Wall Street indices are edging higher after Wednesday’s opening bell, supported by gains in the largest technology companies and further signs that inflationary pressure in the US is easing. The S&P 500 is up around 0.4%, the Nasdaq Composite is gaining 0.2%, and the Dow Jones is adding approximately 0.1%. Sentiment improved following weaker-than-expected PPI data and comments from New York Fed President John Williams, who pointed to growing prospects for a further decline in inflation. However, the scale of the advance remains limited by another rise in oil prices after fresh US strikes on targets in Iran. Compared with Nasdaq 100 futures, which are being weighed down by losses among memory-chip stocks, S&P 500 futures are performing noticeably better.

- Tesla is rising around 2%, while Amazon, Apple, Microsoft, and Alphabet are gaining more than 1%, supporting the broader market.

- The US Producer Price Index fell 0.3% month over month in June, compared with expectations for no change, reinforcing the signal from the earlier, cooler-than-expected CPI report.

- The probability of a Fed rate hike in July fell to 17% from 42% a day earlier, although markets still see the possibility of a move in September.

- Investors reacted positively to John Williams’ comments that inflation may have already peaked and should gradually decline over the coming quarters.

- WTI crude is rising around 1% to above $80 per barrel, while Brent is gaining approximately 0.6% and remains above $85 following further US attacks on Iran.

- BlackRock shares are up more than 6% after the asset manager reported better-than-expected quarterly results.

- Despite improving inflation data, the market remains focused on elevated oil prices and the potential inflationary pressure associated with the AI investment boom.

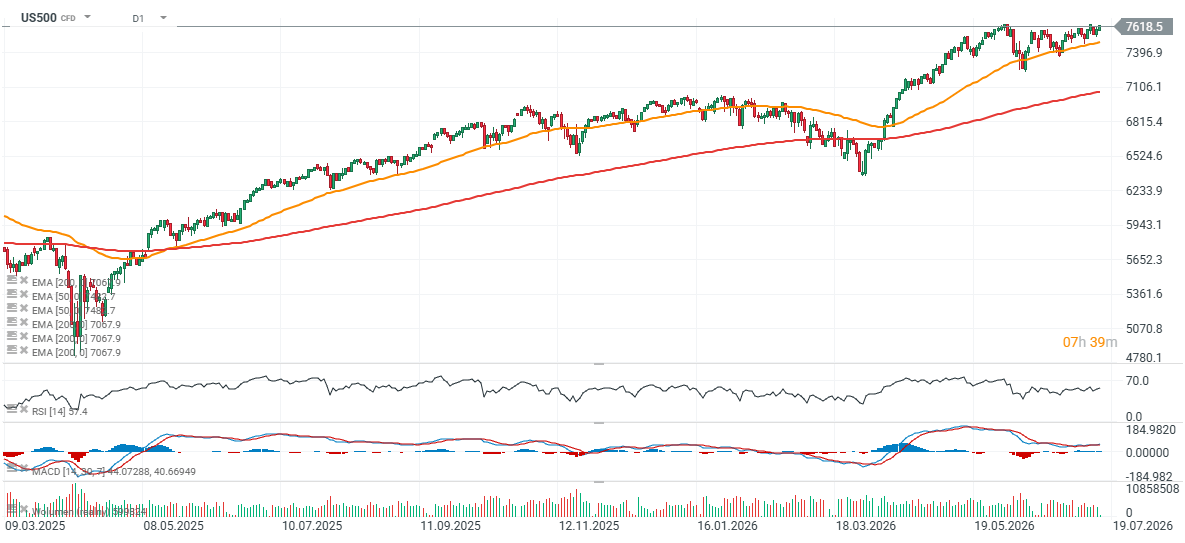

US500 chart (D1 interval)

The contract is rising today to almost 7,620 points, approaching the all-time-high zone despite a pullback in some technology stocks. The key support level remains the 50-day EMA near 7,500 points, while the 200-day EMA is located close to 7,000 points. A breakout above 7,700 points would be crucial for bulls and could open the way toward the 8,000-point level.

