When investors talk about artificial intelligence today, the same names almost always pop up. NVIDIA, Microsoft, Amazon, Meta, and Alphabet have become symbols of a technological revolution that has reshaped the global economic landscape in just a few years. Every new sales record for AI chips, every new generation of language models, and every announcement about building giant data centers instantly makes front-page news on financial portals.

The problem is that most of the market looks exclusively at the end result.

They see NVIDIA's processors, OpenAI's new models, and the next data centers being built by the world's largest tech giants. Much less often do they stop to consider what must happen first—before any AI chip ever makes its way into a server.

Meanwhile, a modern semiconductor is one of the most complex products humanity has ever created. Producing a single chip requires hundreds of technological stages and months of work. On a silicon wafer, consecutive layers of materials are deposited, removed, and modified with precision measured in nanometers. Any deviation from the norm can mean losing an entire wafer worth hundreds of thousands of dollars.

This is exactly where Lam Research comes in.

The company does not design processors, nor does it manufacture memory. It does not build artificial intelligence models or sell cloud services. Instead, it provides the technologies used during the most demanding stages of semiconductor manufacturing. You could say that Lam does not sell the gold itself, but rather the tools needed to mine it.

This is one of the reasons why the company remains virtually unknown to the broader investing public. It is hard to get excited about machinery used in semiconductor fabs when the market's full attention is gripped by NVIDIA's latest records. Paradoxically, this very invisibility makes Lam one of the most interesting companies in the entire AI ecosystem.

Because while most investors have never interacted with Lam's products, nearly every advanced chip in the world has.

The company's clients include the largest semiconductor manufacturers in the world. They are responsible for producing the processors used in data centers, the HBM memory driving the development of artificial intelligence, and the most advanced logic circuits. Although they compete on many fronts, they share one common trait. Their fabs are filled with equipment supplied by a small group of specialized semiconductor equipment manufacturers. Lam belongs to this elite circle.

For many years, investors viewed the company as a classic cyclical business. When chipmakers boosted capital expenditures, Lam’s revenues surged. When the industry cut back spending, the company's performance quickly deteriorated. This operating model was well-known to all market participants.

Today, however, something much more interesting is happening.

Most investors assume that the AI revolution simply means a higher volume of chips being manufactured. This is true, but only partially. What is far more important is that each consecutive chip is becoming increasingly difficult to produce.

For decades, semiconductor advancement relied primarily on miniaturization. Every new generation of transistors was smaller, faster, and more energy-efficient than the last. Over time, however, physics began putting up greater resistance. Shrinking structures further became incredibly expensive and technologically complex.

The industry responded to this problem by increasing the complexity of the chips themselves.

Modern AI accelerators increasingly resemble multi-story structures. HBM memories are stacked on top of one another. Individual systems consist of multiple specialized chips integrated into a single whole. NAND memories contain hundreds of layers of materials, and new transistor architectures require an ever-greater number of technological operations.

And this is where the most important element of the Lam Research story lies.

For the company, the key is not that the world needs more semiconductors. The key is that every semiconductor requires a growing number of operations necessary to manufacture it.

This is a subtle but fundamental difference.

The more complex a chip becomes, the more work must be done by the tools responsible for creating consecutive layers and structures. In practice, this means that the importance of the technologies offered by Lam is growing faster than the number of actual chips leaving the fabs.

This is precisely why the company's management increasingly talks not just about the growth of the AI market, but also about the rising complexity of modern architectures. For Lam, artificial intelligence is not merely another source of demand. It is a force that increases the significance of the technologies offered by the company throughout the entire semiconductor manufacturing process.

As a result, Lam is becoming something more than a mere beneficiary of the AI boom. The company sits at the very heart of the infrastructural backbone of this revolution. It does not compete with NVIDIA or OpenAI. It makes money because the world needs increasingly advanced chips, and those chips are becoming increasingly difficult to produce.

And that is precisely why Lam Research might be one of the most interesting yet underappreciated companies in the entire artificial intelligence ecosystem. While the market focuses on who is selling the most chips, Lam profits from the very process of their creation. And the history of technology has shown time and again that the providers of essential infrastructure often become some of the greatest beneficiaries of long-term shifts.

Chapter 1. The more advanced the chip, the more work for Lam

To understand why Lam Research finds itself in such an interesting position today, one must start with one key shift: the AI revolution is not only driving up demand for semiconductors, but it is also fundamentally changing how they are designed and manufactured.

For many years, the industry's growth was relatively straightforward. New generations of chips contained more transistors, and progress stemmed mainly from their miniaturization. Today, this model is no longer enough.

The soaring demand for computing power forces a new approach. Manufacturers are transitioning toward more complex architectures, novel materials, and integrating multiple chips into a single system.

It is this structural pivot that increases the significance of Lam Research.

A good example is NAND memory, which has evolved from simple designs into structures boasting over 300 layers. Every additional layer translates to consecutive, increasingly demanding production steps, from material deposition to precise etching and cleaning.

A similar trend is visible in HBM memories, which are critical for AI infrastructure. Building them involves vertically stacking multiple layers and connecting them in an extremely precise manner, which enables achieving the bandwidth required by modern artificial intelligence models. Simultaneously, this significantly increases manufacturing difficulty.

This is even more pronounced in the most advanced logic processors, where new transistor architectures improve performance and power efficiency but significantly complicate the fabrication process.

In this context, the concept of process intensity becomes pivotal. It refers to the number and complexity of operations required to manufacture a single chip. For Lam Research, how complicated the fabrication process itself becomes is often more important than the volume of wafers.

The more technological steps a new generation of chips requires, the greater the demand for advanced manufacturing tools. Consequently, Lam’s market can grow faster than the semiconductor sector as a whole.

This is why the company emphasizes not just the scale of its customers' investments, but also the mounting complexity of modern fabs. For Lam, it is not solely about the number of new facilities, but primarily about what will be produced inside them.

