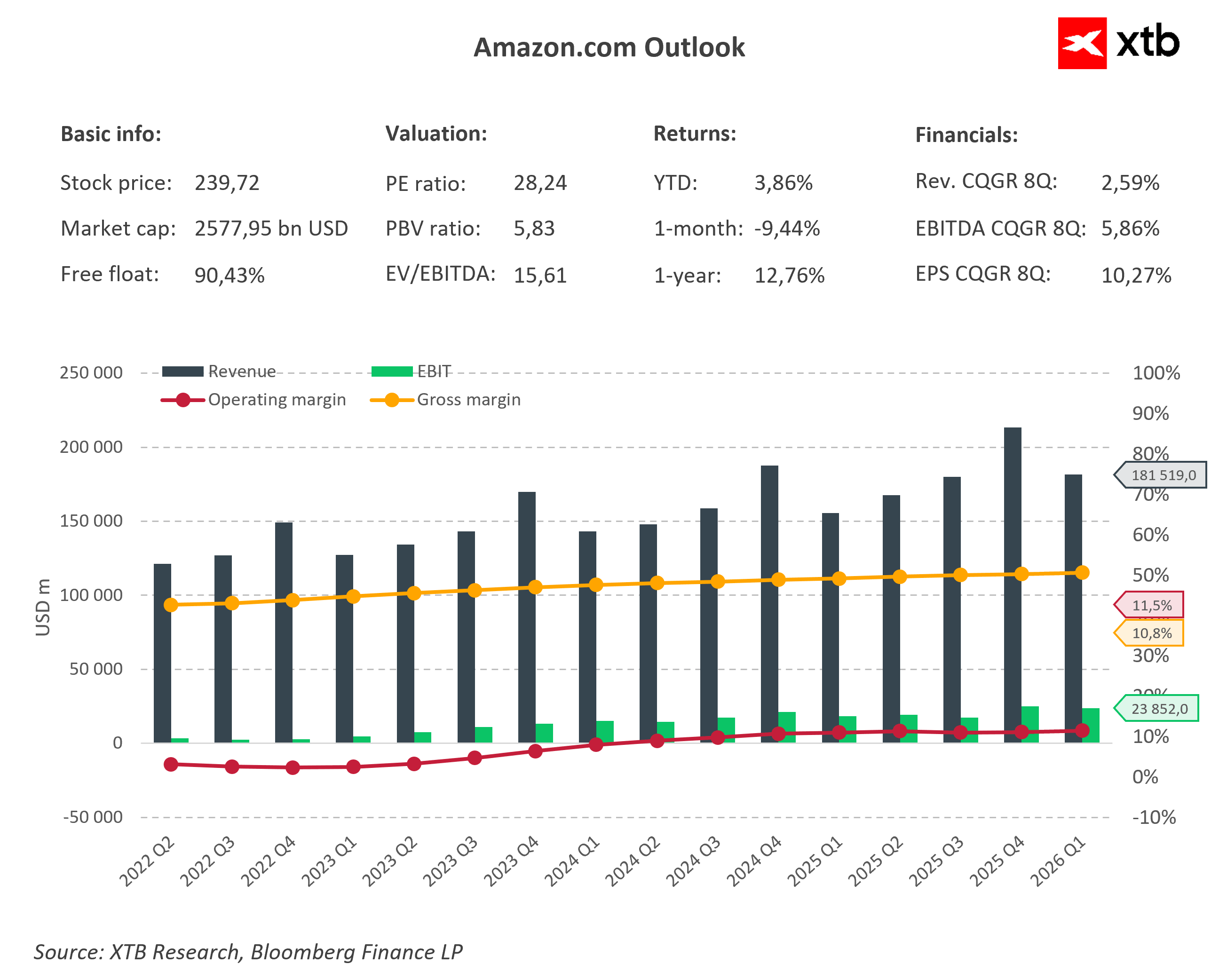

Amazon is in talks to sell its proprietary AI chips to external data center customers. This move could signal a major shift in the balance of power within the artificial intelligence infrastructure market and intensify competitive pressure on Nvidia.

According to available reports, this initiative would expand the current business model, where Amazon’s custom silicon—such as Trainium—is utilized primarily within Amazon Web Services (AWS). The company is now considering making these chips available to other entities building out their own AI infrastructure.

At first glance, this may look like a natural evolution of AWS’s ecosystem strategy, but the broader implications are far-reaching. If Amazon commercializes its own AI accelerators, it would transition from a closed cloud infrastructure vendor into a direct merchant market competitor in a semiconductor landscape currently dominated by Nvidia.

A Long-Term Shift in Tech Demand Structure

From Nvidia’s perspective, the primary threat is not an immediate risk of revenue loss, but a fundamental alteration of long-term market demand.

-

The Traditional Hyper-scaler Model: For years, Nvidia's exponential growth model relied on hyperscalers like Amazon, Microsoft, Google, and Meta acting strictly as high-volume buyers of its GPUs rather than direct rivals. This dynamic guaranteed massive pricing power and insulation for Nvidia.

