Russia is a key member of the exclusive group of major oil producers, and the hydrocarbon industry has been one of the most important factors shaping the policy of the Russian Federation. The war in Ukraine clearly and emphatically showed that the source of Russia's influence is not its army. This source should be sought in Siberian wells, refineries, and pipelines.

This soft underbelly of the Russian economy has been targeted by Ukraine's armed forces. The campaign of attacks on Russian infrastructure takes on a completely new dimension in light of events in the Persian Gulf and the sudden surge in oil prices. Will Ukrainian drones prove faster than revenues to the Kremlin's budget?

To understand oil is to understand Russia.

Like Russia itself, the oil and gas industry in Russia is a hostage to the country's past. The Soviet oil industry, which the Russian Federation inherited, was born in Baku, in modern-day Azerbaijan. The intensive exploitation of these fields resulted in a deterioration of their quality to an extent that the Soviet industry was unable to address.

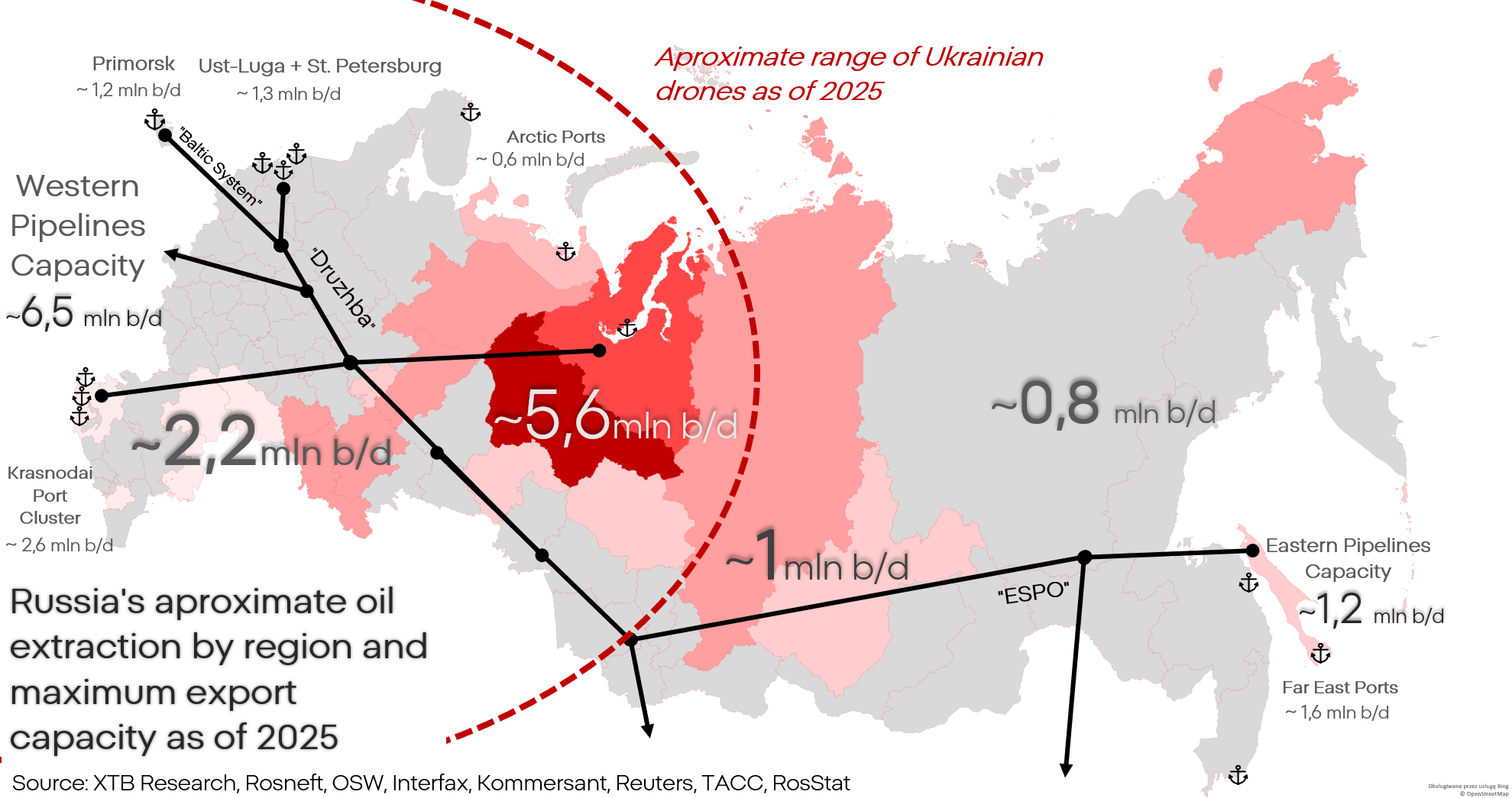

Over time, the center of gravity of oil production in the USSR shifted to Western Siberia—where it remains to this day. This is important because the range of Ukrainian drones is optimized to strike this very region.

The fields of Western Siberia are vast, but extracting them in volumes that would make the venture profitable is challenging. Russian oil is relatively heavy (dense) and sour; this increases both the difficulty and the cost of extraction and refining. Lack of technology and inefficient management during Soviet times led to field degradation, and the USSR's economy eventually became less capable of sustaining this increasingly less profitable oil extraction.

The peak of oil production in Russia occurred in the 1970s, when it reached slightly over 13 million barrels per day. After the collapse of the Soviet Union, production dropped to around 6 million barrels per day; today, this number no longer exceeds 10–11 million.

The degradation of the fields due to exploitation during the USSR forced the Russian Federation to enter into far-reaching cooperation with Western concerns, which provided advanced technology and taught the Russians extraction management. Without companies like SLB, Halliburton, BP, Exxon, Emerson, or Siemens, a poor and backward country like Russia would never have been able to rebuild its production to today's levels.

