Futures contracts on Wall Street point to a lower opening for the spot market, although the fall is expected to be moderate compared with Asia and Europe.

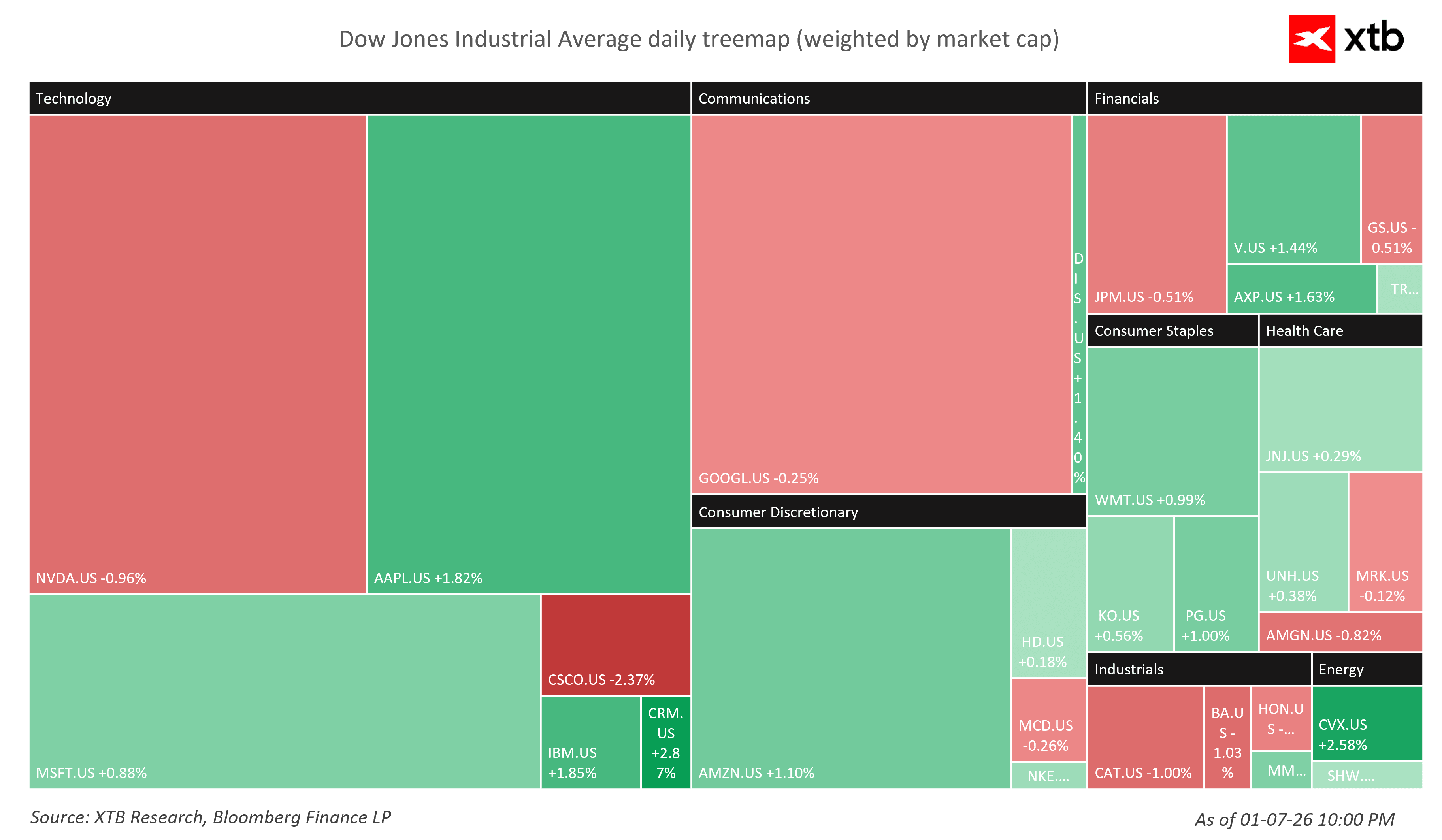

S&P 500 futures are down by around 0.3 per cent, Nasdaq-100 futures are down by as much as 1 per cent, whilst the Dow Jones is holding steady near its benchmark levels.

The main source of pressure is the renewed escalation of the US-Iran conflict over the Strait of Hormuz, following further exchanges of strikes between the two sides over the weekend and Tehran’s announcement that it was ‘closing’ the strait until further notice.

The US responded with strikes on more than 140 targets in Iran, including the first-ever use of naval combat drones, whilst Iran fired on US bases in Kuwait, Bahrain, Jordan, Oman and Qatar.

President Trump has announced that the US will now “police” the straits and expects to be financially compensated for doing so, which further underlines the enduring nature of the American military presence in the region.

