While skeptics in mainstream news cycles and Twitter analysts were racing to draw a bursting AI bubble, Satya Nadella just delivered 83 billion reasons for them to consider a career change. Microsoft didn't just beat expectations; it did so with such grace that even the dip in capital expenditures looks like a calculated show of strength rather than mere cost-cutting. The market was entering a "show-me" phase, and Microsoft responded simply: "Go ahead, take a look".

Although Microsoft shares are still roughly 20% below historical peaks—having lost about a third of their value at one point—it is clear the company maintains massive and stable foundations. If we were to ask which companies will still be with us in 5, 10, or 20 years, Microsoft would surely be on that list. Does it really deserve a slight pullback in after-hours trading then?

Main Financial Results: Math Doesn't Lie

- Revenue: $82.9 billion (+18% Y/Y), clearly above the consensus of $81.46 billion.

- EPS (Earnings Per Share): Reached $4.27 (+23%), slightly above the forecast of $4.03–$4.06.

- Net Income: $31.8 billion—Microsoft generates as much "pure" profit as the total valuation of some S&P 500 companies.

- Operating Income: $38.4 billion (+20%), which, with an operating margin exceeding 46%, makes the Redmond giant the most efficient money-making machine in Silicon Valley.

- Shareholder Returns: $10.2 billion paid out in dividends and share buybacks.

Segments: Azure Pulls Away, the Rest Scrambles to Keep Up

- Azure & Other Cloud: A 40% increase (39% ex-FX) is a knockout for those who feared "cloud fatigue". These results exceeded market expectations, though it is worth noting that Amazon also improved with its AWS cloud.

- AI Business Run Rate: The annual revenue run rate for AI surpassed $37 billion (+123% Y/Y). This isn't just "potential" anymore; it is a gargantuan, real business. Furthermore, this figure lands above CAPEX levels, showing the company is no longer burning cash without knowing if it will ever see a return.

- Microsoft 365 Consumer Cloud: A 33% increase shows that the average user wants and pays for Copilot, regardless of what the media claims.

- Dynamics 365: Grew by 22%, slowly eating away at the competition in the ERP/CRM market.

- Commercial RPO: Remaining performance obligations surged 99% to $627 billion. Microsoft holds a portfolio of orders exceeding the GDP of most European nations. Thanks to recent closer cooperation with Anthropic, it will likely be possible to convert this amount into real revenue even sooner.

- Weak Spots (For those nitpicking): Windows OEM and Devices fell by 2%, and Xbox by 5%. While the market previously obsessed over these numbers, it seems CEO Satya Nadella has no time for toys while building the infrastructure of the future.

Capex: The Great Escape from the "Nvidia Tax"

The biggest surprise for the pessimists? Capital expenditures amounted to $31.9 billion, while the market fearfully expected over $35.29 billion. This is a strategic victory for Amy Hood, the company’s CFO. Microsoft proved it can deliver record Azure growth with less capital outlay than predicted. This suggests that either their own Maia chips have started to significantly lower costs, or infrastructure efficiency has reached a whole new level. The "Peak Capex" era might already be in the rearview mirror, which means only one thing: a potential explosion in Free Cash Flow.

Summary: Who Is the King?

For months, mainstream media fed us a narrative of "threats" from OpenAI, "disputes" over stakes, and a "costly" arms race that was supposedly going to bleed Microsoft dry. Today's results are a brutal reality check for those theories.

Microsoft ceased to be just an "OpenAI sidecar" the moment it showed $37 billion in real AI revenue. Diversifying its portfolio with Anthropic and its own models means the Redmond giant is no longer a hostage to a single lab. Take note of the RPO—a 99% jump to $627 billion is a signal that corporate clients are not just "testing" AI; they are practically signing massive, multi-year contracts.

A valuation around 25x P/E with 23% profit growth looks like a supermarket discount right now. If someone was looking for a "bubble," they need to look elsewhere, because Microsoft Cloud shows strong foundations for the next bull wave, provided the broader market allows it. The company hasn't just returned to the throne; it has started climbing further up the stairs of technological evolution. Microsoft didn't end up in the Mag7 group by accident. Yes, it had its problems, but most are likely behind it. It’s worth noting that Michael Burry recently indicated he is buying the discounted Microsoft. Of course, that doesn't have to be a benchmark for everyone, considering his long-held put options on Nvidia.