This creates a vulnerability that the Russians do not want to admit: Russian oil infrastructure was not built by Russians, but by Europeans and Americans. Cut off from service, software, and spare parts, it will gradually degrade. This could be observed, for example, in Venezuela or Iran, although there the process lasted not years, but decades.

Technical problems in the Russian oil industry can be partially cushioned thanks to cooperation with China and India, but the Russian industry is de facto a Western industry with a Russian flag attached—incompatible with Asian solutions. A comprehensive solution to the problem would require the replacement of almost the entire system and infrastructure.

In addition to the process of technical degradation, the Russian industry must contend with cyclical attacks by Ukrainian drones that physically destroy valuable and difficult-to-replace machinery.

The word "degradation" is key here. Ukraine's goal is not a decapitating strike but an asymmetric campaign that will inflict relatively small yet cumulative losses.

What, however, is the intended nature of these losses?

Over 30% of Russian exports consist of crude oil, and fossil fuels or their semi-finished products account for over 50% of the total. However, crude oil is not the most profitable product: the most economical product manufactured from Russian oil is diesel. This is due to the viscosity and sulfur compound content in Russian oil. Observing the production and export of Russian crude oil, it is difficult to spot the devastating impact of sanctions or the collapse of the entire industry on the chart, however, contrary to popular opinion, this was never the goal of the sanctions.

Russia was not supposed to stop producing oil; Russia was supposed to earn less from it. This intention has been partially achieved, while the raw material market has stabilized after the 2022 crisis.

Observing data on both budget revenues and volumes, it can be seen that the extraction and export of crude oil remained almost unchanged during the analyzed period. The volume of extraction fell by only 2–3%, and exports increased by about 3%.