Brent and WTI crude are up by more than 3% at the open, rebounding from their session lows, as tanker traffic through the strait has slowed dramatically in recent days.

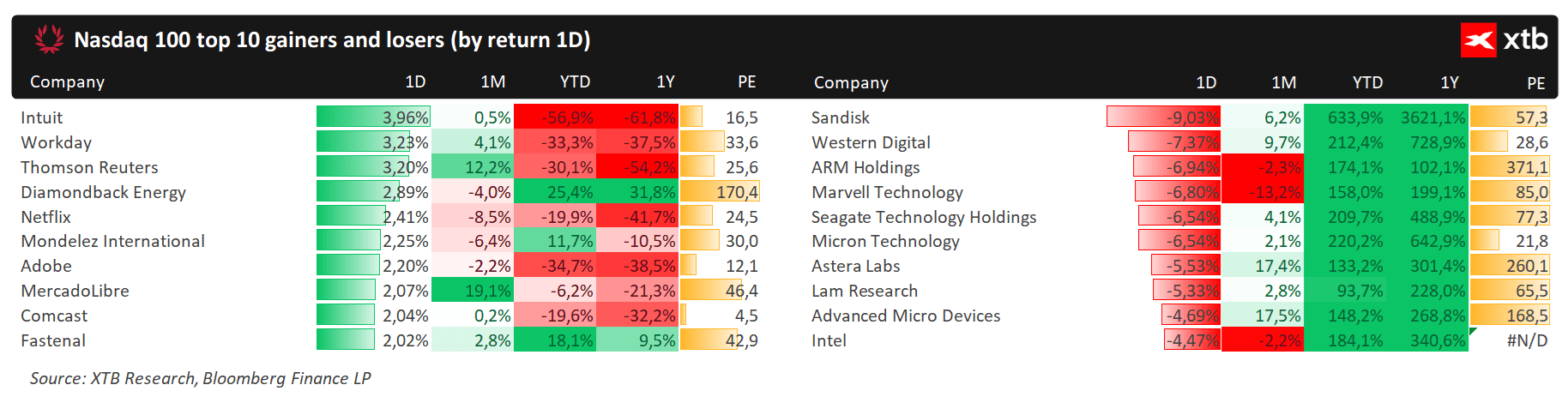

Adding to the pressure on the market is the re-evaluation of so-called AI trading following SK Hynix’s massive but extremely volatile debut on the Nasdaq on Friday.

The energy and commodities sectors are performing best, benefiting from higher oil prices, whilst technology and semiconductor companies are faring the worst, dragged down by a sell-off in memory and AI chips.

Precious metals are losing ground – gold and silver are falling, which is unusual given the current geopolitical tensions and suggests that investors are concerned the Fed will keep interest rates higher for longer following tomorrow’s CPI reading.

Company information

-

SK Hynix (SKHY) – the company’s US ADRs are falling by as much as 8–10 per cent today following Friday’s debut on the Nasdaq, when the shares soared by almost 13 per cent; trading in Seoul plummeted by over 15 per cent – the worst session in the company’s history – as investors took profits following a year-long rally fuelled by the boom in HBM memory for AI.

-

The memory and chip sector – the Roundhill Memory (DRAM) ETF is down by as much as 9 per cent, SanDisk is down 5.5 per cent, Western Digital and Micron Technology are both down 5 per cent, whilst the iShares Semiconductor ETF (SOXX) is down 2 per cent, dragged down in part by Intel (-2.5 per cent) and AMD (-2 per cent) – the market is once again testing the valuations of AI-related companies following a long period of euphoria.

-

TSMC – the Taiwanese contract chip manufacturing giant – reported a 68 per cent year-on-year increase in revenue in June, exceeding the upper end of forecasts, which confirms that demand for AI production capacity remains strong; its shares are up 1 per cent despite generally weak sentiment in the sector.

-

CCC Intelligent Solutions – shares rise by 2% following a Bloomberg report that Elliott Investment Management had built up a significant stake in the company even before talks on a potential sale began.

-

MGM Resorts – shares are up by more than 2 per cent following reports in the Wall Street Journal that the company is in private talks with Barry Diller, to whom People Inc had previously made a takeover bid for the hotel and casino giant back in June.

-

Energy companies – Valero, ConocoPhillips, APA Corporation, ExxonMobil and Chevron – are seeing gains of between 1 and 2 per cent following a surge in oil prices after the weekend’s attacks in the Persian Gulf region.

Morninga Wrap: Wall Street Under Pressure. AI Loses Momentum, Netflix Disappoints, and the Persian Gulf Erupts

Daily Summary: 📉 A Red Day Across Markets. AI Sector Weighs on Wall Street, Precious Metals Under Pressure

Stock of the Week: ASML – The Machines Driving the Future of Semiconductors

Netflix down 45% from its peak 🚩 What will the streaming giant's earnings reveal?

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.