Source: xStation5

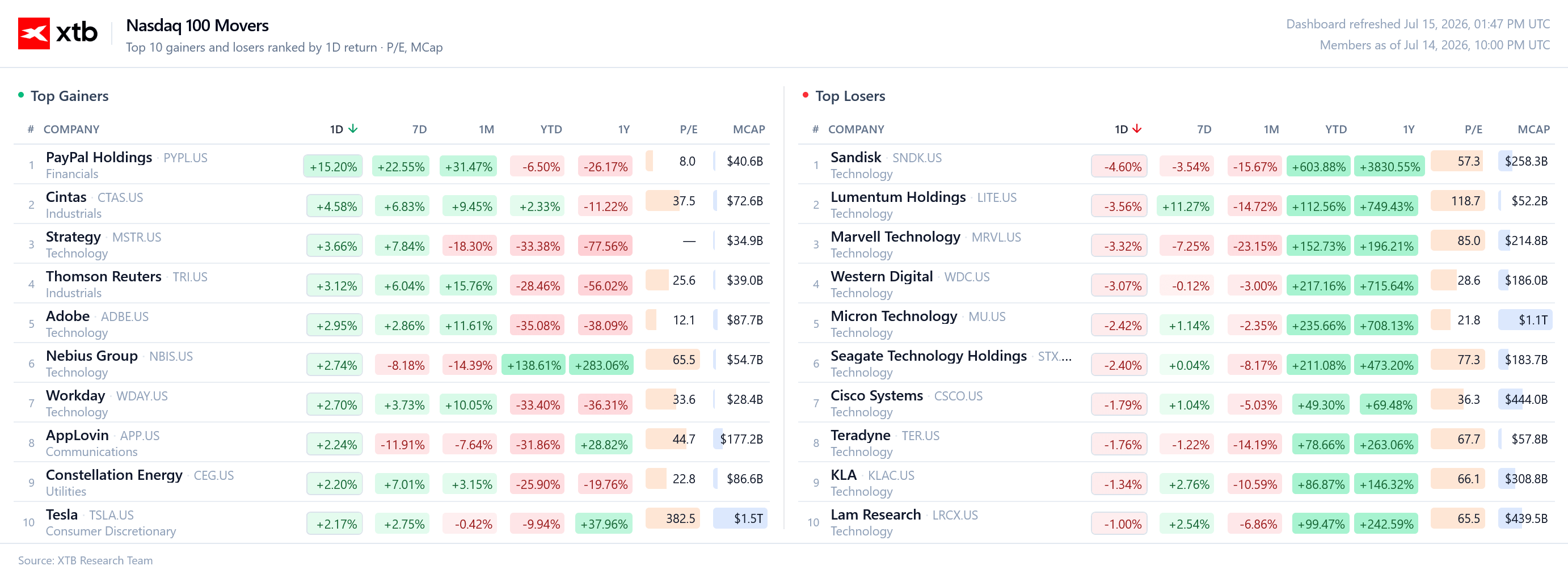

US session open – charts

At the start of the session, PayPal leads the Nasdaq 100 gainers after reports of a possible takeover bid from Stripe and private equity firm Advent. Adobe, Workday, and Strategy are also among the strongest performers, while semiconductor companies dominate the decliners, including Sandisk, Marvell, Western Digital, and Micron, suggesting some profit-taking after the sector’s powerful AI-driven rally. Despite weakness in selected memory and chip stocks, broader sentiment toward the technology sector remains positive.