And everything indicates that the future belongs to increasingly complex chips.

In the context of AI, this carries special significance. The development of large language models and advanced computing systems requires not just more chips, but primarily chips of substantially higher complexity.

For Lam Research, this is an exceptionally favorable combination. The company benefits both from the growing volume of investments in the semiconductor sector and from the rising complexity of the chips themselves. And the more advanced a chip becomes, the more work falls to Lam Research.

Chapter 2. Why AI is so critical for Lam

Though Lam Research has been supplying equipment to semiconductor manufacturers for decades, the rise of artificial intelligence has emerged as the most critical factor shaping the company's prospects today. The reason is relatively simple. AI requires not just more chips, but primarily more advanced chips.

Each new generation of accelerators deployed in data centers demands more processing power, faster communication, and higher memory bandwidth. To meet these specifications, semiconductor manufacturers are developing new chip architectures, increasing memory layer counts, and deploying ever-more intricate manufacturing processes. This, in turn, translates into greater demand for the technologies utilized by Lam.

This is particularly visible in the HBM memory segment, which has become an indispensable component of modern AI accelerators. The growing number of layers, more advanced connections, and escalating manufacturing quality requirements increase the importance of wafer etching, deposition, and cleaning processes—areas where Lam commands a strong market position.

Crucially, the benefits are not confined to memory alone. The rising complexity of logic chips, the deployment of new transistor architectures, and the expanding scale of data center investments mean that artificial intelligence is now influencing virtually every market segment served by the company.

This is precisely why Lam's management consistently points to AI as the most critical growth driver for the coming years. For the company, this is not just another investment cycle in the semiconductor industry. It is a trend that increases both the scale of customer spending and the prominence of the technologies supplied by Lam in the process of manufacturing the most advanced chips in the world.

Chapter 3. AI is just the beginning. Other megatrends supporting Lam Research

While artificial intelligence is currently the most important topic in the semiconductor industry, it would be a mistake to reduce Lam Research’s entire story solely to AI. The company benefits from several long-term trends that reinforce one another and together create an exceptionally favorable environment for semiconductor equipment suppliers.

The first remains the development of the memory market. While HBM used in AI accelerators has grabbed the most attention recently, investments in NAND and DRAM memory are equally vital. The situation in the NAND market looks particularly interesting, as manufacturers transition to increasingly advanced technological generations. In practice, this means retooling existing production lines and the necessity of implementing new processes, which generates incremental demand for Lam’s devices.

Another important area is advanced packaging, referred to in the industry as advanced packaging. Just a few years ago, semiconductor performance was boosted primarily through transistor miniaturization. Today, the way individual chips are connected into a single system plays an increasingly vital role. It is through such solutions that modern AI accelerators—where the processor, memory, and communication components work together as a single organism—are made possible. Lam’s management notes that revenues tied to advanced packaging are currently among the fastest-growing areas of the company's operations, showing how vital this segment is becoming for the entire industry.

The service business concentrated in the Customer Support Business Group segment is also becoming increasingly significant. Unlike new equipment sales, which remain tightly tied to the industry's investment cycle, servicing services generate more recurring revenues. Semiconductor manufacturers cannot afford factory downtime, so they regularly invest in spare parts, upgrades, and enhancing the efficiency of existing tools. In recent quarters, this segment has achieved record results and is becoming an increasingly important pillar of Lam’s business.

It is also worth paying attention to the changes occurring in the global semiconductor supply chain. The United States, Europe, Japan, and South Korea are allocating tens of billions of dollars to build out their own manufacturing capacities. A decade ago, most new investments were concentrated in a handful of Asian countries. Today, we are witnessing a gradual regionalization of manufacturing, which requires building new fabs and outfitting them with cutting-edge equipment. Regardless of where a manufacturing facility is built, the technological process remains similar, meaning more opportunities for suppliers like Lam.

One also cannot overlook the progressive digitalization of the semiconductor fabs themselves. Modern devices generate massive amounts of data used to optimize production processes, improve quality, and boost efficiency. Software, data analytics, and solutions leveraging AI components to monitor technological processes are playing an increasingly prominent role. This is an area that does not capture as much attention as new physical hardware, but it could become an additional source of competitive advantage and revenue in the coming years.

Consequently, Lam Research sits at the crossroads of multiple long-term trends. AI remains the most important of them, but it is by no means the only one. The evolution of memory, advanced packaging, the growth of the service business, the regionalization of semiconductor manufacturing, and fab digitalization together form a broad foundation for growth, ensuring the company's story does not depend on a single market or technology. It is this diversity of factors that makes Lam much more than just a bet on the continued expansion of artificial intelligence today.

Chapter 4. The numbers confirm the growth story

The greatest strength of Lam Research is that its artificial intelligence story does not live solely in investor presentations and management commentary. It is not a narrative that is difficult to find in financial statements; in Lam's case, the AI effect is visible directly on the income statement and balance sheet.