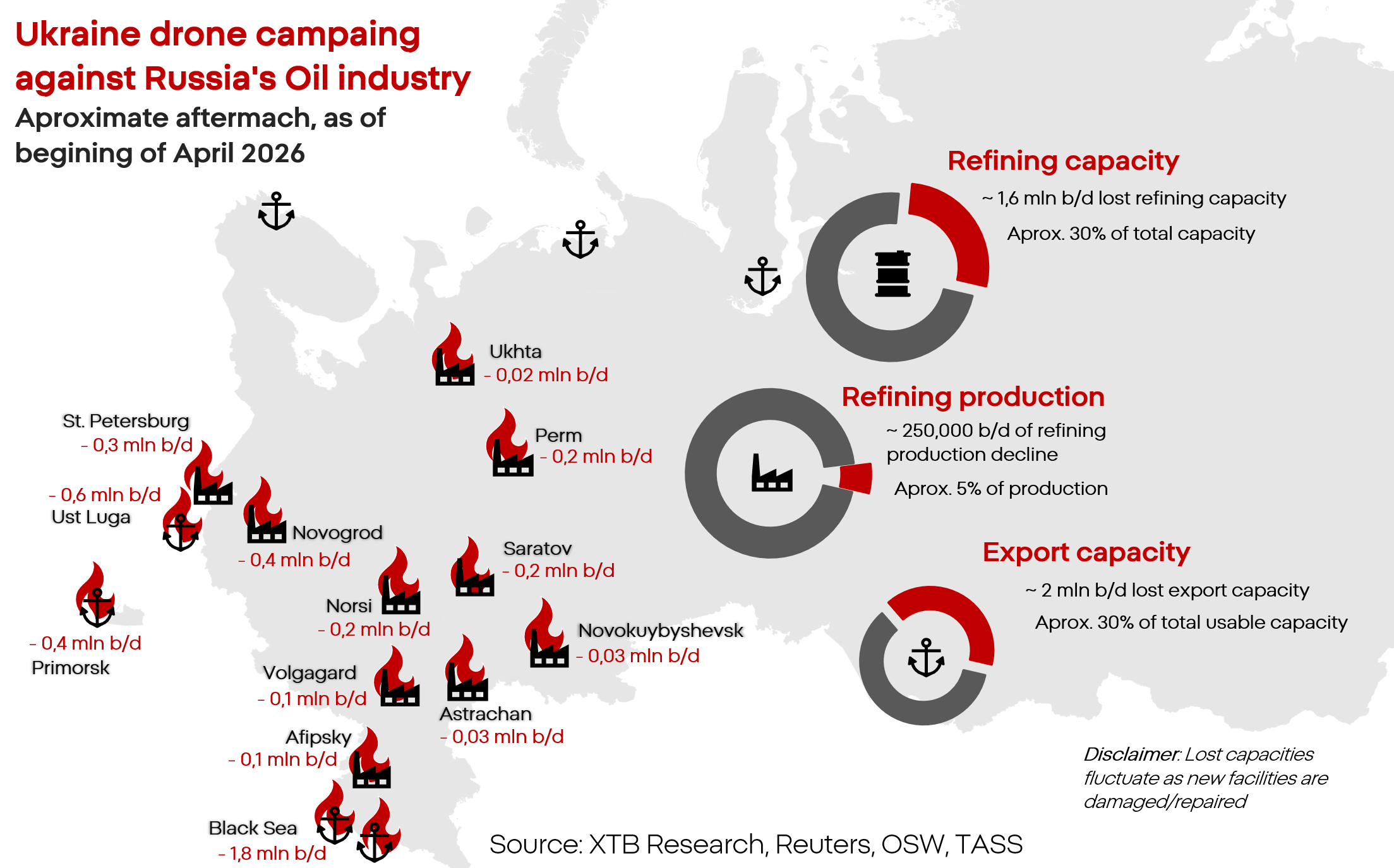

The Ukrainian drone attack campaign is intended to address the more profitable and vulnerable part of the oil industry—refining. When attacking Russian infrastructure, Ukraine usually does not strike extraction infrastructure because it is simply inefficient. It focuses on striking the bottlenecks of refining and fuel exports—which are easier to hit, harder to repair, and whose temporary shutdown is much more costly for the Russian economy and budget.

Due to the optimization of the refining process for specific types of oil, Russia has a huge overproduction of diesel, which it exports and which powers the most economically critical vehicles, including military ones. At the same time, the production of less critical but still necessary gasoline is almost "just enough." This is the real weak point targeted by Ukraine.

At the same time, refinery production fell by 7%, and exports by as much as 12%.

Here, we need to address the frequently cited figures stating that Ukrainian strikes disabled over 30% of the total processing capacity of Russian refineries. How is it possible that production fell by "only" 7%?

Russia has huge buffers of production capacity. The total processing capacity of Russian refineries is estimated at up to 6 million barrels of oil per day; however, Russia currently uses only about 4.5 million. By disabling even ⅓ of the infrastructure, Russia still has the hypothetical ability to redirect production elsewhere while repairs and firefighting operations are ongoing at the affected plants.

