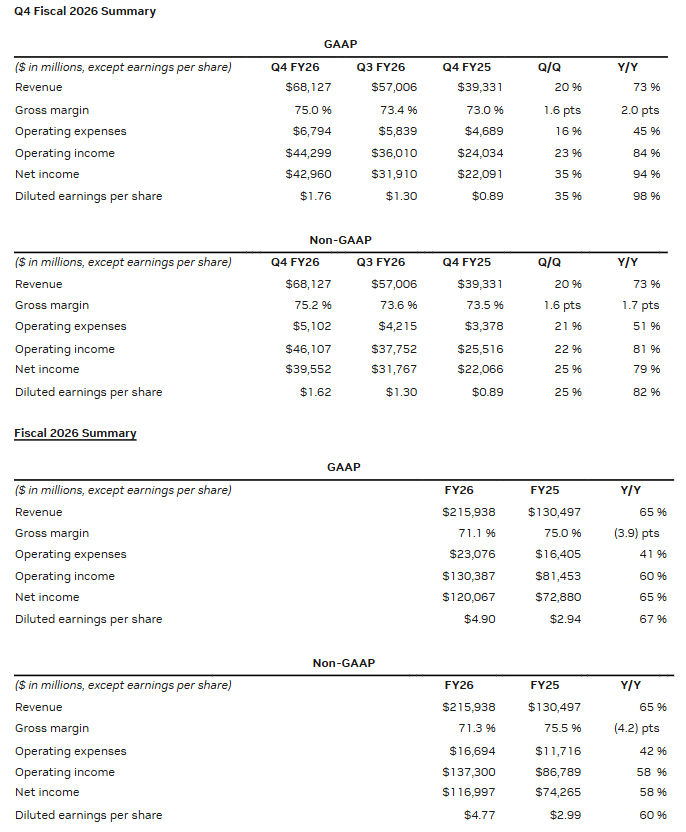

Nvidia (NVDA.US) has once again proven that it remains the biggest beneficiary of the global artificial intelligence boom. The latest quarterly report for fiscal Q4 2026 (calendar Q4 2025) delivered record revenue of $68.1 billion, and the company not only maintained an impressive growth momentum but also beat market expectations on both revenue and earnings. Business fundamentals continue to run ahead of analysts’ already-elevated forecasts. Over the full fiscal year, Nvidia’s revenue increased 65% year over year.

The Data Center segment remains the standout. Since the emergence of ChatGPT, sales in this business have increased 13-fold, underscoring Nvidia’s position as the core of the AI infrastructure stack. Demand for its chips still exceeds supply, which is clearly reflected in profitability. A gross margin of around 75% confirms the company’s exceptional pricing power and technological leadership. Cash generation is equally striking: free cash flow (FCF) reached $34.9 billion, up nearly $20 billion year over year. This level of cash production gives Nvidia enormous flexibility—both to invest in next-generation platforms and to potentially return more capital to shareholders.

Management also delivered a very strong outlook: fiscal Q1 2026 revenue is guided up to around $79.6 billion, implying that the growth trajectory can remain steep even as the comparison base rises. In the immediate reaction to the release, shares climbed as much as 4% in after-hours trading, but ultimately finished the post-close session only slightly higher. A fuller market verdict will likely come at tomorrow’s open, when institutional flows set the tone. CEO Jensen Huang emphasized that customers are “racing” to invest in AI compute and that computing demand is growing exponentially.

Company financials (key figures)

-

4Q revenue: $68.1B (consensus: $65.91B)

-

+20% QoQ, +73% YoY

-

-

4Q Data Center revenue: $62.3B (consensus: $60.36B)

-

+22% QoQ, +75% YoY

-

-

Gaming & AI PC (4Q): $3.7B, +47% YoY (strong Blackwell demand)

-

-13% QoQ as channel inventory naturally moderated after a strong holiday season

-

FY total: +41% YoY to a record $16.0B

-

-

Professional Visualization (4Q): $1.3B, +74% QoQ, +159% YoY (exceptional Blackwell demand)

-

FY total: +70% YoY to a record $3.2B

-

-

Automotive & Robotics (4Q): $604M, +2% QoQ, +6% YoY (continued adoption of NVIDIA’s self-driving platforms)

