Copper is one of the most important metals in the world. Approximately 50% of all copper in the world is consumed in China, mainly in the construction sector, but at the same time, the entire electronics sector would not exist without this metal. What is more, with the current development of artificial intelligence and green energy, the demand for copper will grow even stronger, and in the near future, this sector will be key in terms of overall demand. Therefore, President Donald Trump's introduction of a 50% tariff on copper imports into the United States marks a turning point for the global market for this strategic metal. Although at first glance this decision seems puzzling, it is aimed at rebuilding the American copper industry and ensuring security of supply for key sectors of the economy.

Why does Donald Trump want 50% tariffs on copper?

National security strategy

The main motivation for introducing tariffs on copper is to revive the US copper industry and ensure the security of supply of this critical material. Copper is one of the most important metals in the world, used in a wide range of applications, from electrical cables and pipes to electric vehicles and energy systems.

US government officials argue that dumping and overproduction in the global market have weakened domestic copper production, leaving America dependent on foreign sources of the metal for key industries such as weapons manufacturing. While the US has significant mines, producing approximately 1.1 million tons of copper in 2024 (and refining less at 890,000 tons), consumption of refined metal reached 1.6 million tons, meaning that imports are necessary to fill the gap.

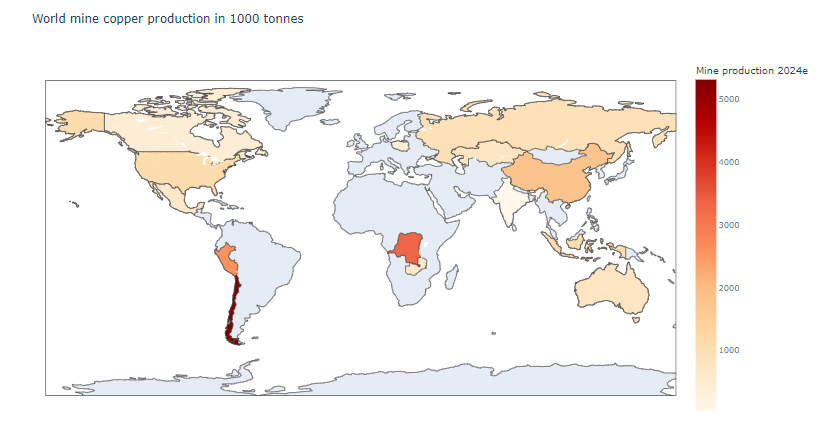

The world's largest copper producers. The key countries in terms of production are Chile, Peru, Congo, and China. The United States ranks only fifth in terms of production. Source: USGS, XTB

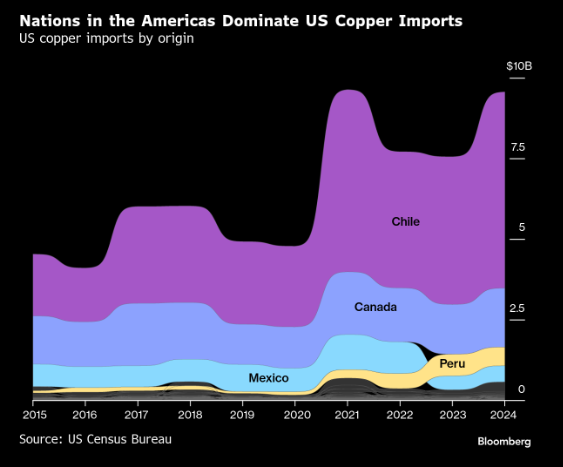

Chile is the largest supplier of copper to the US, but Canada, Peru, and Mexico are also significant players. Source: Bloomberg Finance Lp

A sharp decline in production capacity in the US

Access to cheap copper from South America, Africa, or China has made copper production in the US less profitable. As a result, we have seen a decline in US copper processing capacity over the years. As Trump's February executive order points out, the US “has abundant copper reserves, but our smelting and refining capacity lags far behind our global competitors.” The country had several operating smelters in the late 1990s, but today only two are active – one in Arizona and the other in Utah. This decline occurred as China built more and more smelters. Currently, China is the absolute world leader in refining, with production at 12 million tons. Only two countries exceeded 1 million tons of production in 2024. These were Chile, with production of 1.9 million tons, and Japan, with 1.6 million tons. Copper reserves ready for extraction are currently estimated at 47 million tons in the US, which is not the largest amount in the world, but is higher than in China (41 million tons).

