The UK's economy grew by 0.9% year-over-year in the latest reading, missing both the previous figure and market expectations of 1.1%, while quarterly GDP growth remained unchanged at 0.6%, matching forecasts. In Germany, retail sales surprised to the upside, rising 1.1% month-over-month and 1.8% year-over-year, comfortably beating expectations, while import prices increased 0.7% from the previous month, the current account surplus narrowed to €22.1 billion, and business investment grew 0.9% quarter-over-quarter, in line with forecasts.

UK GDP data — key info

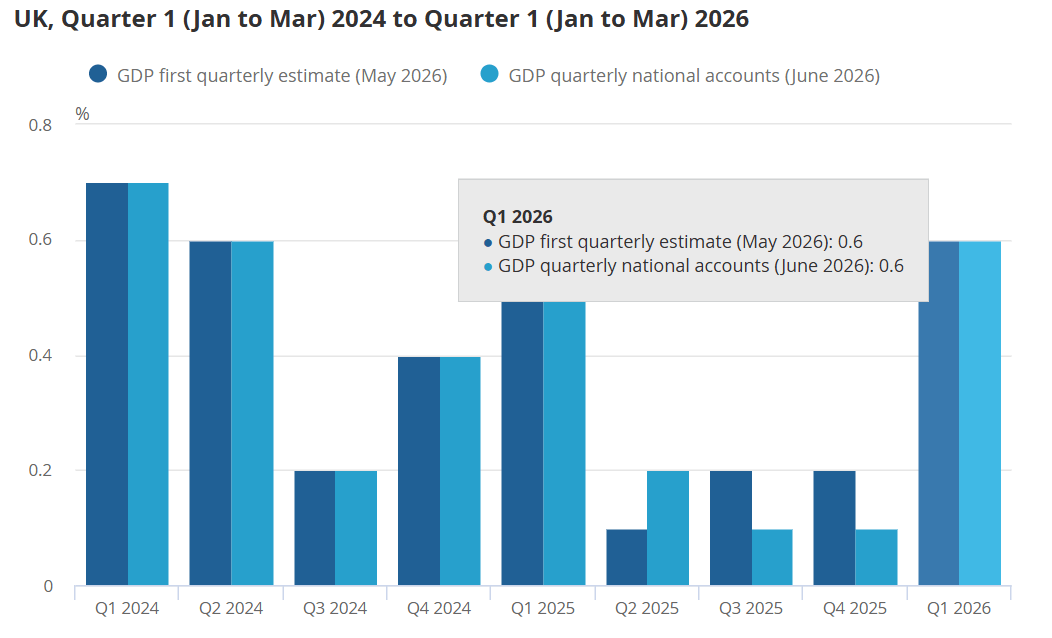

- UK real GDP increased by 0.6% quarter-on-quarter in Q1 2026, confirming the earlier estimate and marking a clear acceleration from the revised 0.1% growth recorded in Q4 2025. The expansion was broad-based, with all three main sectors contributing positively. Services were the main growth engine, rising by 0.8%, which suggests that domestic activity remained resilient at the start of the year.

- Annual GDP growth for 2025 was revised slightly lower to 1.3% from 1.4%, following 1.0% growth in 2024. The revisions were relatively small and mainly reflected updated source data and seasonal adjustment changes.

- Real GDP per head rose by 0.6% in Q1 and was 0.7% higher than a year earlier, pointing to a modest improvement in economic output per person.

- The household picture was less positive. Real household disposable income per head fell by 0.8% in Q1, reversing part of the 1.2% increase seen in Q4 2025, and the household saving ratio also declined, falling by 0.7 percentage points to 8.9%, mainly because of a weaker contribution from non-pension saving.

- Overall, the data show that the UK economy started 2026 on a stronger footing, supported mainly by services. However, weaker household income and lower savings suggest that consumers may remain under pressure despite better headline GDP growth.