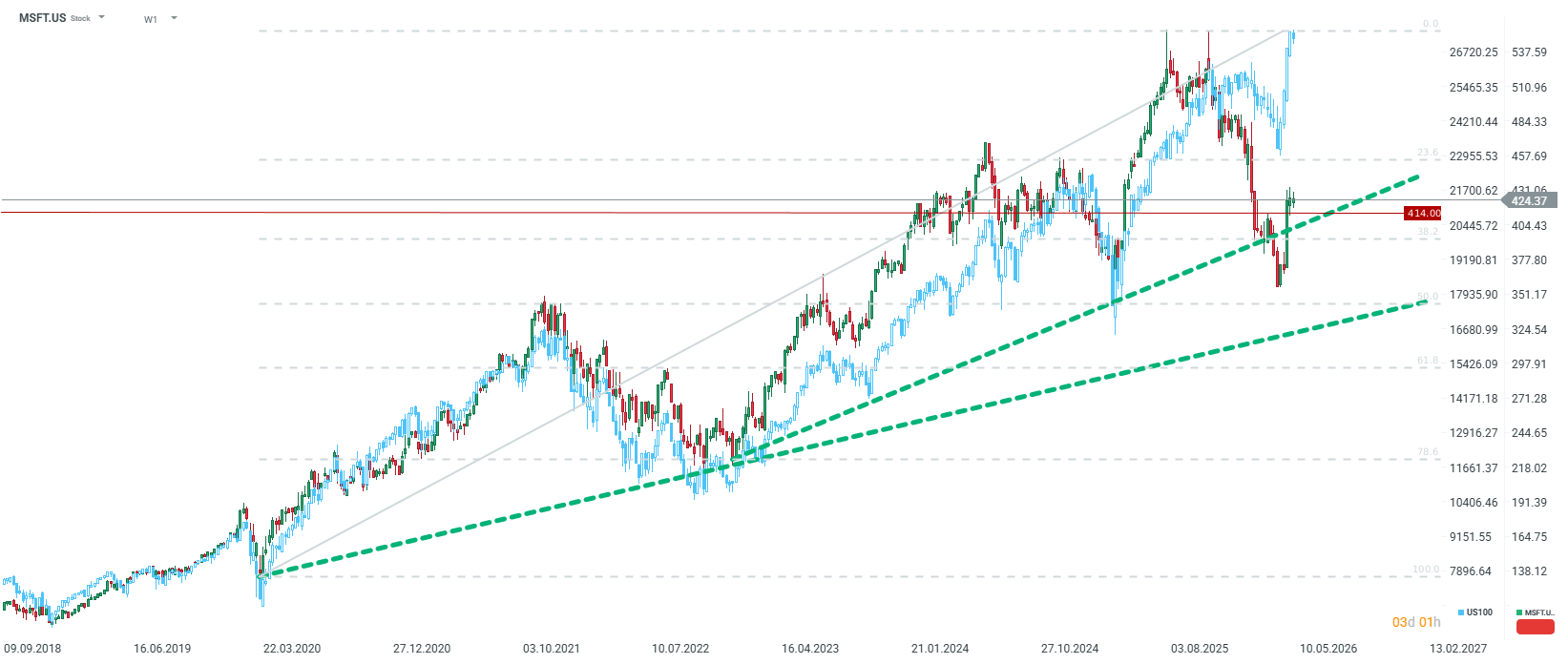

Microsoft is trading about 1.5% below its close in after-hours trading. Key support at $400 appears secure. Source: xStation5

Microsoft is trading about 1.5% below its close in after-hours trading. Key support at $400 appears secure. Source: xStation5

OpenAI heads into a price war ahead of an IPO?

US OPEN: A recovery after declines, Trump threatens to resume fighting with Iran

Daily Summary- Return of the Sell-off on Wall Street⬇️

🔴US100 drops nearly 4%

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.