Why the difference in prices on the LME and COMEX?

Strong increase in the spread between the LME and COMEX

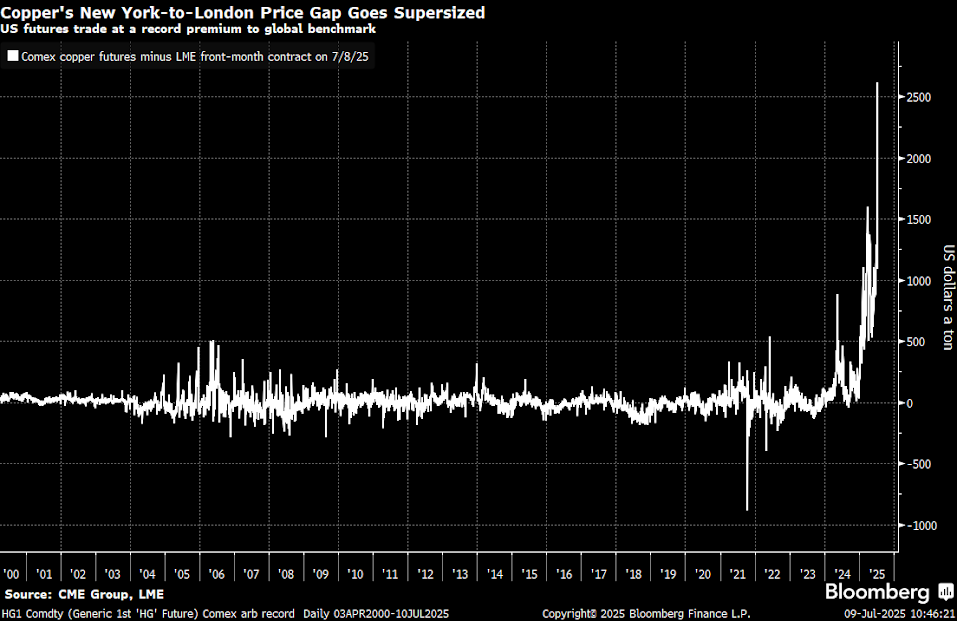

The announcement of tariffs caused an unprecedented increase in the price difference between the US COMEX exchange and the London LME. The spread between these markets rose from around $300 per ton at the beginning of 2025 to over $2,500 per ton after the announcement of 50% tariffs. What's more, the one-day increase in copper prices on COMEX was the largest in decades.

The difference between the COMEX and LME prices rose to an extremely high level of $2,500 per ton. Potentially, this could mean a divergence in the future that will be closed. It is also worth noting that the difference is not only due to the increase in prices on COMEX, but also to the decline in prices on LME. Source: Bloomberg Finance LP