Source: XTB Research

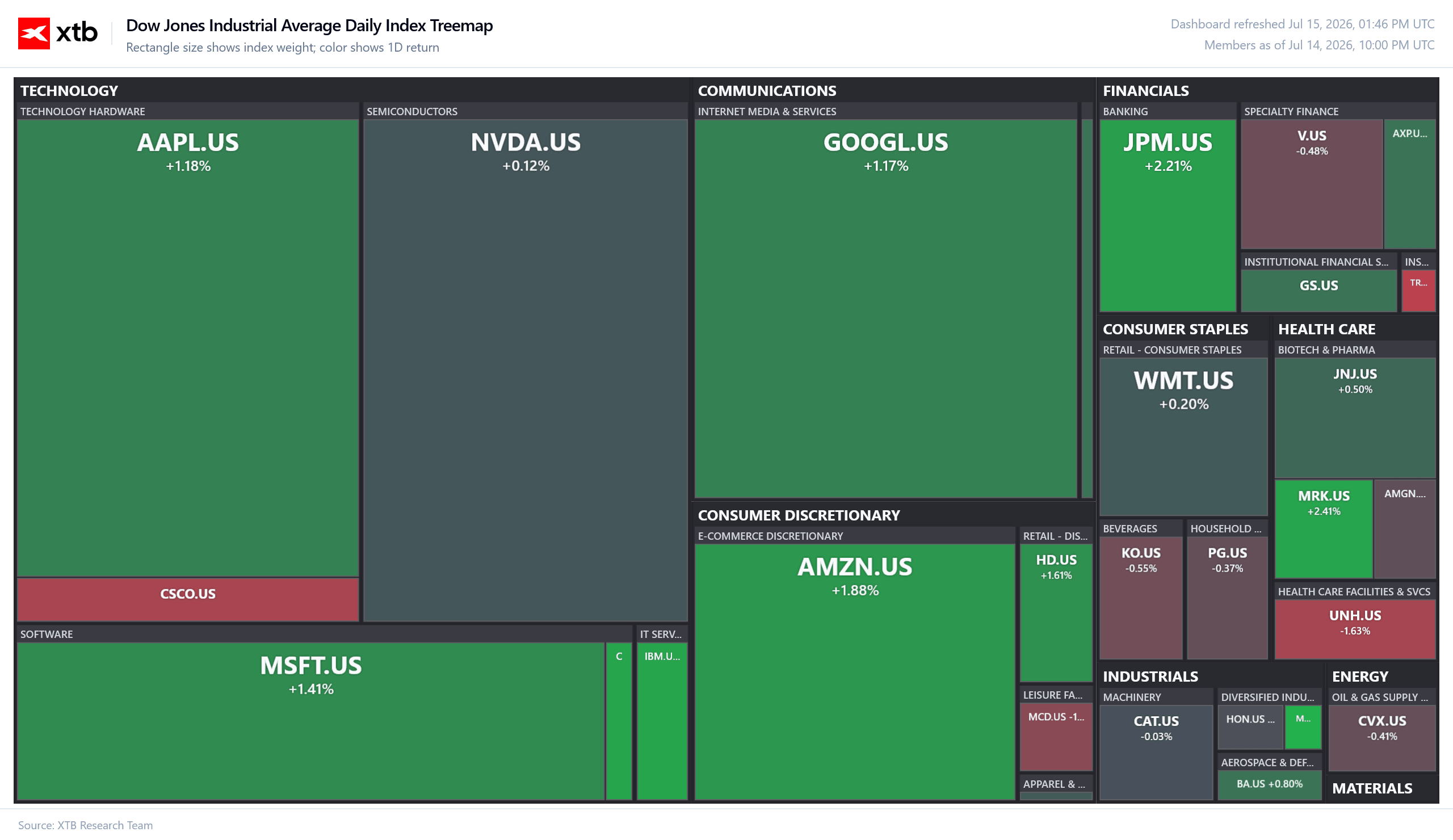

The Dow Jones Industrial Average sector map shows a clear advantage for advancing stocks, with gains led primarily by the largest technology and communications companies, including Apple, Microsoft, Alphabet, and Amazon. JPMorgan and Merck are also performing well, while UnitedHealth, Visa, Coca-Cola, and Cisco are among the stocks weighing on the index. The overall market picture remains moderately bullish, with capital concentrated mainly in the largest technology companies and sectors linked to digitalization.

Source: XTB Research

Company news

PayPal (PYPL.US): Shares of the digital payments platform rose nearly 16% after Reuters reported that Stripe and private equity firm Advent had submitted a $53 billion takeover offer. The proposed price is $60.50 per share. According to the sources, the bid was submitted earlier this month.