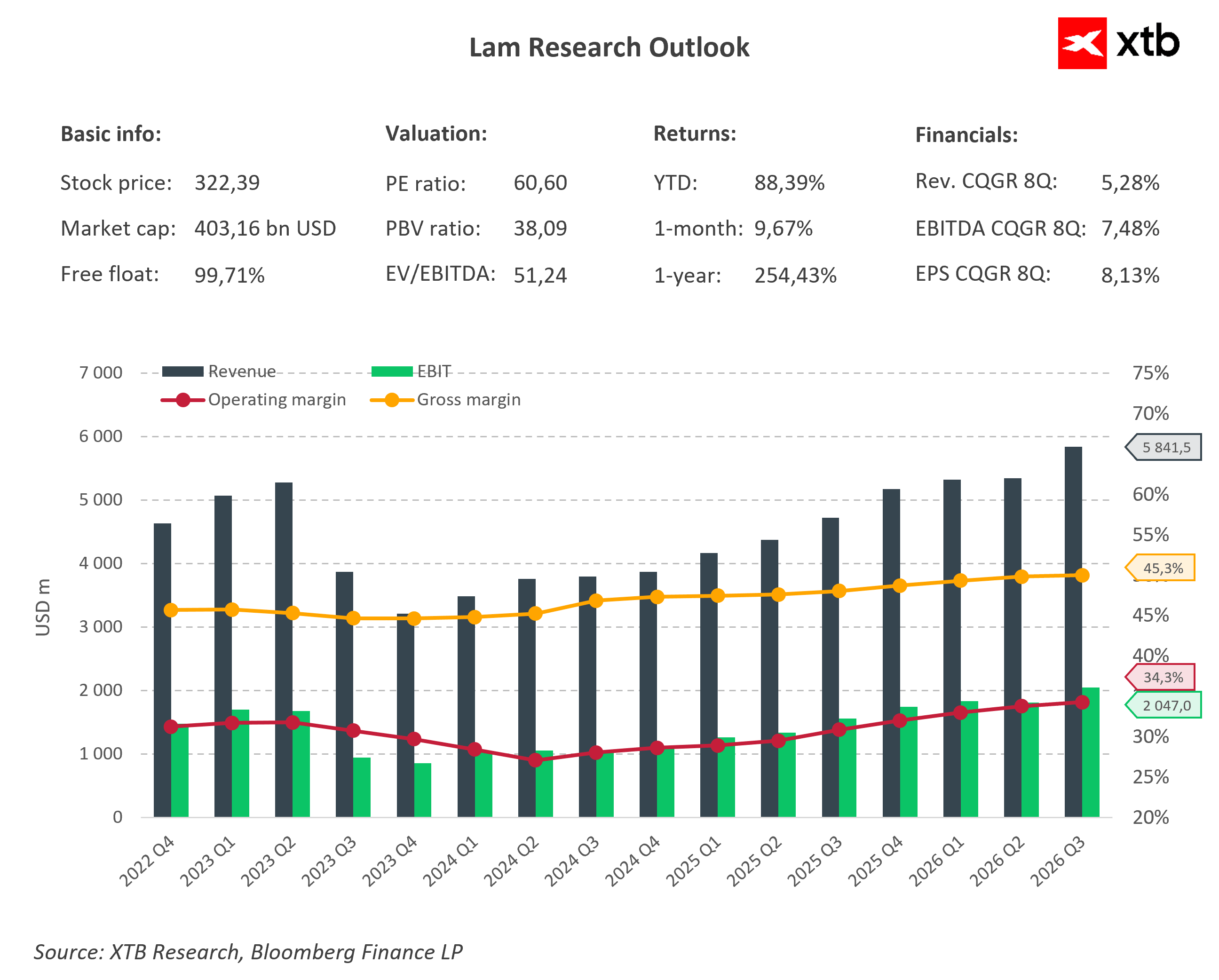

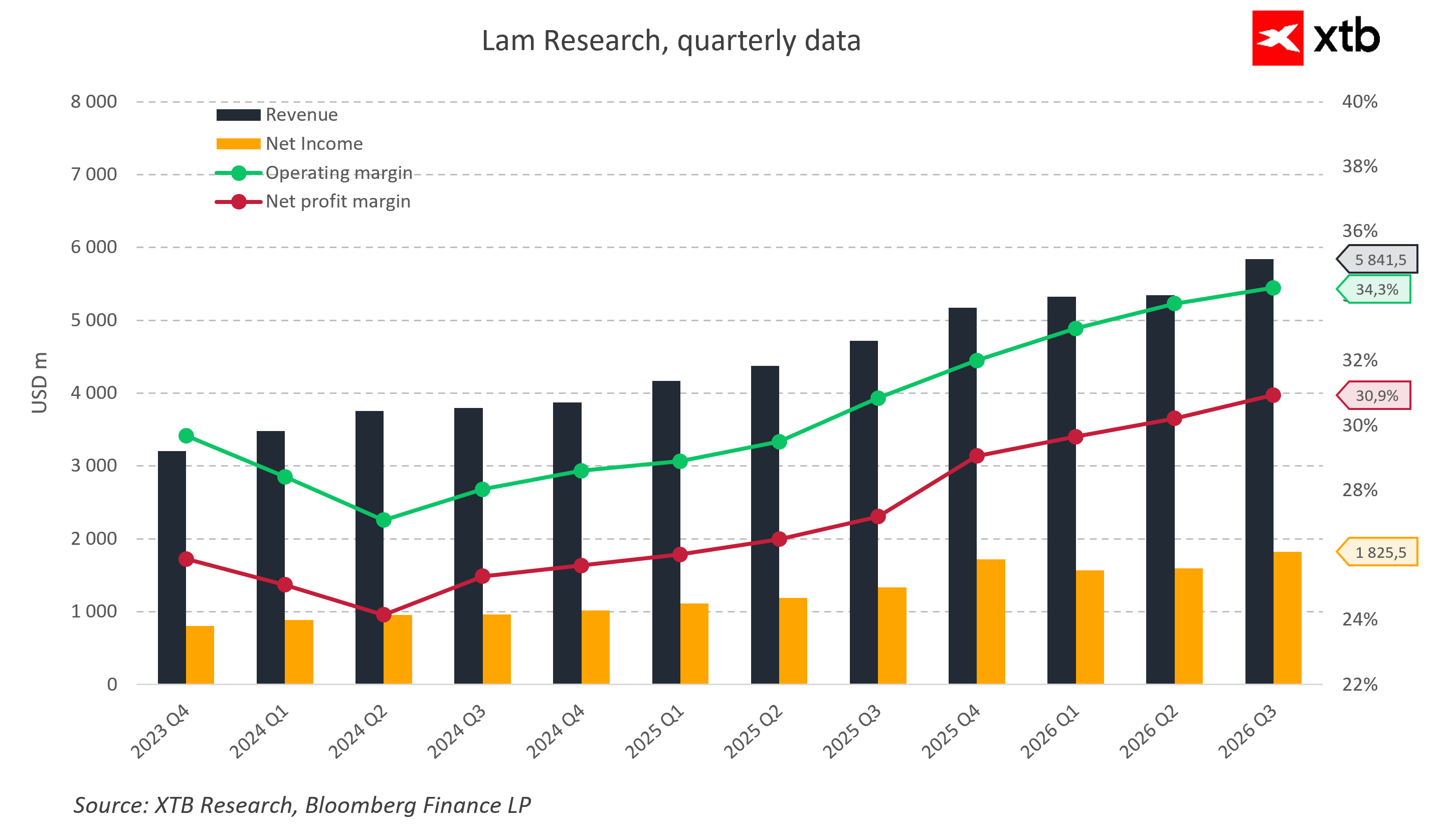

As recently as early 2024, the company’s quarterly revenues hovered around 3.5 billion USD. Today, Lam generates nearly 6 billion USD in sales per quarter. In its latest report for the third quarter of fiscal year 2026, revenues reached a record 5.84 billion USD, representing roughly a 24 percent year-over-year increase and about a 9 percent sequential increase from the previous quarter. Simultaneously, earnings per share came in at 1.47 USD, beating market expectations and the upper end of prior guidance. This combination of dynamically growing revenue and systematically beating forecasts is typically the fuel that drives valuation revisions upward.

