On Friday, U.S. equities are trading lower in reaction to the latest PPI release. The print came in clearly above consensus, immediately reinforcing the narrative of sticky inflation and raising concerns that the Fed may have limited room for near-term easing. The Dow fell 715 points (-1.5%), the S&P 500 dropped 1.1%, and the Nasdaq declined 1.4%. January PPI rose 0.5% m/m (vs. 0.3% expected), while core PPI jumped 0.8% (vs. 0.3%). It was the core component that did most of the damage to sentiment.

Technology and software are once again under pressure, and the market is wrapping up February on a weak note. Adding to the cautious tone, UBS downgraded U.S. equities to “benchmark,” flagging dollar risk, stretched valuations, and political turbulence in Washington. In the background, geopolitical risks are also building: tensions between Pakistan and Afghanistan, the potential for escalation involving Iran, and reports that the U.S. has ordered diplomats and their families to evacuate Israel.

- PPI (U.S. producer inflation): +0.5% m/m vs. +0.3% expected; core PPI +0.8% m/m vs. +0.3% — a strong upside surprise and a clear inflation risk signal.

- Index reaction: Dow -1.5% (-715 pts), S&P 500 -1.1%, Nasdaq -1.4%.

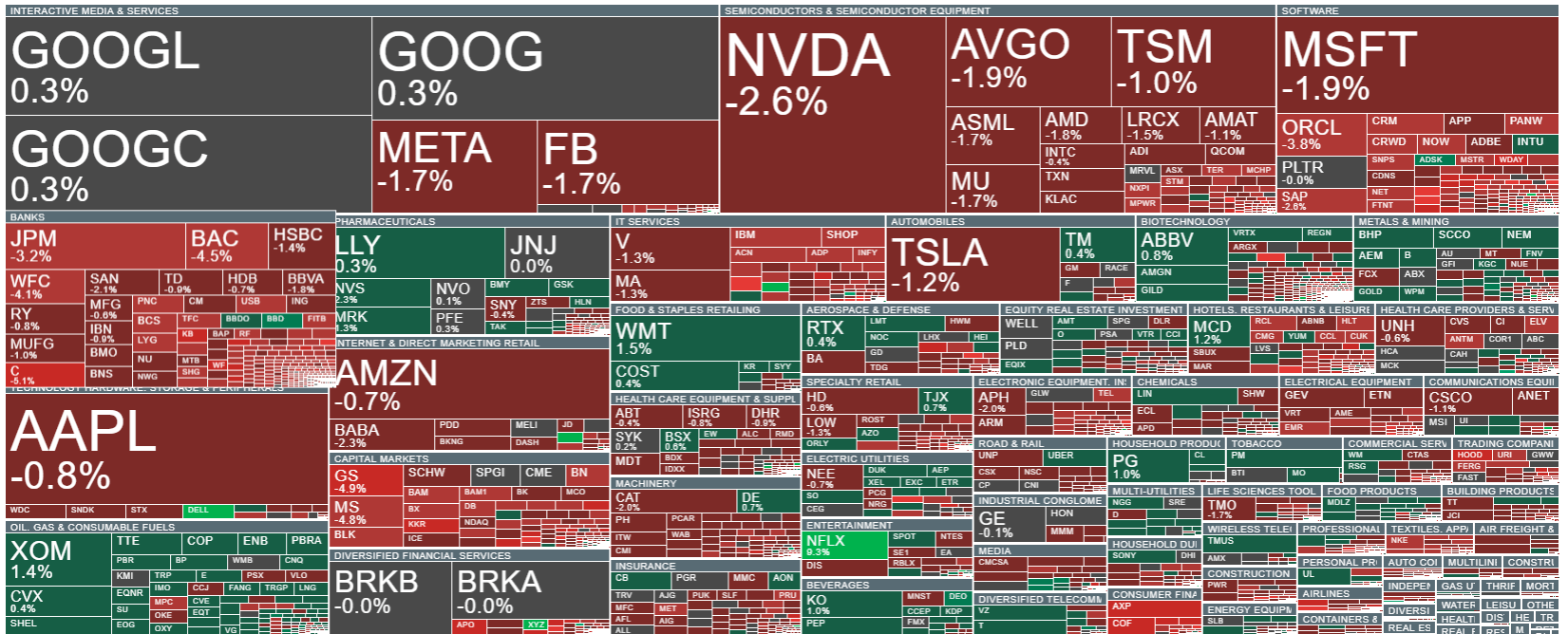

- Tech under pressure again: Nvidia -2% (after more than -5% the previous session), Amazon also weaker — investors are less willing to chase AI hype and OpenAI-related headlines, focusing instead on valuation and risk.

- Software/cybersecurity hit hard: Salesforce -4%, Microsoft около -2%; Zscaler -11% after disappointing results; CoreWeave plunges nearly 20% on weak guidance.

- Sentiment: classic risk-off — investors are cutting exposure first and asking questions later; concerns about AI’s impact on the labor market linger (including major layoffs at Block).

- February wrap-up: Nasdaq on track for a decline of more than 3% m/m; S&P 500 около -1% for the month, Dow around -0.3%.

- UBS on U.S. equities: downgrade to “benchmark,” citing a weaker dollar outlook, elevated valuations, and political turbulence; non-U.S. markets are clearly outperforming in 2026 (MSCI World ex-US up nearly 8% YTD vs. S&P 500 roughly flat).