-

FY total: +39% to a record $2.3B

-

-

Gross margin (4Q FY2026): GAAP 75.0%, non-GAAP 75.2%

-

Gross margin (FY2026): GAAP 71.1%, non-GAAP 71.3%

-

EPS (4Q): GAAP $1.76, non-GAAP $1.62 (vs $1.52 expected)

-

FY2026 EPS: GAAP $4.90, non-GAAP $4.77

-

Q1 revenue guidance: $76.44B–$79.56B (consensus: $72.78B)

-

Guidance note: management/CEO stated the outlook assumes no Data Center compute revenue from China

-

Networking revenue: $11B, >3.5x YoY

-

Capital returns (FY): $41.1B (buybacks + cash dividends)

-

Remaining buyback authorization: $58.5B at the end of 4Q

-

Next dividend: $0.01 per share, payable April 1, 2026 (record date March 11, 2026)

Source: Nvidia Investor Relations

Additional topics: CAPEX, margins, geopolitics, product cycle

-

CAPEX: $6.1B in FY26; Nvidia signals a larger investment push ahead and higher FY27 CAPEX, driven by AI demand.

-

Inventory write-off / margins: a $4.5B inventory charge tied to H20 (overstock and purchase commitments) pressured FY26 gross margins.

-

4Q gross margin benefited from lower inventory provisions.

-

-

Trade/tariff risk: Nvidia warned H200 shipments may face a 25% U.S. import tariff as the supply chain expands beyond Asia.

-

China / export licensing: the U.S. granted a Feb 2026 license to ship limited H200 volumes to specific China-based customers, but Nvidia says there is no revenue yet and it remains unclear whether imports into China will be allowed.

-

OpenAI: Nvidia is in talks to finalize an investment and partnership with OpenAI, with no assurance a deal will be signed.

-

Supply constraints: Nvidia expects gaming supply constraints in Q1 and beyond.

-

Demand mix: hyperscalers accounted for just over 50% of 4Q Data Center revenue.

Technology / roadmap highlights

-

Nvidia highlighted inference leadership and power-efficiency gains from Blackwell and NVL72/GB300, claiming up to 50x performance per watt and materially lower cost per token.

-

Nvidia unveiled the Rubin platform: Vera CPU, Rubin GPU, NVLink-6, Spectrum-6, BlueField-4.

-

The company shipped the first Vera Rubin samples, targeting production shipments in the second half of the year, which management expects will be widely adopted by cloud model builders.

-

Geopolitical/China risk remains unresolved; Nvidia also warned that Chinese competitors could disrupt the global AI industry over the long term.

-

Product positioning: Jensen Huang said “Grace Blackwell with NVLink is the king of inference.”

Detailed outlook (FY2027 methodology + Q1)

-

Starting in fiscal Q1 2027, Nvidia will include stock-based compensation (SBC) expense in non-GAAP measures.

-

Q1 FY2027 revenue outlook: $78.0B ±2%, with no assumed China Data Center compute revenue.

-

Gross margin outlook: GAAP 74.9% ±50 bps, non-GAAP 75.0% ±50 bps, including a ~0.1% impact from SBC.

-

Operating expenses (OPEX): GAAP ~$7.7B, non-GAAP ~$7.5B, including $1.9B of SBC expense.

-

FY2027 tax rate: GAAP & non-GAAP 17.0%–19.0%, excluding discrete items and material changes to Nvidia’s tax environment.

NVDA.US share price (technical note)