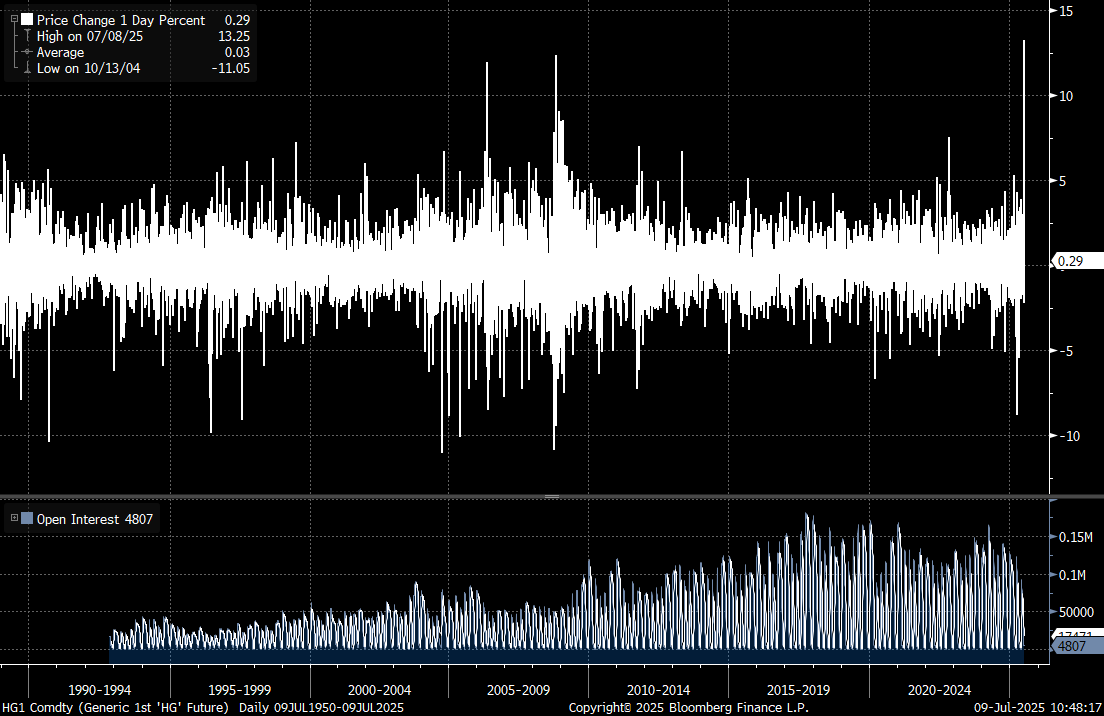

The double-digit price increase on COMEX during the July 8 session was the largest since 1990. Source: Bloomberg Finance LP

The annual price increase on COMEX is over 70%, while on LME we see a sideways trend. The biggest differences appeared in January and only briefly in April, when Trump announced the suspension of tariffs, did the difference decrease significantly. Source: Bloomberg Finance LP

Reasons for the decline in prices on LME

Copper prices on the London Metal Exchange (LME) are falling for several key reasons:

1. Redirection of supplies to the US

The announcement of tariffs caused a massive redirection of copper supplies to US ports before the tariffs came into effect. According to estimates by Mercuria Energy Group, at the end of March, approximately 500,000 tons of copper were on their way to the US, compared to normal monthly volumes of approximately 70,000 tons. Of course, this has also led to a shortage of copper on other exchanges recently, which has led to a rise in the spot market.

2. End of trade arbitrage

As Shanghai Metals Market analyst Michael Wu notes, “there are few buyers in Asia willing to ship copper to the US, given the short time remaining before the tariffs take effect.” This marks the end of a long-running trade arbitrage that has been pulling metal out of global markets.

3. Release of supply outside the US

Copper in the US must currently be more than 50% higher if it is to remain profitable to continue to ship copper to that market, hence the very large increase on COMEX. At the same time, prices are not that high, and the US could potentially achieve independence from suppliers in the coming years. Countries such as Peru, Chile, and Congo will have to find other markets for ore shipments. The same applies to refined copper, primarily from China.

Price outlook

Goldman Sachs analysts predict that the COMEX-LME spread could reach 25-35% of the LME price, or $2,300-3,300 per ton, compared to earlier forecasts of 15-20%. At the same time, they forecast that LME prices will peak at around $10,050 per ton in August 2025. Citi, on the other hand, indicates that LME prices may fall below $9,000 per ton, specifically to $8,800 per ton. This will be due to the fact that the large US market will not be reporting demand at this point, given the high inventories built up in recent months.

At the same time, however, it is not known what the specific shape of copper tariffs will be. Will it apply equally to ore or only to copper products? If tariffs are limited, this may lead to a reduction in the difference between COMEX and LME prices, although primarily in the form of a decline in prices in the US.

