European share indices have opened the week on a mixed note — the Spanish IBEX 35 is up 0.65 per cent, the Dutch AEX is up 0.56 per cent, and the London FTSE 100 is barely in positive territory (+0.19 per cent), whilst the DAX (-0.25 per cent), the CAC40 (-0.78 per cent) and the Italian FTSE MIB (-0.32 per cent) remain under pressure. Market sentiment is being driven primarily by developments surrounding the US–Iran peace talks, following the announcement by mediators from Qatar and Pakistan of a preliminary agreement on a roadmap for a final deal within 60 days, which has significantly reduced the geopolitical risk premium.

However, the talks remain fragile — Iran has once again announced the closure of the Strait of Hormuz, a move that previously drove oil prices up to nearly $126/bbl in May, and the markets remain cautious about the sustainability of the de-escalation. Brent crude is down by around 0.7% to $80 per barrel, whilst WTI is trading around $75–77, giving back earlier gains. The dollar is strengthening — the DXY index is up 0.13%, whilst the USD/JPY pair is rising to 161.74, supported by the Fed’s hawkish stance, which is signalling a possible rate rise as early as September.

An additional factor affecting sentiment in the UK was the resignation of British Prime Minister Keir Starmer, who this morning officially announced his departure from his posts as leader of the Labour Party and head of government — meaning the UK is now facing its seventh prime minister in a decade. The market reaction was, however, muted: the pound lost just 0.19% against the dollar, trading at around USD 1.3207, whilst yields on 10-year gilts remained virtually unchanged at 4.85%, as the resignation had been widely priced in following Andy Burnham’s victory in last week’s by-election. The Polymarket prediction market puts Burnham’s chances of becoming Prime Minister at as high as 96 per cent, and nominations in the Labour leadership race are set to open on 9 July — yet the key question for nervous bond markets remains who will take the post of Chancellor of the Exchequer and how the new government will tackle Starmer’s most difficult legacy: strained public finances.

At sector level within the Euro Stoxx 50, technology is clearly in the green (+1.62%), driven by semiconductors, whilst the luxury goods and discretionary consumption sectors (-2.77%) are predominantly in the red, along with communications (-1.50%) and healthcare (-1.10%). However, the rise in volatility as measured by the VSTOXX index (-1.61% compared with the previous close) suggests that the market has calmed down somewhat following last week’s turbulence.

Company information

-

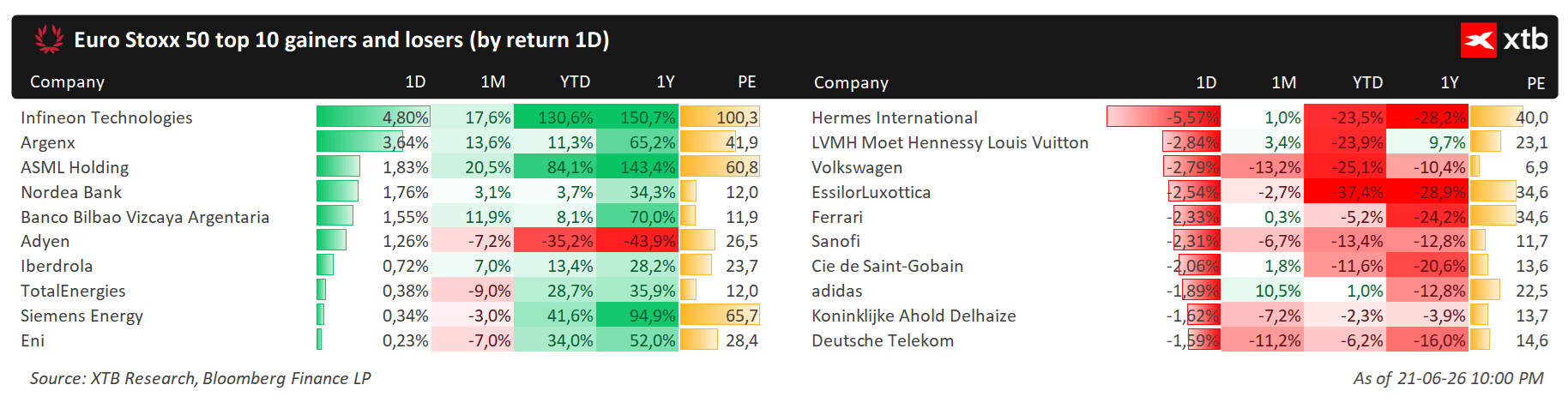

Infineon Technologies is posting the biggest gain on the Euro Stoxx 50 — its shares are up +4.80% during the session, continuing an impressive run: +130.6% year-to-date and +150.7% year-on-year, with a P/E ratio of 100x, reflecting investor enthusiasm for industrial and automotive semiconductors amid the AI boom.

-

Hermès International is down -5.57% and is the index’s biggest loser, with its shares down -23.5% since the start of the year — the weakness in the luxury goods sector stems from concerns over demand in China and a slowdown in consumer spending in the premium segment.

-

LVMH is down 2.84%, adding to the luxury sector’s slump (-23.9% YTD).

-

EasyJet is up by around 3% after the Castlelake fund made a third bid to take over the airline, reigniting speculation about consolidation in the European low-cost airline sector. Babcock International is down nearly 4% following disappointing results — the defence company missed its gross profit forecast, whilst BioArctic is up 8% after announcing a collaboration agreement with Eli Lilly in the field of neurological therapies.

Oil loses again, despite turmoil around Hormuz

Economic Calendar: Canada's CPI print takes center stage 💡

Morning Wrap: Fragile, but still. Investors are confident that U.S.-Iran talks are making progress⏰

Daily Summary: End of an Extremely Intense Week (19.06.2026)

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.