However, this does not mean that the impact of these attacks is not visible. The first downtimes and shortages are already appearing at this level, with a missing processing capacity in the range of 0.2–0.5 million barrels per day.

Furthermore, many facilities are damaged to an extent that prevents repair. Redirections are time-consuming and costly, and not always physically possible. In addition, Russian refineries were built with the primary goal of serving the local market—a damaged or destroyed refinery paralyzes the local fuel market.

Budgetary perspective

The value of Russian crude oil exports fell to levels lower than before the war, by just under 10%. However, the decline in exports of processed products is already over 40%.

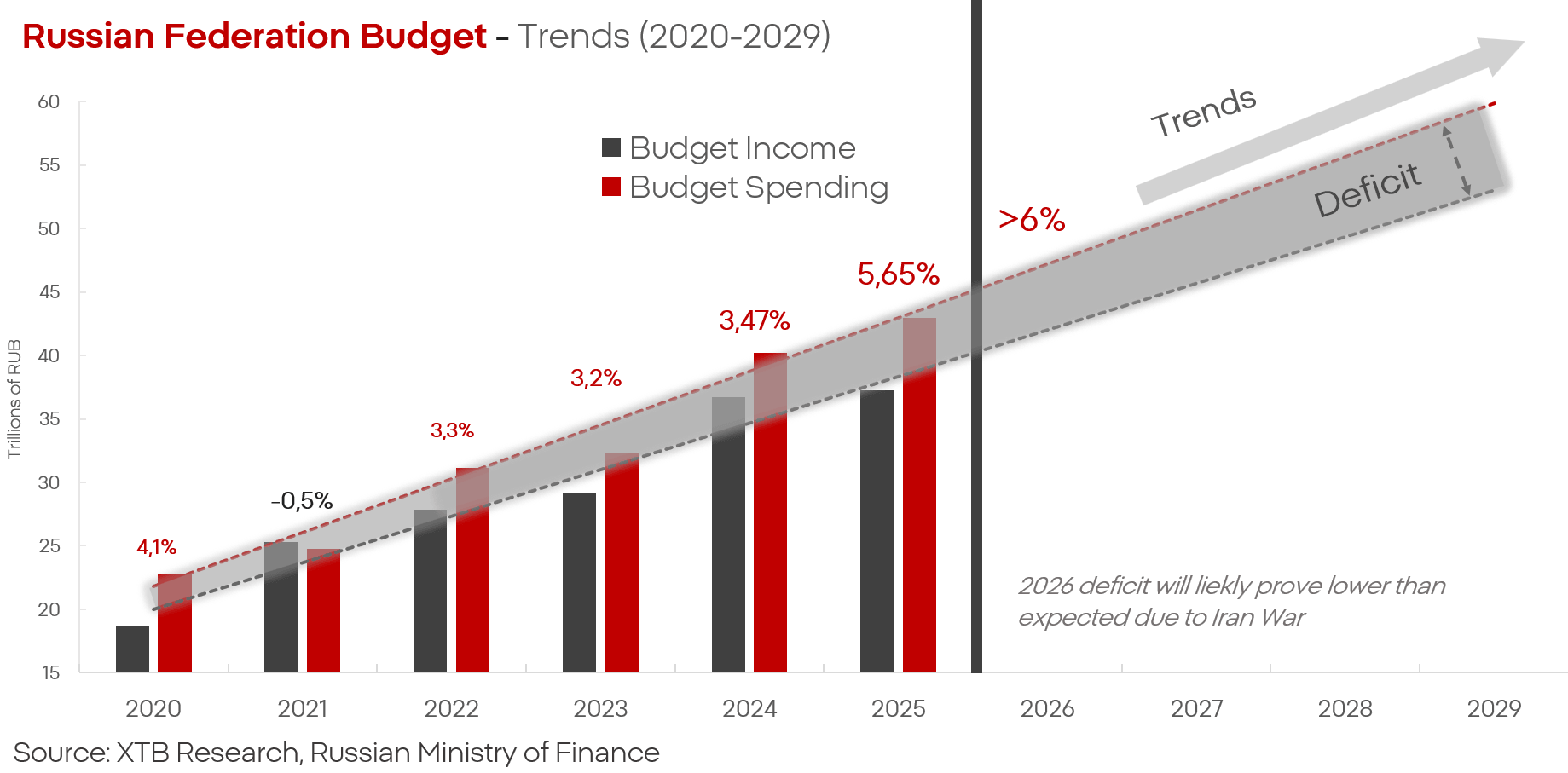

Russia's federal budget for 2025 is 41.5 trillion rubles (approx. 415 billion USD). Military spending is 13.2 trillion rubles, and internal security is another approx. 4.5 trillion rubles. This means that "defense" and "security" alone, which in practical terms means war and repression - cost Russia over 40% of the entire budget.

Budget revenues from the sale of oil and gas, meanwhile, constitute about 20–30% of Russia's budget revenues. The puzzle falls apart without this element. Assuming that the decline in export value will translate into an approximately linear drop in budget revenues, this means a decrease in available funds of around a dozen percent of the budget.

If Ukraine maintains or escalates the campaign against the Russian oil sector, a scenario becomes realistic where Russia will be forced to choose between meeting its own needs (including the front) and meeting the needs of customers, and thus - the budget.

From every ton of oil, Russia is able to produce approx. 300–400 kg of diesel and approx. 150 kg of gasoline.

At the same time, the Russian economy needs approx. 130–140 million tons of fuel annually to function under conditions of relative normalcy.