Impact on copper companies

KGHM – between benefits and challenges

For the Polish copper giant KGHM, the situation is twofold. On the one hand, the company can currently benefit from higher global copper prices and the potential redirection of supplies from the US to other markets. KGHM shares are currently up by about 5% since the beginning of Trump's term, while since the April low, the company's shares have risen by as much as 30%. However, the company remains well below the recent local price peaks of 2024 or the historical peaks of 2021 above PLN 200 per share.

KGHM, as the eighth largest copper producer in the world with a production of 730,000 tons in 2024, may benefit from:

- The potential for price increases in global markets in the event of a smaller impact of US tariffs

- The United States was the fifth largest market for KGHM, which is one of the leaders in the European copper market. KGHM may potentially focus on Asian countries.

- KGHM is present in the US through two mines: Robinson in Nevada and Carlota in Arizona. Local price increases on the market work to KGHM's advantage.

- The current situation may favor a potential reduction in the copper tax in Poland.

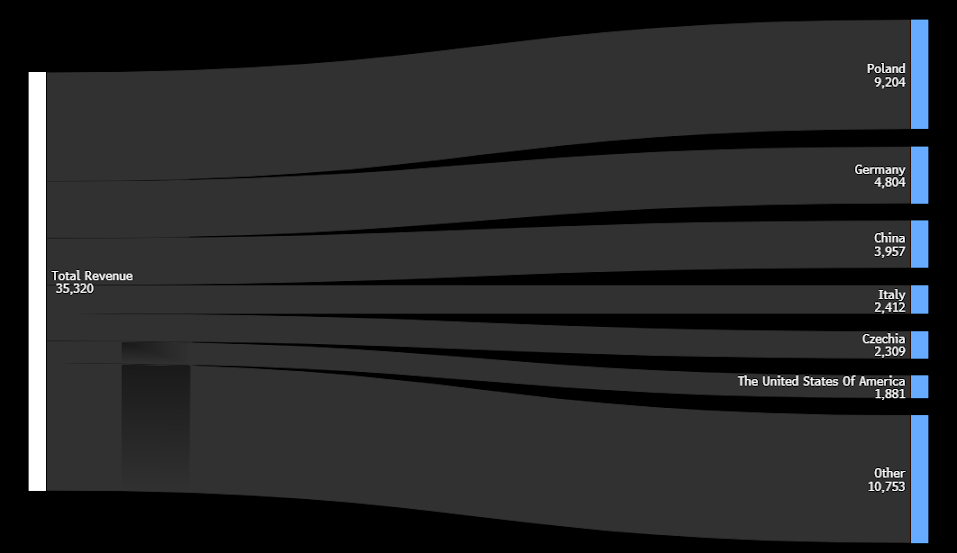

The United States is of limited importance to KGHM's results, although the company itself is also present in that market locally. Source: Bloomberg Finance LP