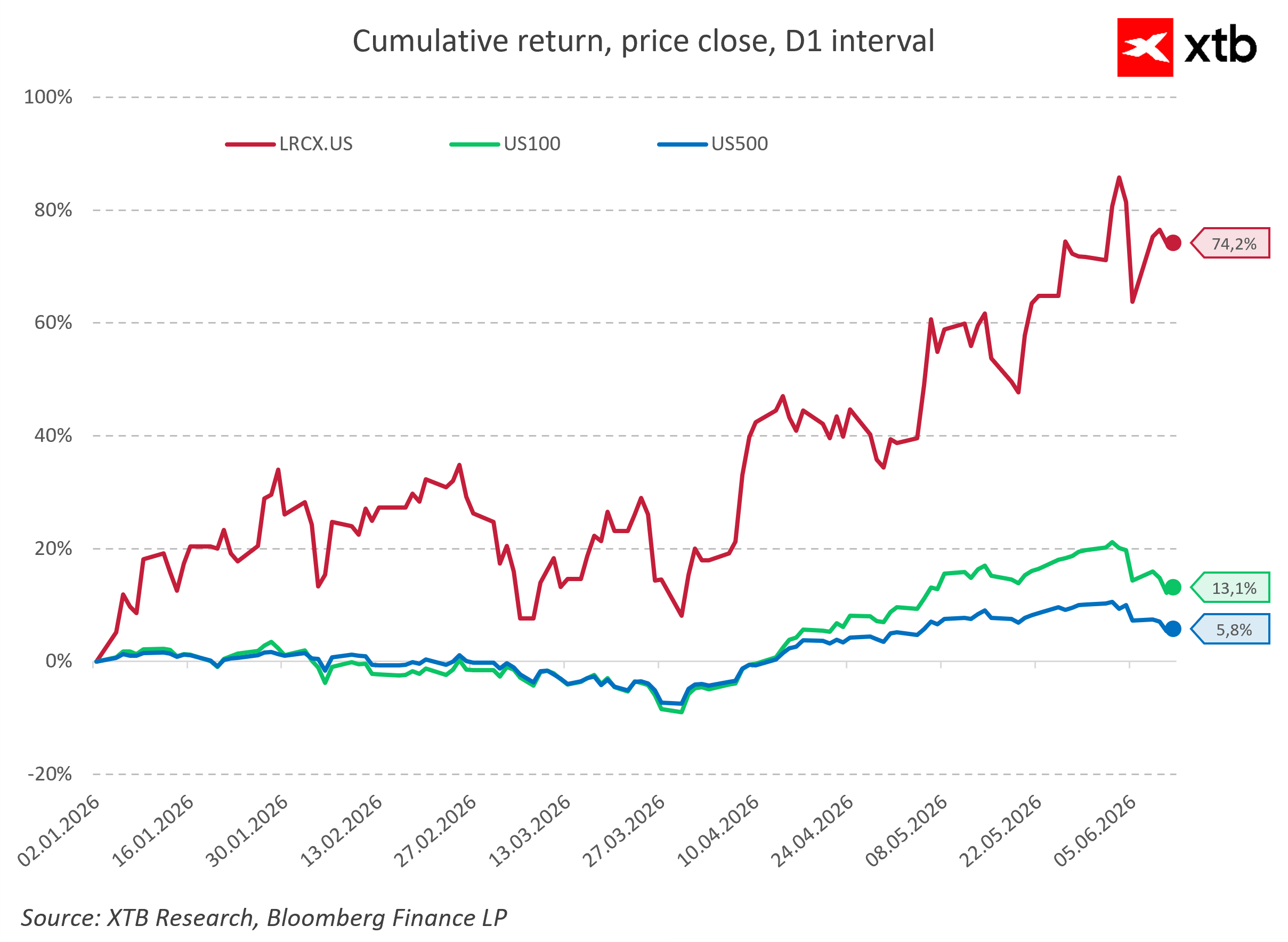

The stock price behavior only confirms this transition. Since the beginning of 2026, Lam Research shares have delivered double-digit percentage returns, clearly outperforming both the Nasdaq 100 and the S&P 500, demonstrating how quickly the market has re-rated the company’s valuation, accounting for its role in the capital expenditure super-cycle for AI infrastructure. This is no longer just standard cyclical semiconductor exposure, but a company that investors have begun treating as a primary beneficiary of a long-term megatrend.

