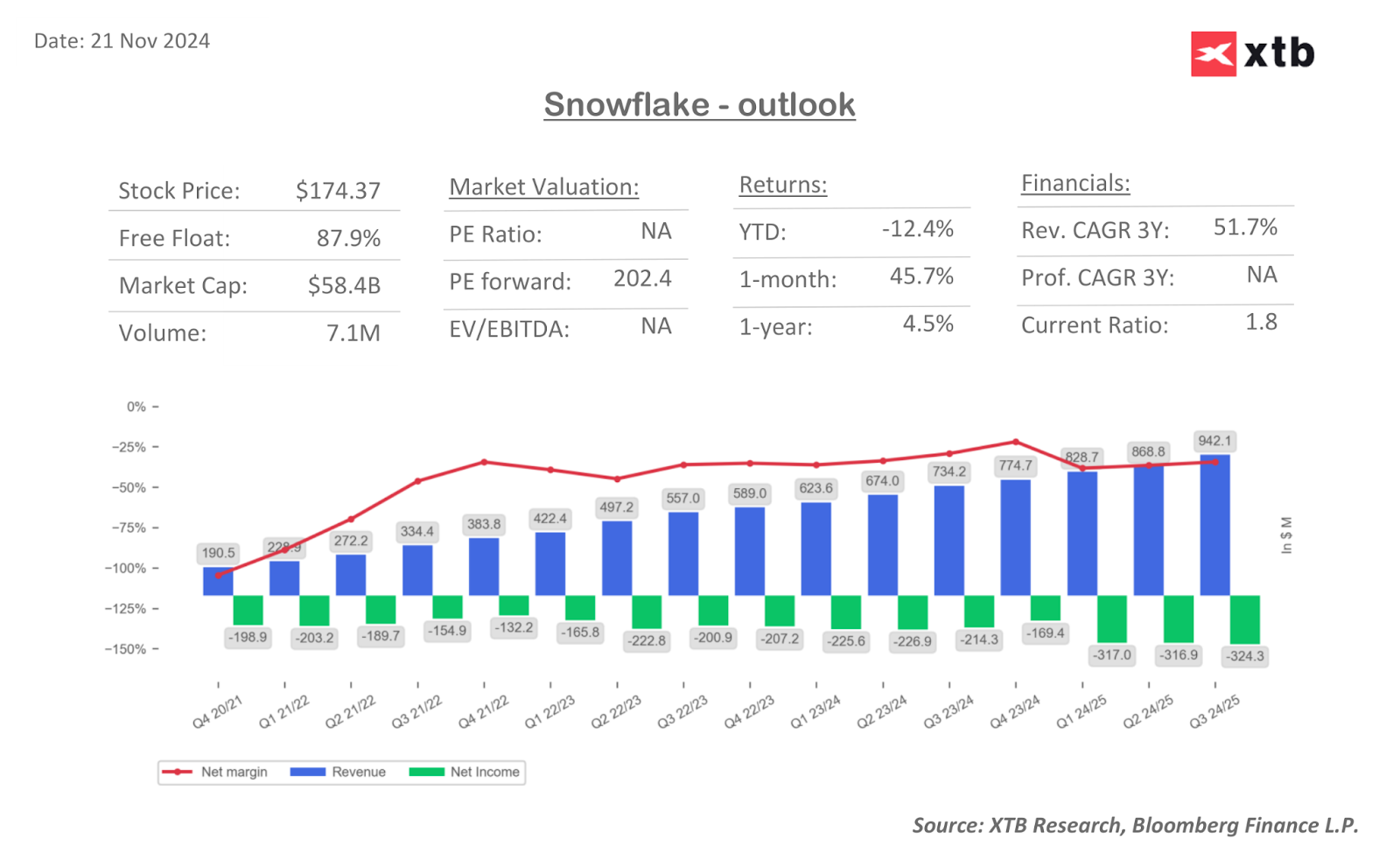

Snowflake (SNOW.US) reported record revenues, continuously posting year-over-year and quarter-over-quarter sales growth since Q4 2020. Furthermore, the company raised its forecasts for Q4, significantly surpassing market consensus. As a result, the stock soared today, gaining over 33%.

The company achieved sales of $942.1 million, representing a year-over-year increase of 28%. The growth rate of sales is slightly decelerating due to the high base effect, but it remains at a high level. In the case of product sales (the company's main business segment), Snowflake recorded an increase to $900.3 million (+29% y/y), surpassing the $900 million mark for the first time in history and significantly exceeding the forecasted $856.6 million.

Additionally, the company anticipates maintaining positive sales trends in the fourth quarter, raising its estimates for product sales revenue to a range of $906-911 million, compared to analysts' estimated level of $882 million. This means that for the entire fiscal year, it expects product revenues of $3.43 billion, which translates to an increase of $0.07 billion over the estimates.

The company is heavily investing in the development of AI projects, and it is evident that investor hopes for maintaining positive trends remain very high. The extent to which investors believe in the company's cost-cutting policy, while simultaneously expanding its product and service base, is indicated by the forward P/E ratio, which currently shows that the company is trading at 202 times the estimated earnings for the next year. Such seemingly drastically high valuations primarily result from the company's growth-oriented nature and the fact that it is just entering the path to positive net profit margins. Therefore, if it succeeds, current shareholders have the chance to get ahead of the trend. The forward P/S ratio presents a much more stable picture, standing at 14.1x for the company.

3Q24 FINANCIAL RESULTS:

- Revenue $942.1 million, +28% y/y, estimate $898.6 million

- Product revenue $900.3 million, +29% y/y, estimate $856.6 million

- Professional services and other revenue $41.8 million, +17% y/y, estimate $40.8 million

- Loss per share 98c vs. loss/shr 65c y/y

- Net revenue retention rate 127% vs. 135% y/y, estimate 124.2%

- Current remaining performance obligation $5.7 billion, +54% y/y, estimate $5.22 billion

- Adjusted gross margin 73% vs. 75% y/y, estimate 71.8%

- Adjusted diluted EPS 20c vs. 25c y/y, estimate 15c

4Q24 FORECAST

- Product revenue $906 million to $911 million, estimate $890.7 million

- Adj. operating margin 4%

2025 FORECAST:

- Product revenue: $3.43 billion, previously: $3.36 billion, estimate $3.36 billion

- Adj. operating margin 4% (previously expected: 3%)

Snowflake chart (1D)

The company's stock has broken through the local highs from May of this year and reached its highest level since February during today's session. The sharp upward movement may indicate a potential correction tomorrow, but in the slightly longer term, technical indicators show potential for further growth. The consolidation that the stock had been in since September of this year has been broken, and investors should pay attention to the $191 level, which is currently a key resistance.

Source: xStation

Has Alphabet just won the AI race?

MicroStrategy in trouble? Shares down 67% from the highs ✂

Stock of the Week – NVIDIA (21.11.2025)

DE40: European tech and defence stocks sell-off

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.