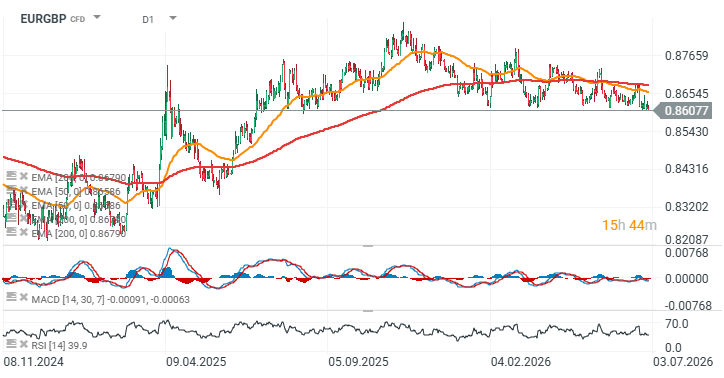

EURGBP chart (D1)

Source: xStation5

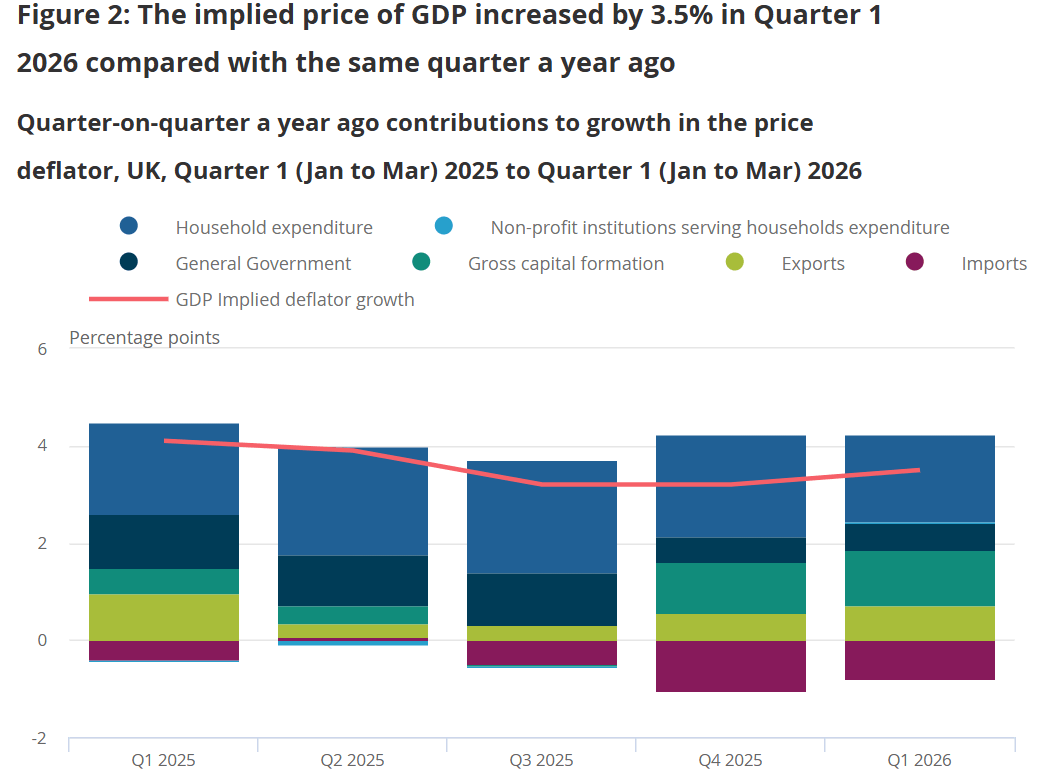

Source: ons.gov.uk

Source: ons.gov.uk

📉 US100 loses 1.5%

EURUSD: Fed Pushback Keeps Dollar Supported Despite Softer Inflation Data

Economic calendar - Europe's Inflation and US Housing Market in Spotlight

Morninga Wrap: Wall Street Under Pressure. AI Loses Momentum, Netflix Disappoints, and the Persian Gulf Erupts

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.