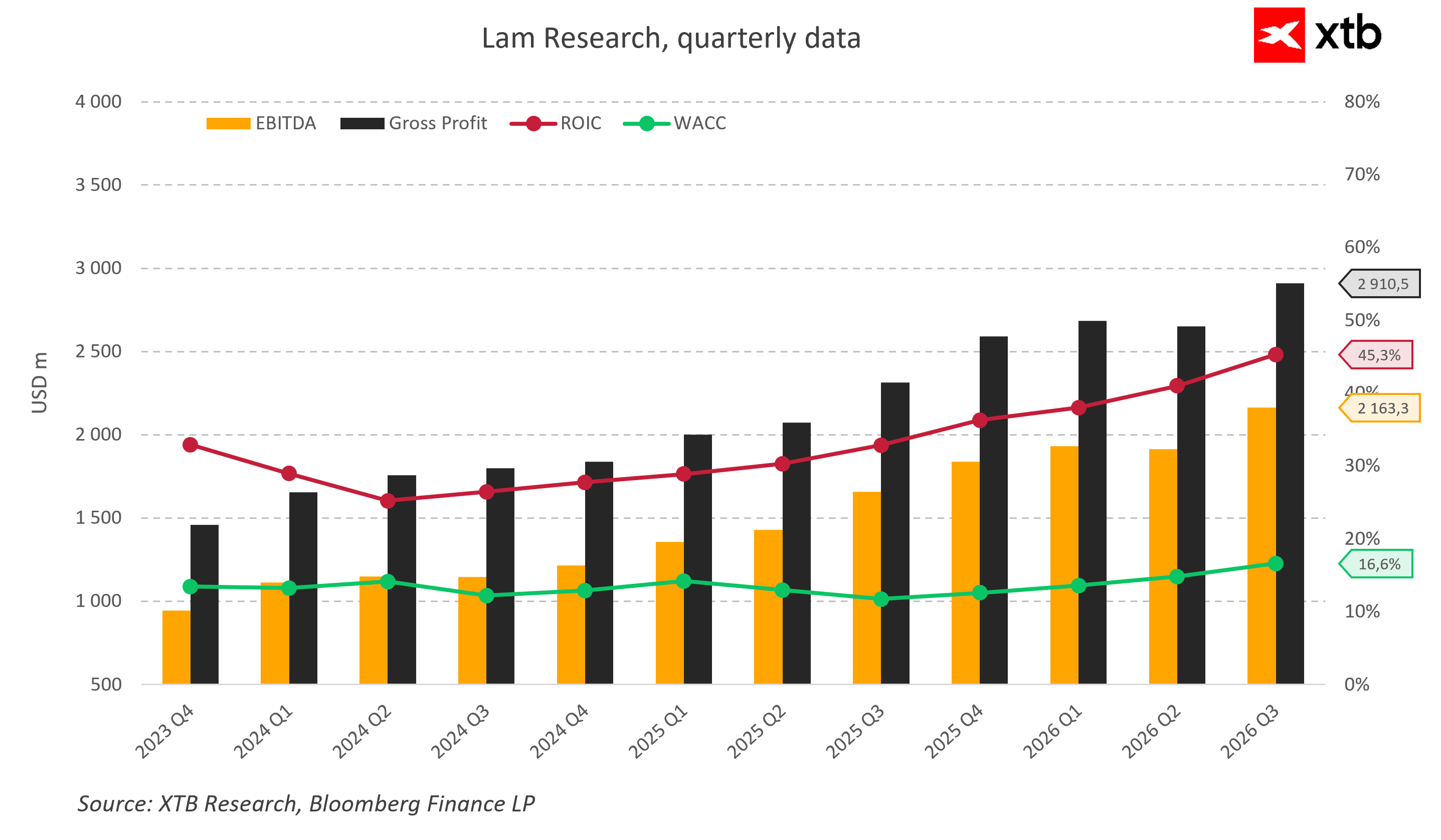

An analysis of profitability looks even more interesting. In many tech companies, rapidly expanding sales comes at the expense of margins. For Lam, we see the opposite. Operating margin has increased from levels below 30 percent in 2024 to around 35 percent currently, while gross margin has neared 50 percent, and net margin has exceeded 30 percent. This implies that each incremental dollar of revenue generates increasingly more profit for shareholders. Both an effect of scale and a highly favorable product mix are visible here. The fastest-growing segments are those tied to HBM memory, advanced logic processes, and modern packaging—areas requiring the most sophisticated etching and deposition steps, where Lam boasts its strongest competitive position.

Added to this is the expanding role of the service business. In the last quarter, the Customer Support Business Group segment crossed roughly 2 billion USD in quarterly revenue for the first time, hitting approximately 2.1 billion USD and growing 25 percent year-over-year. For investors, this is a crucial signal, as service revenues are typically more stable than new equipment sales and help smooth out the cyclical swings of the semiconductor market. A growing installed base of tools automatically converts into an expanding, predictable stream of revenue from parts, services, and upgrades.

The company’s ability to create shareholder value—measured by return on capital—looks equally impressive. The ROIC indicator has climbed toward 45 percent in recent quarters, while the cost of capital remains significantly lower, in the double-digit percentage range. In practice, this means that every dollar invested in expanding the business generates a rate of return several times higher than the cost of acquiring it. This is a hallmark of the best technology enterprises—a high, stable ROIC signals that the firm is not burning through capital, but rather consistently investing in projects with high barriers to entry and durable competitive advantages.