Keeping in mind the processing capacities of refineries in Russia, this means that Ukraine would have to disable 50–60% of the processing capacity of refineries in the Russian Federation to present Russia with a choice:

Stop military operations due to a lack of fuel in the economy and military;

Reduce budget expenditures by several to tens of percent as a result of limiting fuel exports.

Does the conflict in Iran change the situation? Partially.

The rise in oil prices on world markets and the high degree of dependence of local consumers in Asia on the raw material are visible in the Russian balance sheet. The price of Urals oil rose from around 60 USD per barrel to over 90 USD, an increase of over 50%. The dramatic situation on the oil market makes Russian oil much more attractive. However, this increase may only be price-related, not volume-related. Why?

Russian transmission infrastructure is severely limited. Transneft, the operator of Russian pipelines, controls approx. 67 thousand km of pipelines, but the vast majority of them were built with export to Europe and (now former) "people"s democracy" countries in mind. The greatest demand for oil and fuels today is in Asia, and the pipelines and transshipment terminals there are already operating at maximum capacity.

In the face of the conflict in the Middle East and the global increase in raw material prices, Ukraine's goal has become the additional limitation of Russia's oil export and transmission capabilities. Large attacks on ports and refineries in Ust-Luga and Tuapse, which are key arteries not only for production but also for export, were part of this strategy.

The enormous rise in oil prices is only a partial respite for the Russian budget. Despite a revenue increase from exports in March of approx. 40%, it still meant a drop of nearly half compared to the analogous period a year earlier. The indicators for April look better for Russia: an increase to 19 billion USD means a growth of approx. 100%. However, considering historical data and context, this is most likely a temporary increase, and revenues have their "ceiling" in the form of logistical capabilities for export.

