The biggest disappointment: subscription growth

The key issue in the report was subscription revenue, the core of ServiceNow’s business model. It reached $3.67 billion, representing a slight beat and 22% year-over-year growth. However, investors were expecting something materially stronger. Management explained that approximately 75 basis points of growth were lost due to delays in closing several large on-premise deals in the Middle East, linked to ongoing regional conflict.

Fundamentally, this looks like a timing issue rather than a sign of weakening demand. However, in the current market environment, investors are reacting more to momentum than to nuance.

Raised guidance failed to reassure the market

Under normal circumstances, raising full-year guidance would support the stock. ServiceNow increased its full-year subscription revenue outlook to $15.74–$15.78 billion, up from $15.53–$15.57 billion previously. CFO Gina Mastantuono emphasized that the updated guidance already includes conservative assumptions around delayed deal timing in the Middle East.

This is an important signal, suggesting management does not see structural weakness in demand. However, investors interpreted the move more as an attempt to stabilize sentiment than as a strong catalyst for a turnaround.

AI narrative still ahead of monetization

From a sector perspective, the key question around ServiceNow is no longer whether it is growing, but whether it is growing fast enough to justify its positioning as a major AI beneficiary. The company has been framing itself as an “AI control tower” for enterprise clients. The issue is that the market now demands not just a compelling narrative, but tangible financial impact.

Management indicated that its AI product line is on track to exceed $1 billion in revenue in 2026, with CEO Bill McDermott suggesting that $1.5 billion could be a more realistic figure. While promising, forward-looking potential is no longer sufficient if quarterly results do not demonstrate a clear inflection point.

Fundamentals remain strong

This is where the disconnect between market reaction and operational reality becomes most visible. ServiceNow does not appear to be a business facing structural deterioration. On the contrary, the company continues to deliver strong growth, raise guidance, execute aggressive share buybacks, and close strategic acquisitions.

The company repurchased roughly 20 million shares during the quarter—more than double the total for all of 2025. It also completed the $7.75 billion acquisition of cybersecurity firm Armis ahead of schedule. These are not signs of a company under pressure, but rather of one with strong financial capacity and confidence in its long-term trajectory.

Why the reaction was so severe

The explanation lies in how ServiceNow is being valued. The company is no longer treated as a typical growth stock, but as one of the flagship AI stories in enterprise software. That raises the bar significantly. With the stock already down sharply year-to-date, the market was not looking for a “good enough” quarter, but for results that would clearly shift the narrative.

Instead, investors got a marginal beat, explanations around delayed deals, and guidance to wait for a broader strategic update at the upcoming Analyst Day. That proved insufficient, triggering a sharp sell-off that spilled over into other software names such as Salesforce, Oracle, and Adobe.

A crisis of patience, not a crisis of business

This reaction can be seen primarily as a reset of expectations rather than a signal of deteriorating fundamentals. The market is punishing ServiceNow not for weak results, but for failing to deliver a sufficiently strong proof of AI-driven acceleration—something investors have increasingly come to expect from infrastructure and enterprise software leaders.

This distinction matters. In the short term, sentiment may remain fragile. In the longer term, the key question will be whether delayed deals return to the pipeline and whether AI meaningfully accelerates growth.

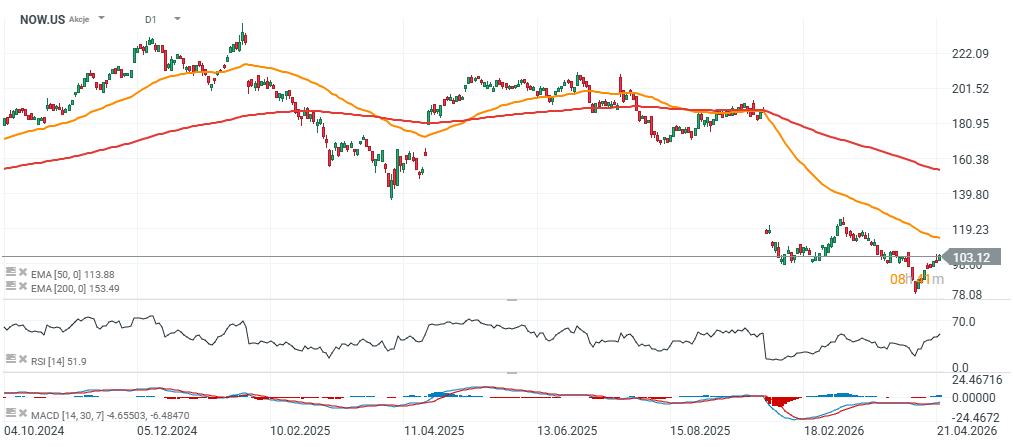

At present, this looks more like a company that disappointed on pace rather than one losing control of its business. The valuation, based on forward 12-month earnings, currently stands at around 23x and may decline toward 21x after the market open, suggesting a meaningful cooling in investor expectations.

Source: xStation5

US Closed: Postponed negotiations weigh on futures

Will Massive AI Investments Bring Dark Clouds Over Wall Street?

Market wrap: Limited volatility and a strong dollar

Daily Summary: Dollar at 1-year high, stocks rebound on renewed risk appetite 🚀 (18.06.2026)

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.