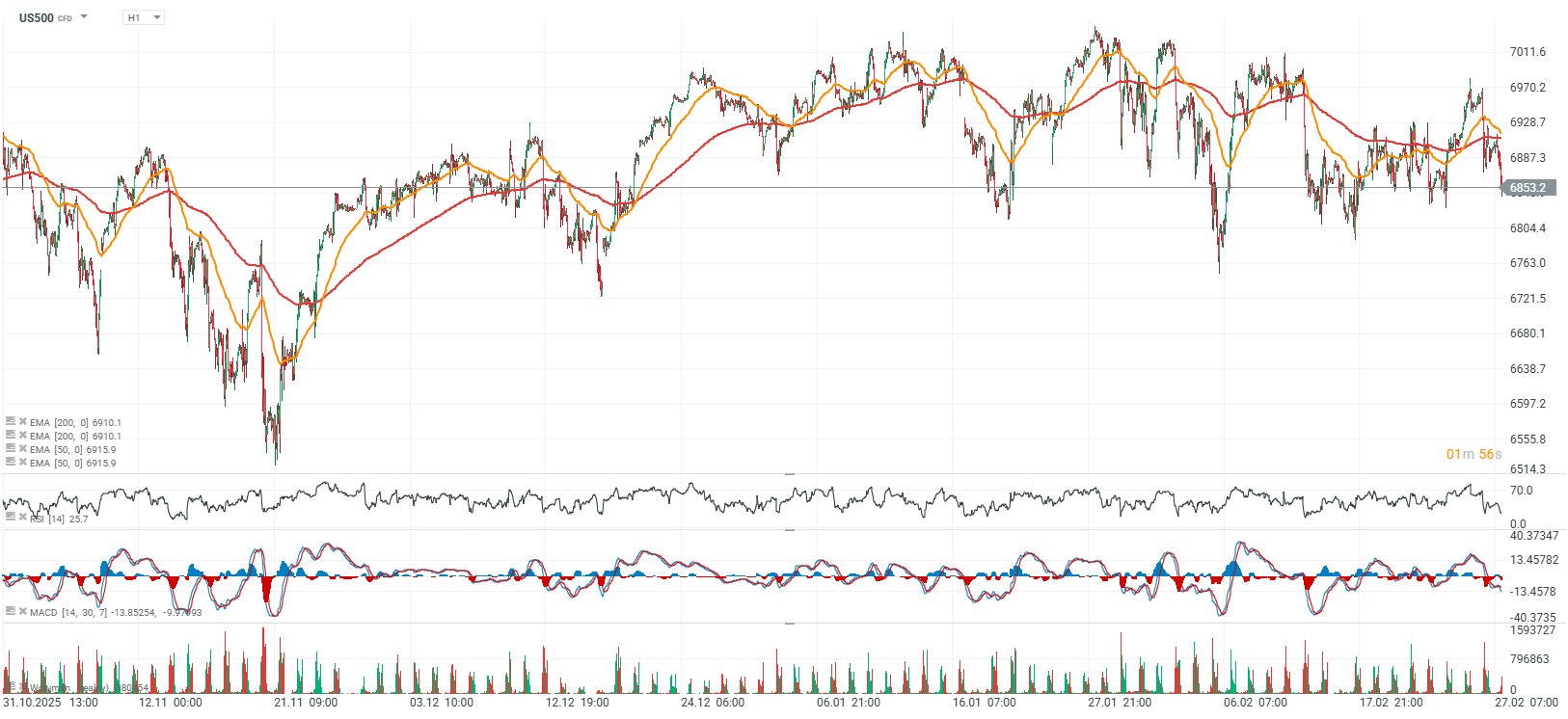

US500 (H1 interval)

Source: xStation5

The financial sector and banks are notably weak today, with concerns centered around private equity exposure and the risk of failures among software companies. Netflix and Dell are among the standouts on the upside. Meanwhile, software and IT services are back under pressure, and Nvidia continues to look technically fragile.

Source: xStation5

Corporate news

Netflix / Warner Bros. / Paramount Skydance: Netflix has walked away from the race to acquire Warner Bros. Discovery, leaving Paramount Skydance to finalize a $111 billion deal. The market welcomed the move — Netflix +8% premarket, WBD -2%, Paramount +9%.

Live Nation: Shares +1% after Rothschild & Co. Redburn upgraded the stock to “buy” and raised its price target to $193 (around 22% upside). Analysts point to stabilization after prior derating, strong demand (Q4 results and guidance), and easing regulatory concerns.

Block: The company announced plans to cut more than 4,000 jobs (around half its workforce). Shares surged 19% in extended trading, with investors interpreting the move as a decisive step toward improving efficiency.

Dollar Tree: Citi downgraded the stock to “neutral” from “buy”; shares -2%. The bank argues that after doubling from its lows and trading close to its price target, the risk/reward is now more balanced despite progress in its multi-price strategy.

Amazon / Big Tech / OpenAI: Following OpenAI’s announcement of a $110 billion funding round (implying a $730 billion pre-money valuation), Big Tech traded lower: Amazon -1%, Microsoft -2%, Meta -1%. Although Amazon is participating in the round and expanding its multi-year partnership with OpenAI, the scale of the valuation and ongoing AI capex appear to be cooling short-term enthusiasm.

Source: xStation5

BREAKING: BoC Leaves No Surprises; Canadian Interest Rates Unchanged 🚨

Bitcoin Looks Cheap, But Is This the Bottom? Crypto Markets Are Waiting for a Catalyst

BREAKING: US CPI data in line with expactations. Monthly CPI Slightly Elevated

Is Inflation Spinning Out of Control?

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.