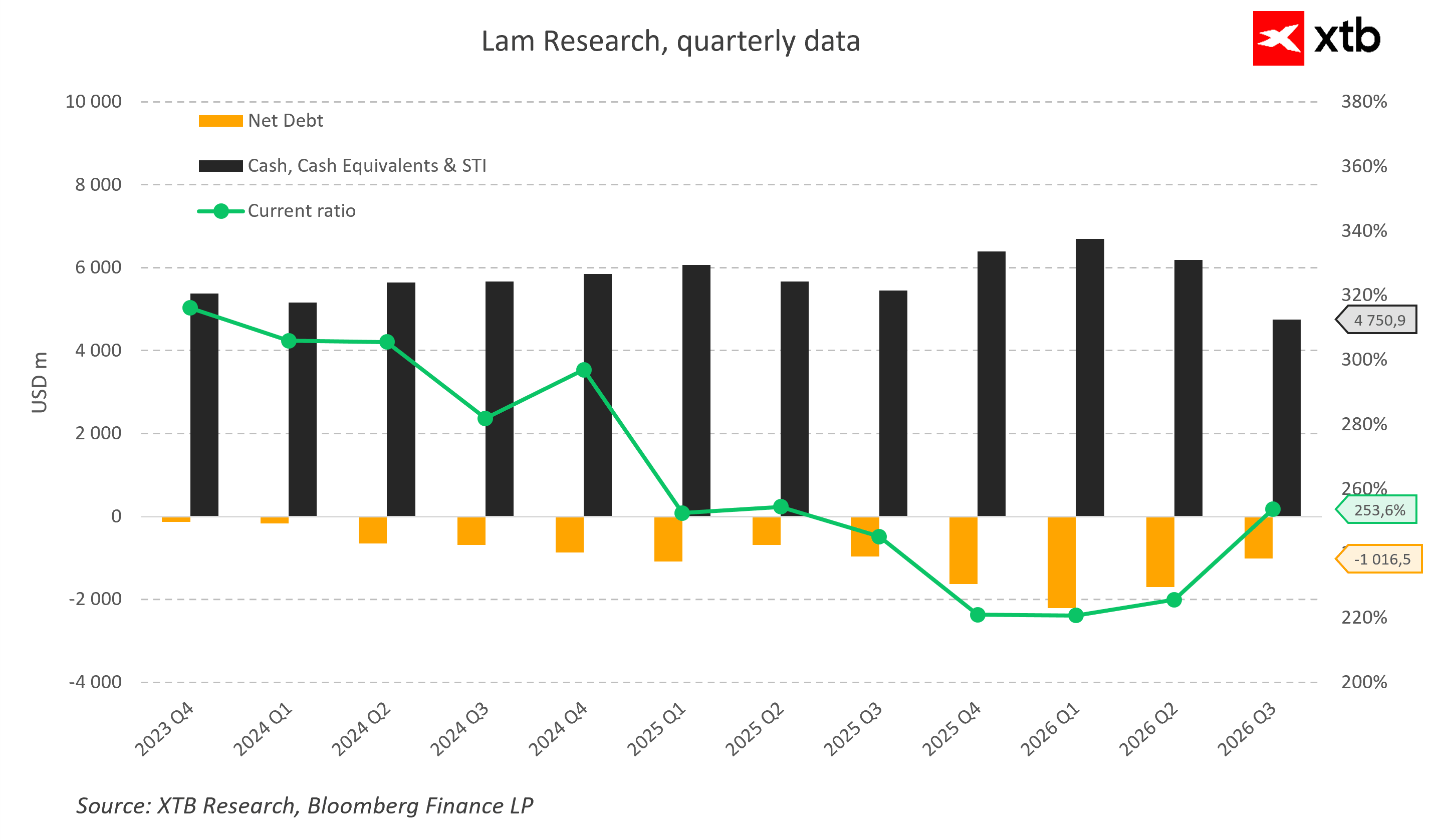

The balance sheet only strengthens this picture. Despite aggressive share buyback programs and regularly paid dividends, Lam maintains a very comfortable liquidity position. At the end of March 2026, the company held roughly 4.8 billion USD in cash and cash equivalents, and after accounting for debt, it remained in a net cash position exceeding 1 billion USD. This financial buffer gives management ample flexibility to fund capacity expansion, intensive technology development, and simultaneously return capital to shareholders.

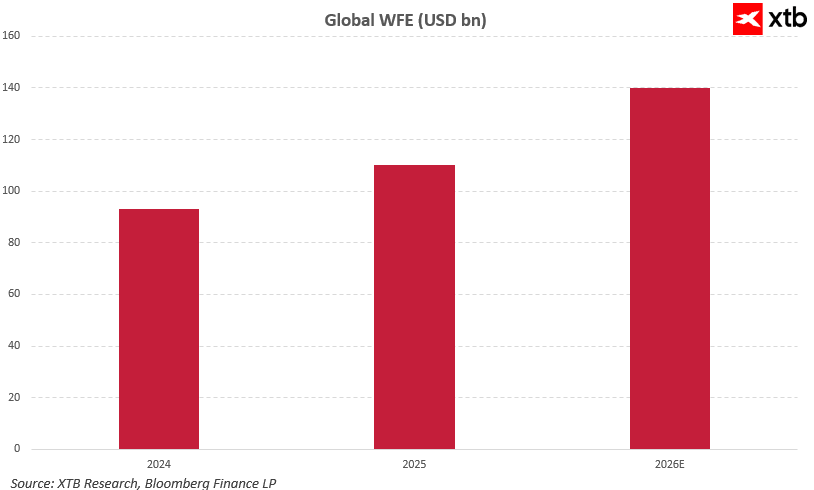

Just as importantly, management is not signaling any slowdown in demand. Along with the publication of results, they raised their 2026 WFE market forecast to approximately 140 billion USD, explicitly linking this revision to booming demand for AI chips, HBM memory, and advanced logic processes. Simultaneously, they issued revenue guidance for the upcoming quarter at 6.6 billion USD while maintaining very high margins, suggesting that the record-breaking fiscal third quarter of 2026 may be just another step in the current growth cycle rather than its peak.