-

The New Dual-Competitor Era: Amazon's entry into the merchant chip market accelerates a more complex model where cloud giants not only lease compute capacity but design, build, and distribute alternative AI hardware stacks. In practice, Amazon ceases to be just an Nvidia customer and pivots into a partial competitor.

This trend mirrors a macro shift sweeping across the tech sector. Hyperscalers are aggressively scaling up investments in custom silicon to insulate themselves from supply shortages, mitigate soaring Nvidia costs, and optimize efficiency for specialized internal workloads. The potential commercialization of these proprietary chips represents the next frontier of this strategy—moving past captive consumption to capture open market share.

Strategic Alternatives for AWS Infrastructure

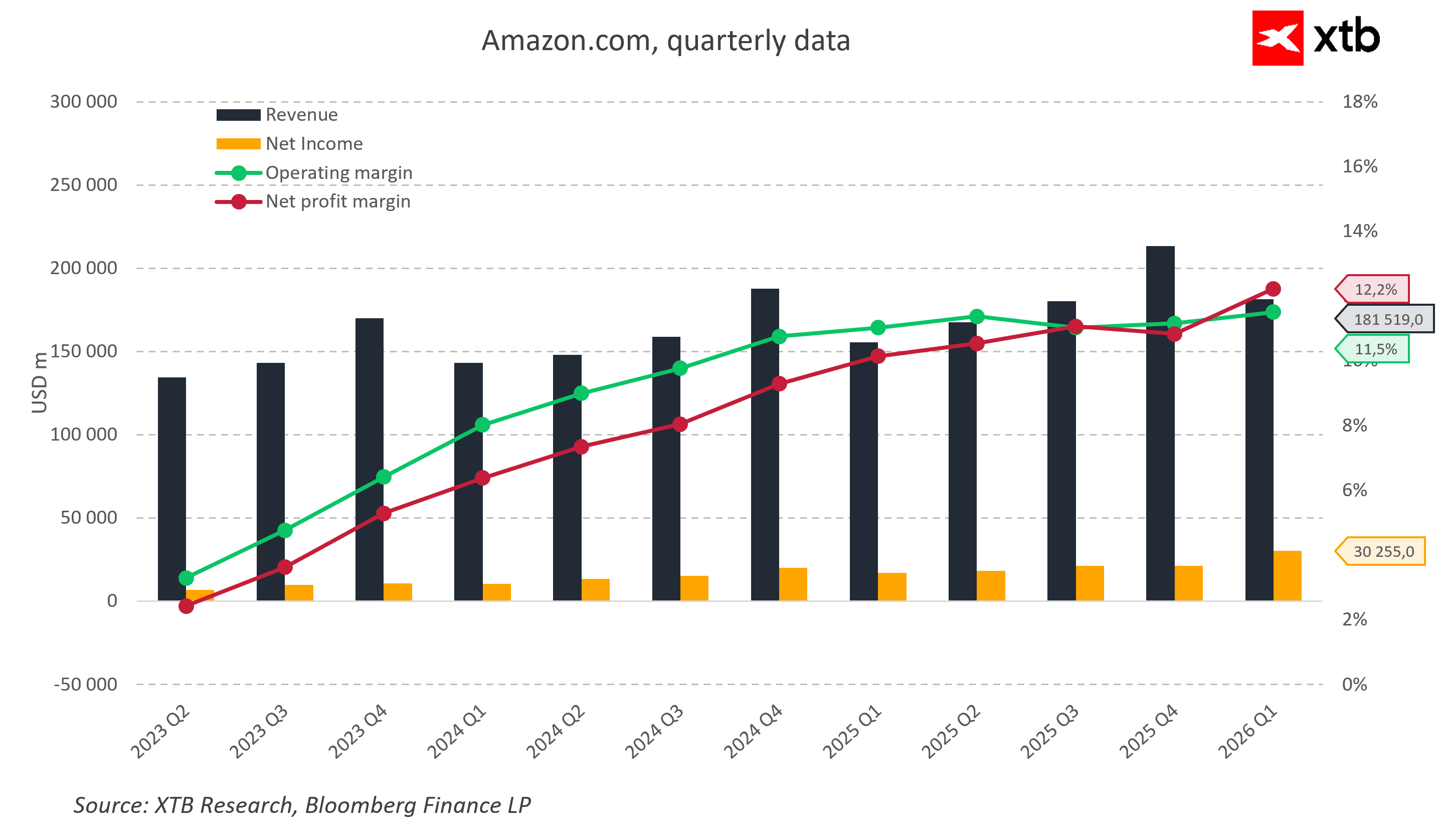

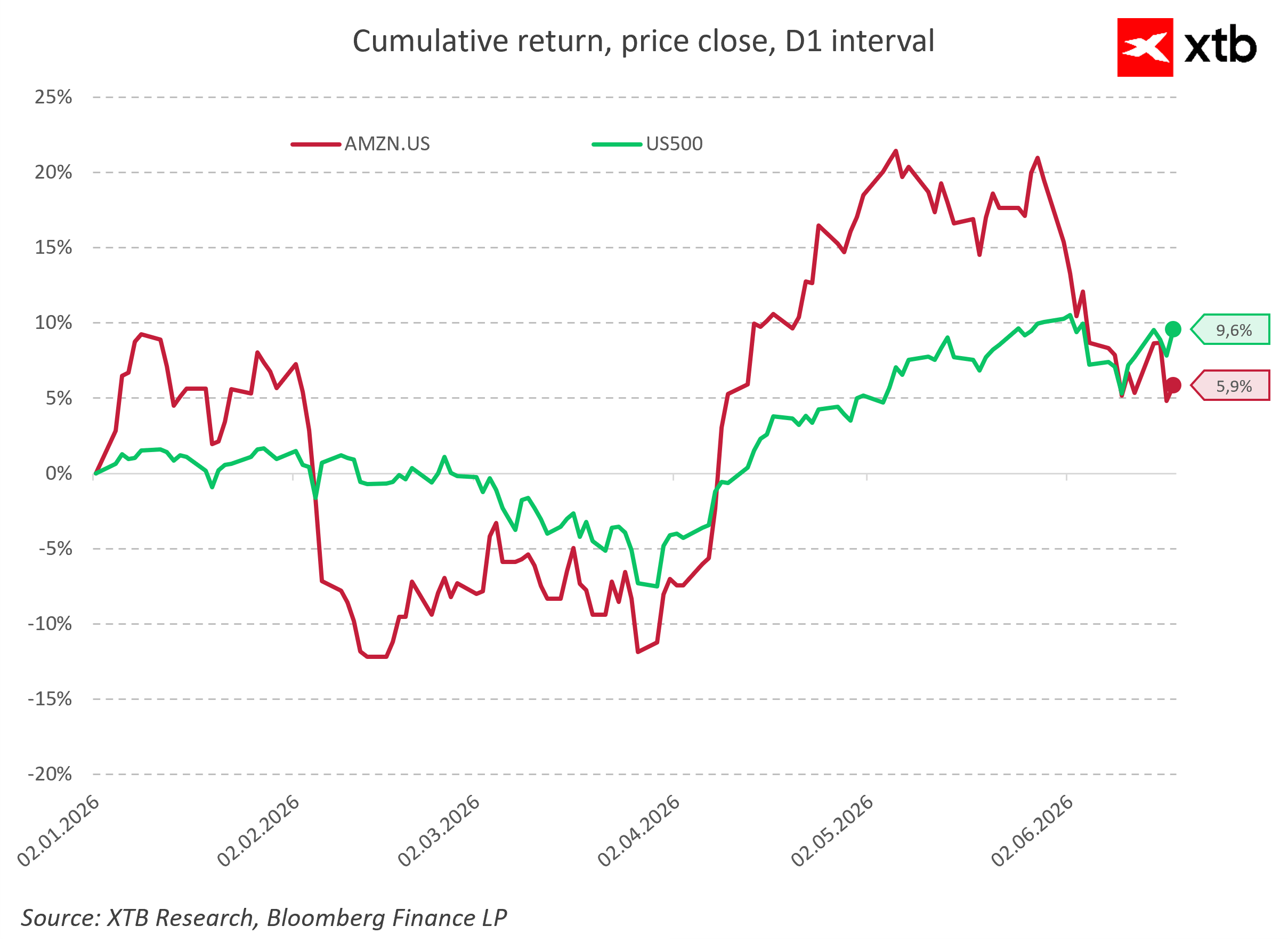

Amazon’s chip division is already growing dynamically under the AWS umbrella. The company is currently deploying a dual-track strategy: rapidly iterating its own architecture while concurrently utilizing Nvidia's bleeding-edge systems. This demonstrates that Amazon is not abandoning Nvidia in the near term, but is instead systematically weaponizing a secondary alternative to bolster its future supply independence.

For Wall Street investors, the critical question is whether this is merely an extension of internal AWS infrastructure optimization or the starting gun for a broader enterprise strategy where Amazon actively competes with Nvidia for raw silicon sales to third-party data centers.

In the long run, the significance of this development goes far beyond a new hardware revenue line for Amazon. If successful, it could gradually erode Nvidia’s near-monopoly—not through a direct price war, but by structurally decentralizing how global AI infrastructure is engineered, deployed, and consumed.

Current Market Standing

For now, Nvidia’s competitive moat remains exceptionally deep. The firm continues to dictate the performance benchmark for high-end AI acceleration, and the vast majority of cloud ecosystems remain deeply tethered to its proprietary CUDA software stack. Nonetheless, Amazon's exploratory move serves as another clear signal that the AI hardware market is inexorably drifting toward greater fragmentation and deep vertical integration among mega-cap cloud providers.

Daily Summary: Dollar at 1-year high, stocks rebound on renewed risk appetite 🚀 (18.06.2026)

Stock of the Week: KLA Corporation and the Economics of Error in the Age of Artificial Intelligence

US OPEN: Indices Recover Amid More Expensive iPhones and GTA 6 Preorders (18.06.2026)

Accenture shares sink after earnings

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.