Johnson & Johnson (JNJ.US): Shares fell more than 1% in pre-market trading despite better-than-expected second-quarter results. J&J reported adjusted earnings per share of $2.90, compared with the $2.85 forecast. Revenue reached $25.31 billion, exceeding the consensus estimate of $25.05 billion.

Alibaba (BABA.US): Alibaba’s US-listed ADRs rose around 5% following reports that its Qwen AI model will be integrated into Apple Intelligence in China. The information was reported by Chinese state media. The market viewed the development as a potentially important boost to Alibaba’s position in China’s domestic artificial intelligence ecosystem.

Semiconductor sector: Chipmakers advanced at the start of the session, while the VanEck Semiconductor ETF (SMH) gained around 1.2%. ASML led the advance, rising 3% after raising its sales outlook for the second time this year. Intel and Lam Research also gained more than 3%, confirming a broad improvement in sentiment across the sector.

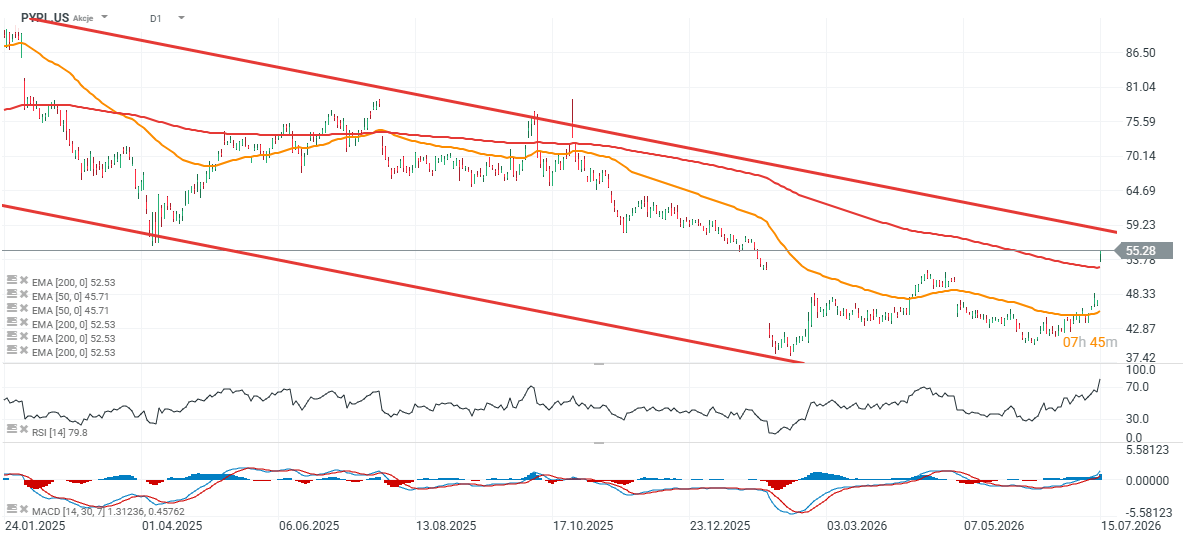

PayPal shares (D1 interval)

PayPal shares are once again trading above the 200-day EMA, marked by the red line, but a reversal of the long-term trend would require a breakout above the upper boundary of the multi-year downward channel. A move above $60 could make such a scenario more likely, while a decline below $50 per share could signal that bears are regaining control and could also imply that the takeover does not go through. The proposed transaction values the company at a premium of approximately 10% to its current share price.

Source: xStation5

Morninga Wrap: Wall Street Under Pressure. AI Loses Momentum, Netflix Disappoints, and the Persian Gulf Erupts

Daily Summary: 📉 A Red Day Across Markets. AI Sector Weighs on Wall Street, Precious Metals Under Pressure

Stock of the Week: ASML – The Machines Driving the Future of Semiconductors

Netflix down 45% from its peak 🚩 What will the streaming giant's earnings reveal?

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.