Looking at the numbers alone, it is hard to miss the clear pattern. Lam Research is not simply a company riding a favorable market conditions in the semiconductor industry. Instead, the results suggest that the firm is steadily compounding its significance within the global ecosystem of advanced chip manufacturing. Revenue scale is expanding, margins are climbing, returns on capital are rising, and management is lifting forecasts for both themselves and the broader market. This is exactly the suite of metrics investors want to see in a company positioned as a core beneficiary of the long-term megatrend of artificial intelligence.

Chapter 5. Is Lam Research an Attractive Investment Today?

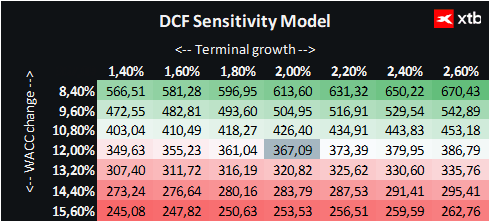

We present a valuation of Lam Research using the Discounted Cash Flow method. It should be emphasized that it is for informational purposes only and should not be construed as investment advice or a precise valuation.

After analyzing the business model, megatrends, and financial performance, the most critical question from an investor's perspective remains: does the current stock price still leave room for growth?

This question is especially pertinent for companies tied to artificial intelligence. Recent years have seen explosive valuation growth across many firms riding the AI wave, leaving investors increasingly wondering whether the market has already priced in the industry's future successes.

In the case of Lam Research, however, the situation appears more balanced. On one hand, the company capitalizes on one of the most powerful technological megatrends of recent decades. On the other hand, because it is not a direct chip manufacturer or an AI infrastructure provider, its valuation remains far more measured than that of the most recognizable poster children of the artificial intelligence revolution.

