to new lows, forces costly investments, and fuels price wars. Traditional car manufacturers, both in the U.S. and Europe, clearly struggle to “re-tool” their factories, model lineups, dealerships, and design departments for electric cars. In this context, Rivian’s “incremental” approach is a breath of fresh air in the industry and in the market. Innovations in production technology, management, and materials allow even relatively small companies to compete with massive conglomerates, something that would have been difficult to imagine just a dozen or so years ago.

The upcoming launch of the company’s “R2” model is, in the view of many analysts and investors, a “make-or-break” moment for the company, and for good reason. The R2 can be viewed from two perspectives. On the one hand, it represents a departure from the company’s previous imperative: lightness and efficiency. On the other hand, it is a step toward scalability and growth, which is essential if the company is to become more than a market curiosity.

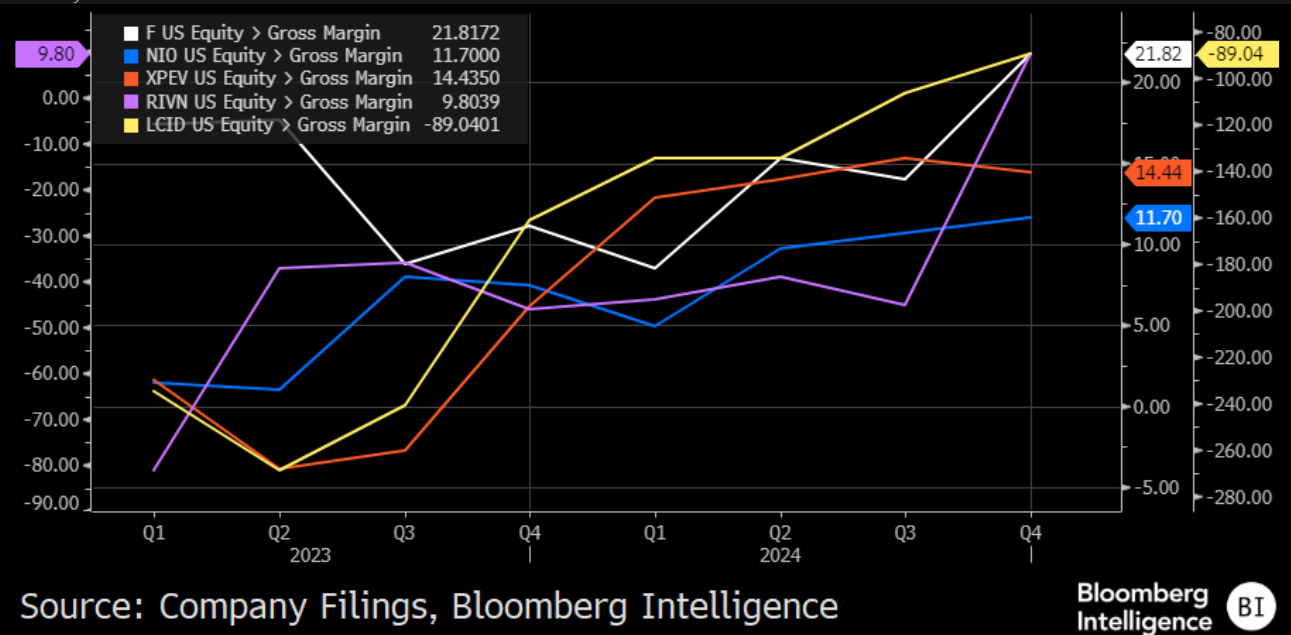

As of today, the company has a number of industry-unique solutions, proprietary components, and software that can compete with industry leaders despite only a fraction of the costs it incurs for development and production. Vertical integration of systems and solutions, as well as platformization, also give the company an edge it desperately needs in an ultra-competitive market.

Source: Bloomberg Finance L.P.

What also gives the company an advantage, one that does not seem to be fully priced in by the market, is its recent agreement with Uber. Considering the potential to supply vehicles to the ride-hailing market’s hegemon, as well as the recent joint venture with Volkswagen, Tesla may find itself in a situation where Rivian “skips a few steps” and begins monetizing robotaxis while bypassing most of the problems Elon Musk’s company is struggling with.

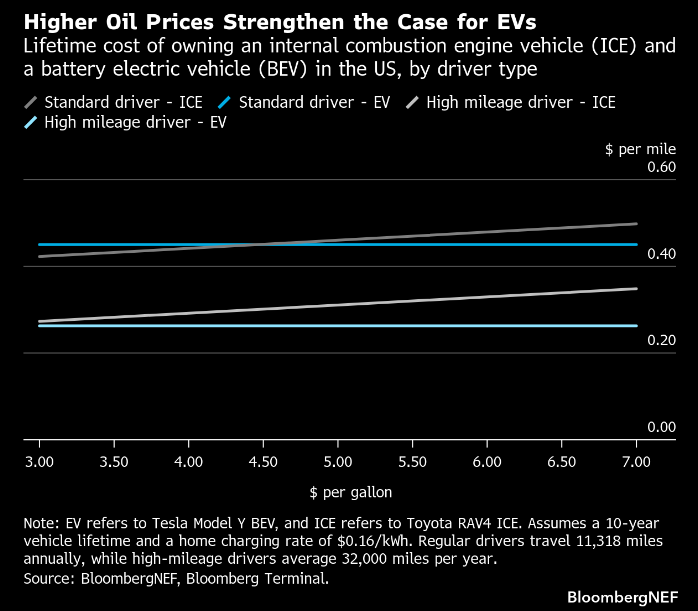

Source: Bloomberg Finance L.P.

Additional support for Rivian is the hard-to-ignore rise in fuel prices. The oil market is not able to wean itself off, or even meaningfully reduce, its dependence on the Middle East, but the global economy can significantly reduce its dependence on oil. The price of gasoline in the U.S. has risen by around 30% over the past month. With Elon Musk’s nearly permanent reputational crisis among current and potential EV owners

in mind, high fuel prices may give Rivian a chance to capture a meaningful share of the market at the best possible moment, especially with the R2 launch ahead.

However, the company still faces a number of risks, not just opportunities. As of today, it is still not profitable—although the trend is strongly improving. The company promises significant growth in financial metrics, and the data partially supports these intentions, but it is worth asking:

- How much of this growth is already priced in (if at all)?

- How likely is it that the company will deliver such an ambitious expansion scenario in such a difficult market?

Investors, both current and prospective, will be looking for answers to these questions during the company’s earnings call on May 12.

RIVN.US (D1)

The company’s shares have continued a bumpy uptrend since the beginning of 2024. A very important signal is the crossover of the EMA100 and EMA200, which is a strong bullish signal. However, it is worth remembering that the valuation—despite the recent gains—still remains far below the peak levels seen at the IPO in 2021.

US OPEN: The market extends losses as investor concerns grow

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

Worse than the Dot-com bubble: IBM stock crash

Daily Summary - Escalation in the Middle East. FOMC fears inflation

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.