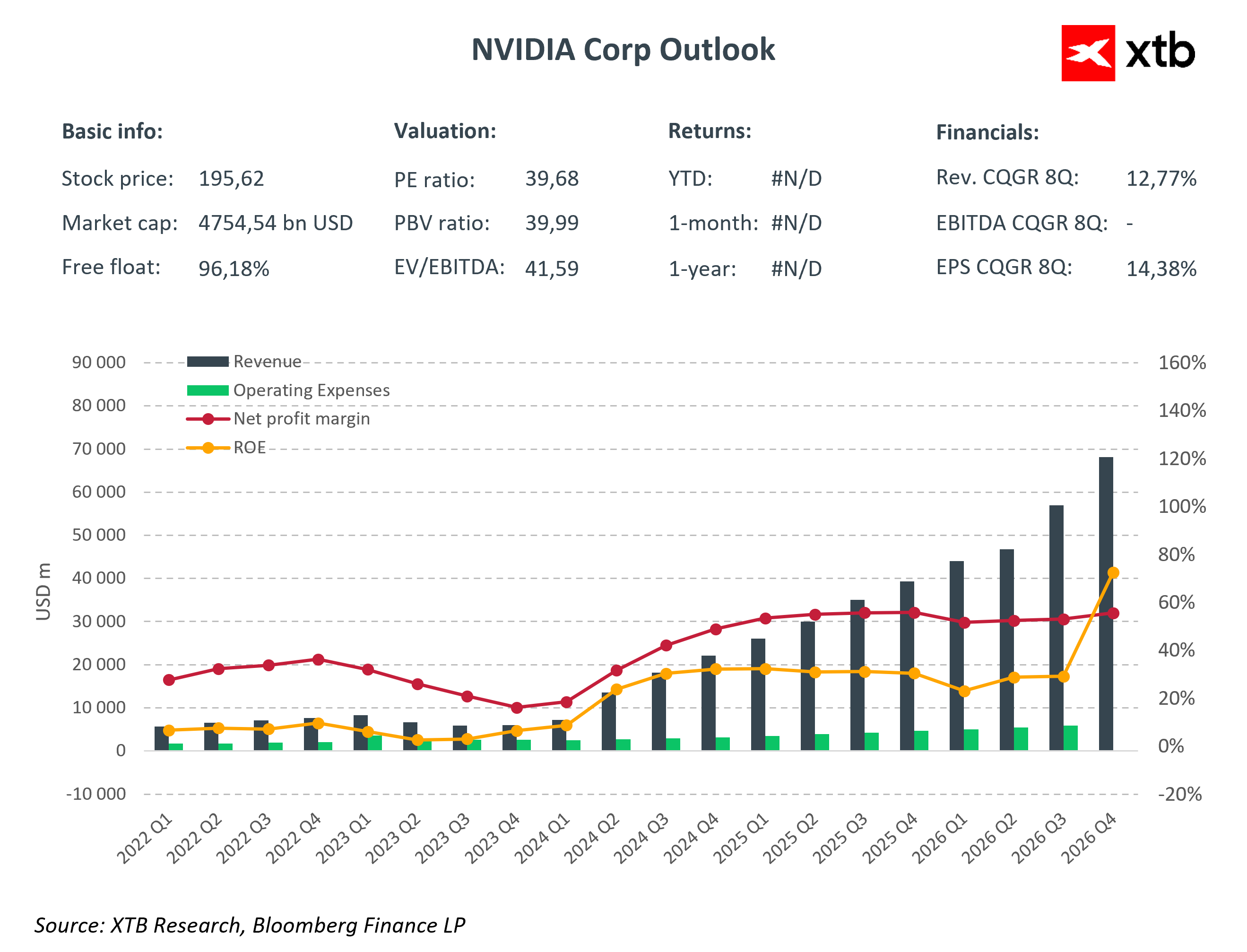

NVDA recently tested the 200-session EMA (EMA200), which acted as a key support level. Since then, the stock has risen by roughly 10%, and tomorrow’s session could open above $200 per share, with a potential attempt toward new highs near $210.

Source: xStation5

Aktualnie wskaźnik cena/zysk oscyluje wokół 40, ale wskaźnik ceny do oczekiwanego 12-miesięcznego zysku wynosi niespełna 30, co dla spółki 'jakości' Nvidia nie wydaje się bardzo wymagającą wyceną na poziomie mnożników. Jeśli ekstrapolujemy dynamikę z poprzednich kwartałów i uznamy, że tempo ekspansji zysków NVDA w tym roku przekroczy prognozy analityków, możemy założyć, że spółka wyceniania jest mniej więcej na poziomie 25-krotności rocznych, oczekiwanych zysków co jest mniej więcej zgodne ze średnią wyceną Nasdaq 100, gdzie aktualnie to 24.

Source: XTB Research, Bloomberg Finance LP

Wall Street rebound continues ahead of the US open 📈Netflix surges on Goldman Sachs upgrade

DAX down 12% from all-time high 🚩Watch this 2 stocks in April

Daily summary: Hopes for peace and space stocks in the spotlight

Globalstar: Are we headed for a battle of giants over orbit?

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.