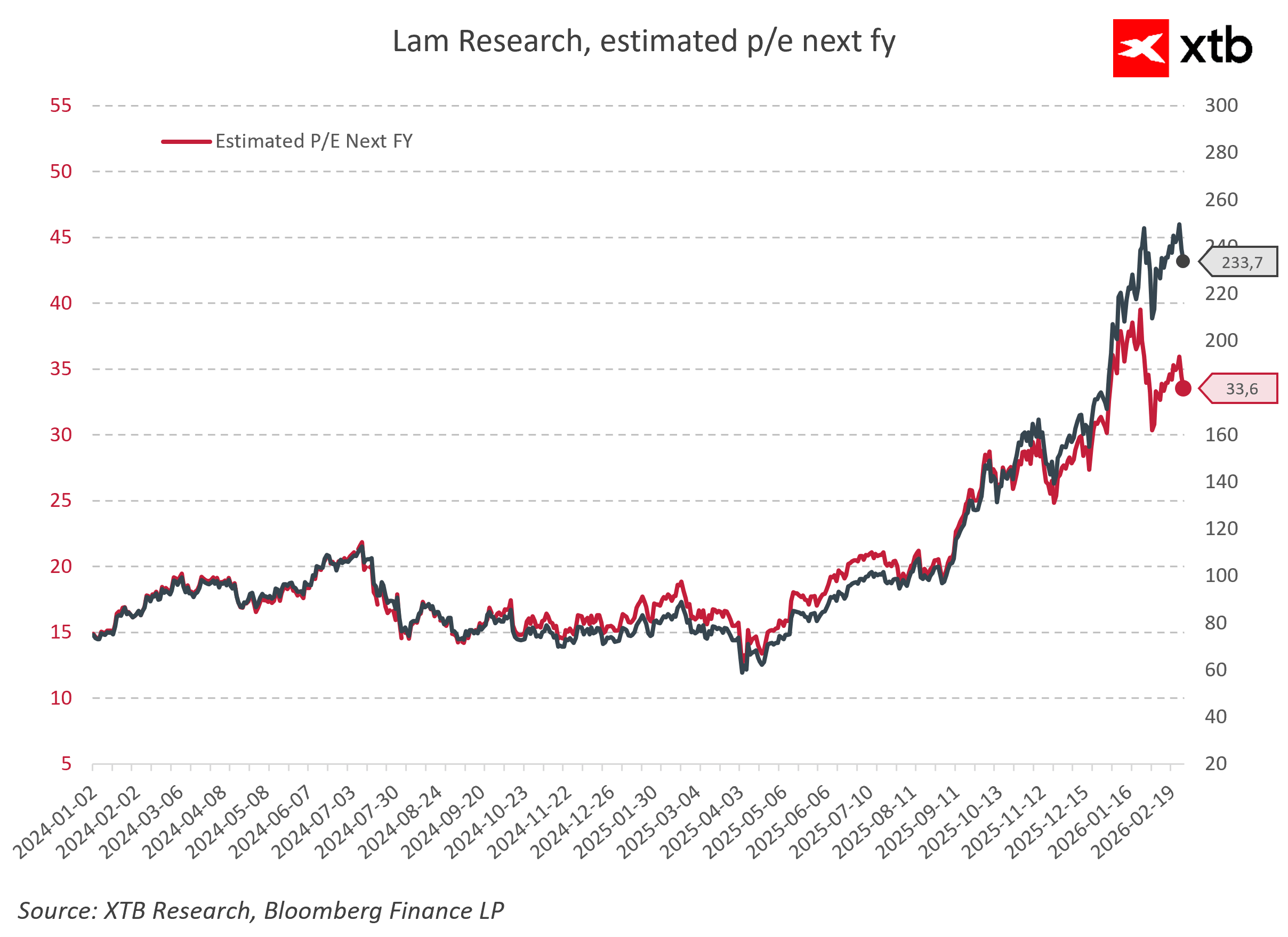

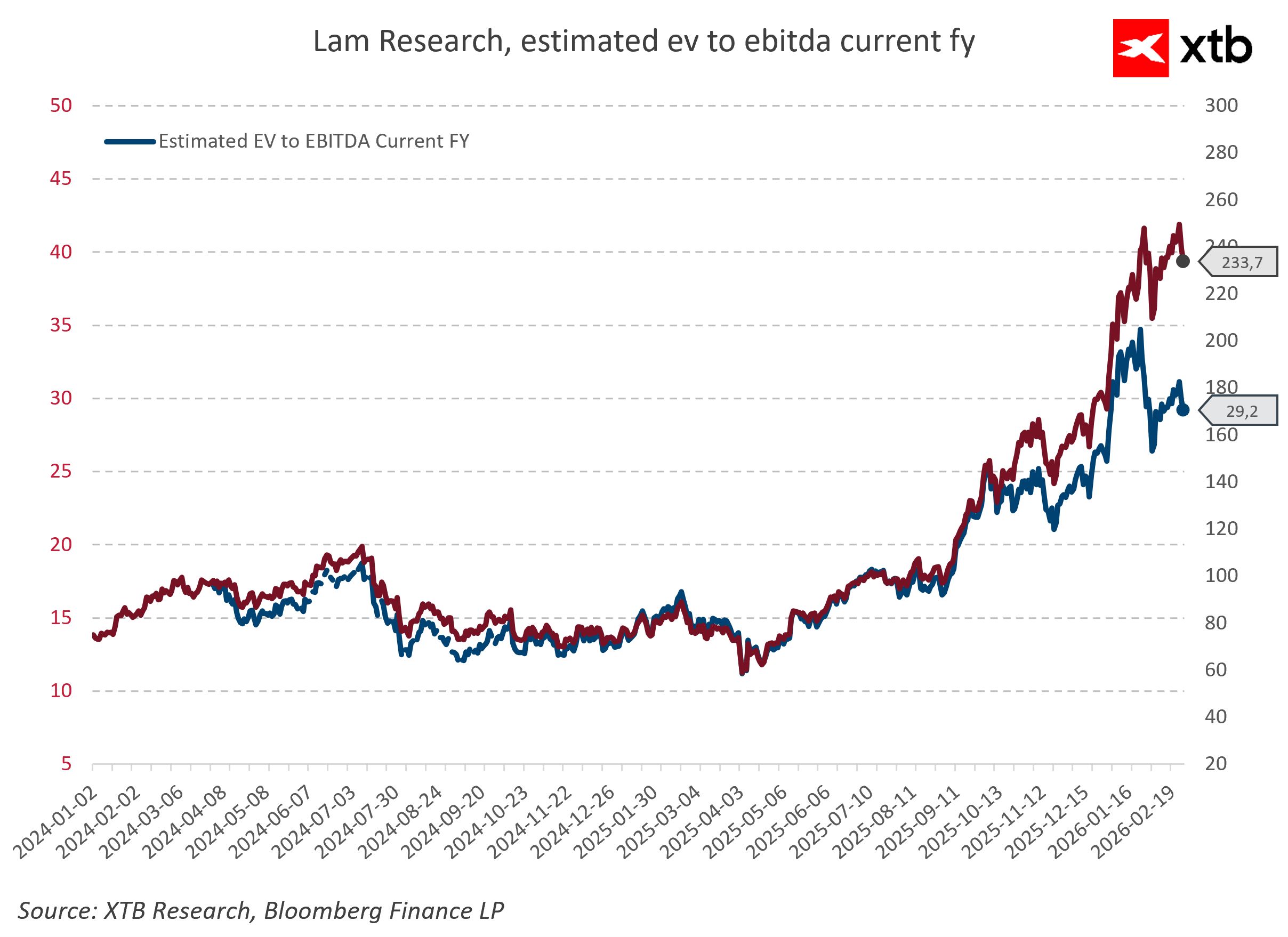

A Discounted Cash Flow analysis indicates a fair value of approximately 367 USD per share. Given the current market price of around 322 USD, this implies an upside potential of roughly 14%.

This is not a level that suggests spectacular undervaluation. At the same time, it is difficult to argue that the valuation has become detached from fundamentals. The market seems to recognize the gains stemming from the AI boom but stops short of pricing in an overly optimistic, blue-sky scenario. In practice, this means that further stock price appreciation will heavily depend on the company's ability to sustain its current revenue momentum and high profitability.

The strongest argument for Lam’s long-term appeal remains the quality of its business. The company operates in a segment defined by high barriers to entry, possesses a commanding technological position, and partners with the largest semiconductor manufacturers in the world. Simultaneously, it generates high margins, maintains a healthy balance sheet, and achieves returns on capital that significantly exceed its hurdle rate.

However, this does not mean it is devoid of risks. Despite all the structural trends supporting the semiconductor industry, Lam remains a company operating in a cyclical sector. History shows that even the best semiconductor equipment firms periodically experience order pullbacks when clients trim capital expenditures.

An important risk factor also remains geopolitics. China accounts for a meaningful portion of global semiconductor manufacturing investments, yet it remains an area subject to expanding export restrictions imposed by the United States. A further tightening of regulations could disrupt the revenue mix of the entire semiconductor equipment sector.

It is also worth keeping in mind the risk associated with the AI boom itself. Currently, most forecasts call for continued aggressive spending on data centers and compute infrastructure. Should the investment pace of the largest tech giants cool down and fall short of market expectations, it could translate into slower order books for the machinery used to build the most advanced chips.

Despite these threats, Lam Research appears to be one of the best-positioned companies to profit from the secular growth of the semiconductor market. The firm is not reliant on a single customer, a single chip architecture, or a single technology. It rides the wave of AI adoption, but concurrently draws strength from the evolution of memory, advanced packaging, supply chain localization, and an expanding base of recurring service revenues.

This allows investors to view Lam not merely as a speculative bet on artificial intelligence, but primarily as an investment in the growing structural complexity of the entire semiconductor ecosystem.

OpenAI heads into a price war ahead of an IPO?

US OPEN: A recovery after declines, Trump threatens to resume fighting with Iran

Market wrap: European stock indices try to rebound 📈 WizzAir surges 6% after earnings

CD Projekt shares hit new lows! What are investors afraid of?

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.