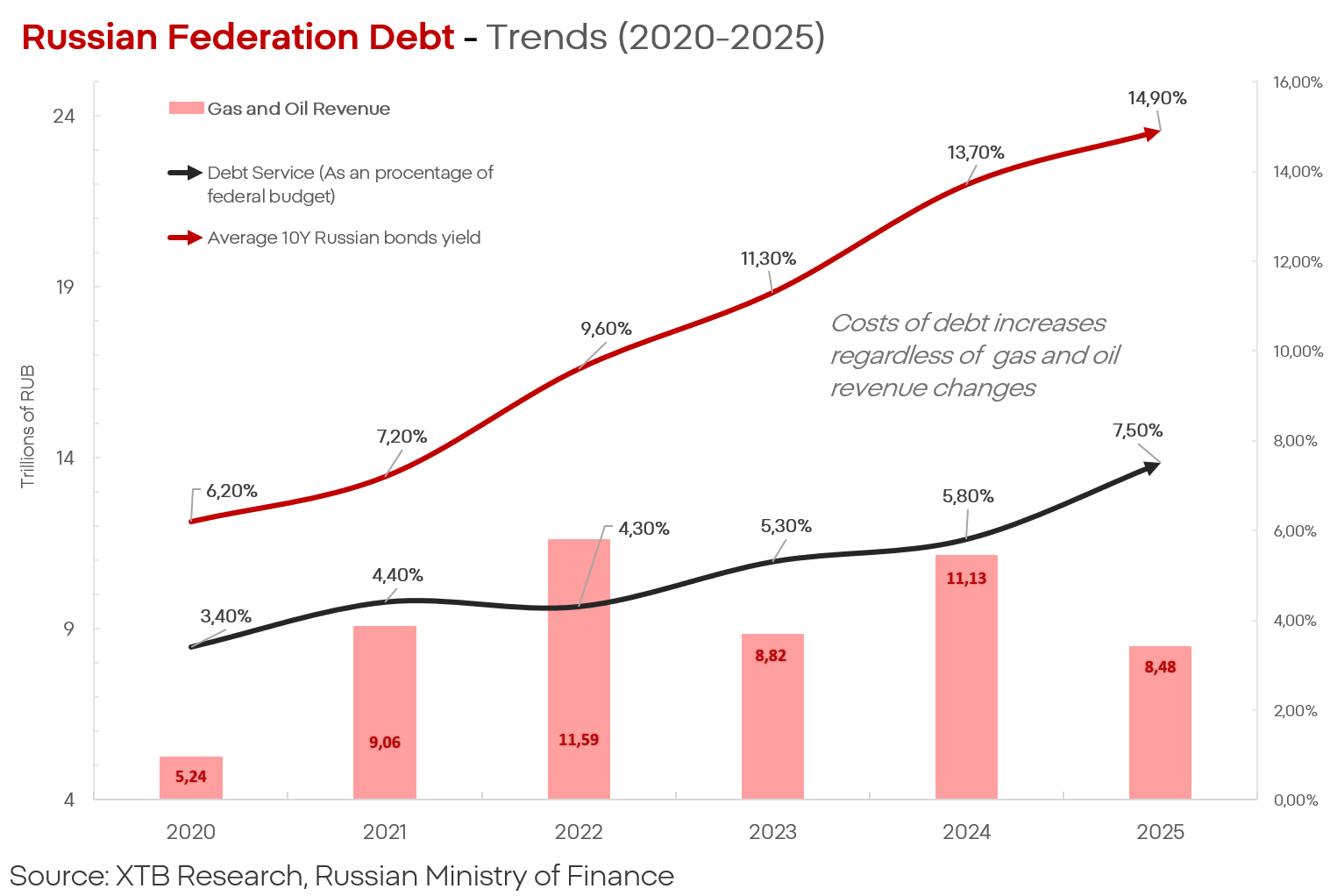

These revenues are also, by their nature, not permanent. Their impact on the Russian budget and the debt, which is becoming an increasing burden for Russia, is also not permanent, despite huge surplus profits in 2022 and realistically operating schemes bypassing sanctions in 2024, the cost of debt service is growing as vertically as the losses on the Ukrainian front.

At the same time, Reuters sources indicate that Russia has begun to distinctly limit both extraction and export. In April, oil extraction was supposed to fall to 8.5 million barrels per day, and exports to 4.1 million. If these estimates are correct, it means that oil production in Russia has fallen to levels not seen for about 10 years—despite record prices and high demand.

Even the Russian Ministry of Economy presents grim prospects, estimating that oil exports are expected to fall to around 200 million tons annually; the ministry itself also admits that there are no prospects for rebuilding market position in this decade.

This means that the war in Iran is powerful support for Russia, but if the trends continue, even this will not be enough to halt the persistently negative trend in which the country's economy, industry, and budget find themselves.

Kamil Szczepański

Financial Market Analyst XTB

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

Fed Chair Kevin Warsh’s Q&A from Congress Testimony: Inflation stability is a key

Bypassing Hormuz: Gulf States Race Against Time

Warsh's Address to Congress: Zero Tolerance for Inflation, But No Change in Interest Rates?

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.