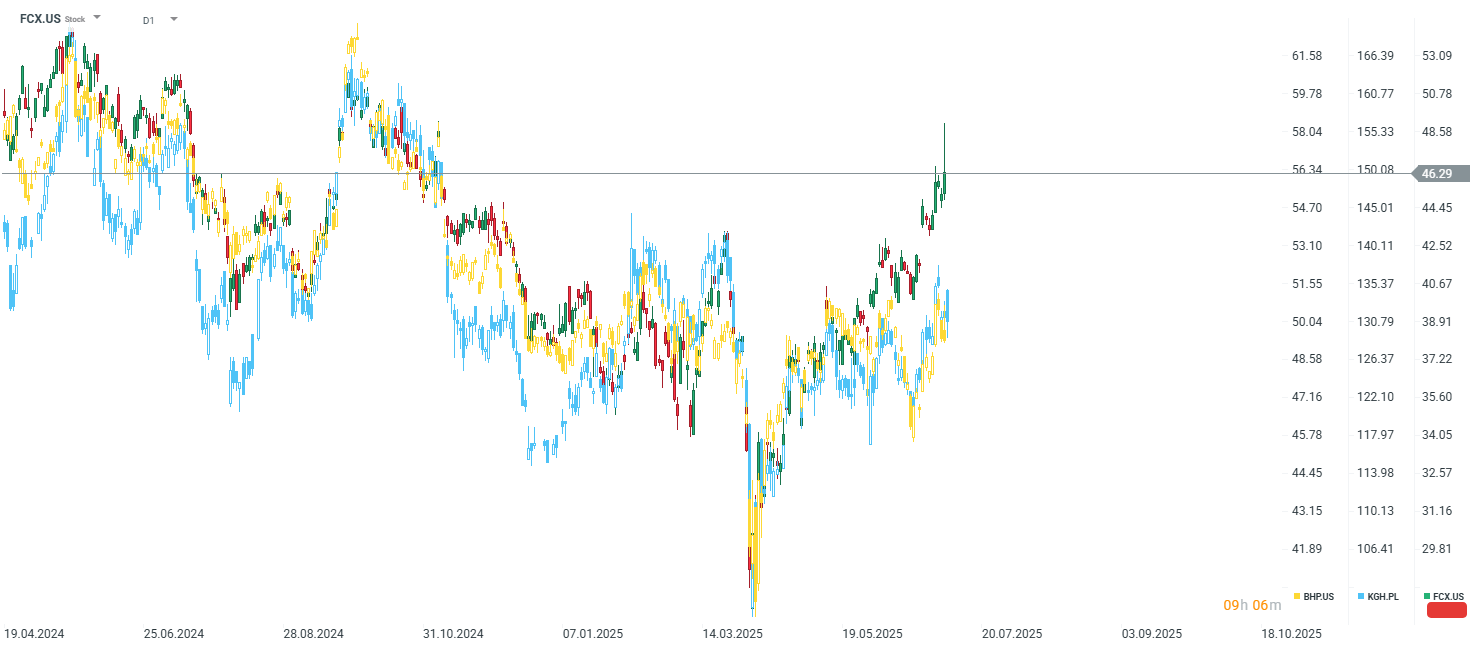

Even with limited increases in LME copper prices, KGHM's prices performed slightly worse, which can be partly attributed to the overly strong Polish zloty. Source: xStation5

US producers - the main beneficiaries

Freeport-McMoRan is one of the companies that stands to gain significantly from the tariffs. The company, which accounts for about 70% of processed copper in the US, could benefit from a premium of about $800 million per year with a spread of 13%. Freeport-McMoRan shares rose 2.5% after the tariffs were announced.

Southern Copper Corporation may also benefit from its US operations, despite potential export problems from Mexico and Peru. However, the company lost nearly 1.5% in value on the day the tariffs were announced.

Global players - mixed outlook

For global leaders such as BHP, Codelco, and Glencore, the situation is more complicated. While they may benefit from potentially higher global copper prices, they are losing access to the lucrative US market. Codelco, the largest exporter of copper to the US, has already expressed concern about the announcement of tariffs. However, the company is a Chilean state-owned company and is not listed on the stock exchange. BHP and Glencore shares have lost value.

Freeport-McMoran shares have recently performed significantly better than KGHM or BHP shares. Source: xStation5

Long-term outlook for the copper market

The International Copper Study Group (ICSG) forecasts that the global copper deficit will reach 289,000 tons in 2025, more than double the 138,000 tons in 2024. At the same time, demand for copper is expected to grow by over 40% by 2040, requiring the launch of around 80 new mines and investments of $250 billion by 2030. The main driver of the copper market is expected to be the new technology sector. The expected significant increase in demand prices with limited production prospects may mean that in the long term, copper prices can be expected to be significantly higher than at present.

Conclusions – opportunity or threat?

For copper companies, copper tariffs represent both an opportunity and a threat. Donald Trump's actions show how important and strategic copper may be in the near future. The price increase on the US COMEX shows how strong the long-term prospects are for the global copper market if there is no growth in supply in the near future. At the same time, the enormous uncertainty associated with tariffs will not encourage global companies to invest.

XTB Poland, HQ

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

Alphabet shares are down 22% from their all-time high 🚩 Is Google ready to resume its bull run?

SAP earninigs: The cloud shows strong demand, margins remain under pressure

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.