Markets are currently focusing more on the losses resulting from the ongoing conflict in the Persian Gulf. This instinct is entirely understandable, wars, ultimately, are costly negative-sum undertakings. Investors must price in losses to budgets, risks to growth, inflation, etc.

The market participants that can generally only benefit from such a major escalation of tensions are defense companies. This time is no different.

The U.S. and Israeli campaign in Iran remains, for now, primarily an air campaign. According to official data, the U.S. conducted, up to the ceasefire, more than 10,000 combat missions and struck over 13,000 targets in Iran.

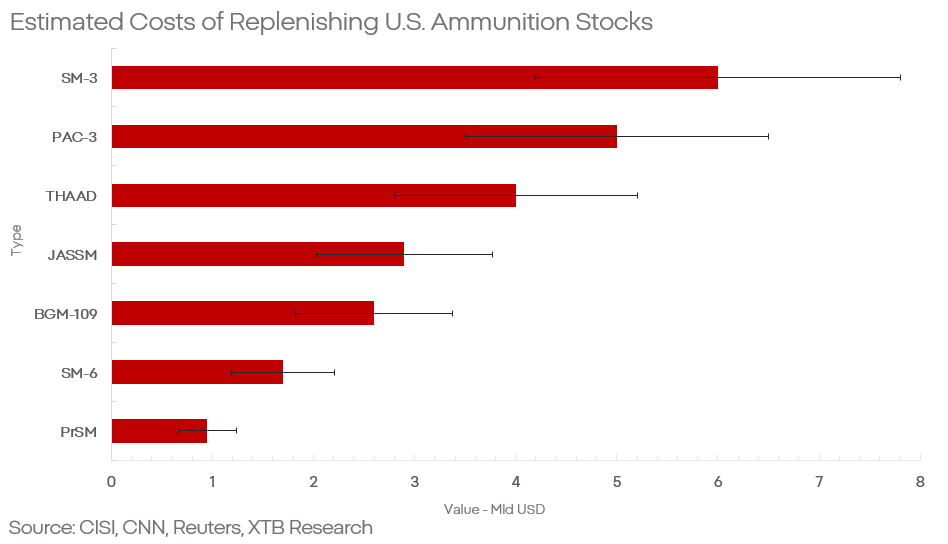

Ammunition is currently one of the most important bottlenecks in the defense industry, and the U.S. is no exception. According to analyses by, among others, CNN and CSIS, during Operation “Epic Fury” the U.S. used in Iran:

- more than 1,000 BGM-109 “Tomahawk” missiles,

- more than 1,000 “JASSM” missiles,

- approx. 60 “PrSM” missiles,

- nearly 250 SM-3 missiles,

- more than 200 SM-6 missiles,

- more than 200 “THAAD” interceptors,

- more than 1,000 PAC-3 “Patriot” missiles.

This means that among the most advanced types of munitions, mainly long-range systems, the U.S. has now depleted roughly 30–60% of its pre-war stockpiles. However, this is not the Pentagon’s biggest problem. The problem is that these munitions are not only extremely expensive, but their production is also limited to only a few dozen units per year. With current production capacity, the U.S. will need roughly four years to rebuild stockpiles.

This in no way means the U.S. is becoming “defenseless” or even ineffective. Nor does it mean a renewed escalation in Iran is unlikely. It does, however, highlight significant challenges for the Department of Defense and enormous opportunities for weapons suppliers to U.S. forces. Who are we talking about?

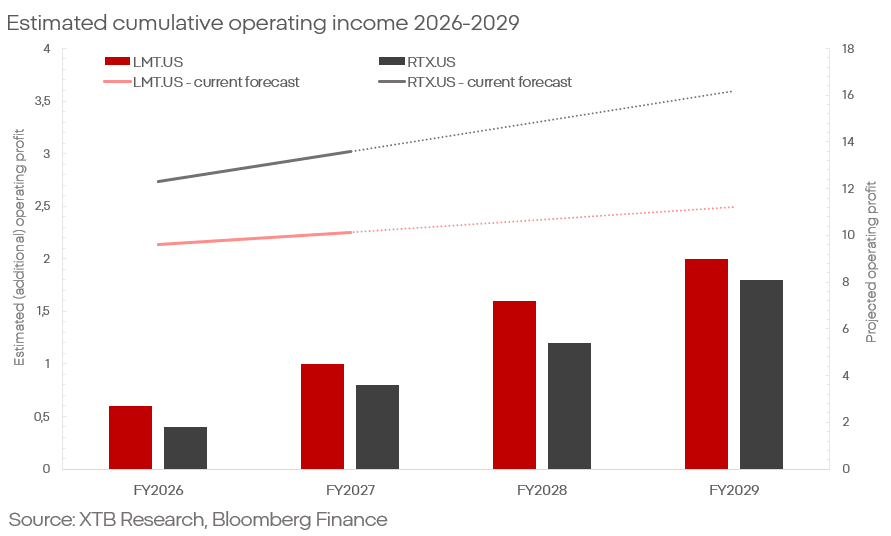

Among producers of the most advanced U.S. munitions, RTX Corp. and Lockheed Martin maintain near-total dominance.

- Tomahawk, SM-3, and SM-6 are products of RTX Corp.

- JASSM, PrSM, THAAD, and PAC-3 Patriot are associated with Lockheed Martin.

Considering only stockpile replenishment, and based on publicly available data on prices and past orders - this implies amounts of roughly $20–30 billion over aprox. four years.

Assuming a conservative $25 billion, that would translate into sales revenue of roughly $11–13 billion for RTX and roughly $13–16 billion for Lockheed Martin.

Using segment margins at these companies (12–13%), this implies operating profit of about $1.5–2.5 billion over the next four years, i.e., about $0.4–0.6 billion per year.

A high degree of caution is warranted regarding the timing of these revenues. While production of the listed munitions is currently one of the Pentagon’s most pressing bottlenecks, major investments are underway intended - at least partially, to accelerate output.

The key question to answer is: is this already in the price?

Nothing suggests it is. Both companies appear to have performed weakly in recent quarters (given the context), and the trend worsened after the latest results.

Because, based on forecasts for, among other things, the operating profit of both companies, it does not appear to have changed materially recently.

- For Lockheed, expectations for 2026 and 2027 are $9.6 billion and $10.1 billion, respectively.

- For RTX, expectations are $12.3 billion and $13.5 billion for 2025/2026.

If so, this implies a potential upside surprise of about $0.4–0.6 billion (~5%) in operating profit—an upside that the market does not currently see—at a time when both stocks are at multi-month lows.

Final remarks

Naturally, forecasts of this kind are not “absolute.” Neither RTX nor Lockheed is a company focused solely (or even primarily) on munitions—earnings forecasts can be diluted by the performance of other segments.

Moreover, there is no high precision in estimating expenditures of this type. The specifics of producing these missiles are highly classified, margins are averaged, and many operational issues can appear or disappear unexpectedly without investors or the public being informed.

Kamil Szczepański

Financial Market Analyst at XTB

Daily Summary: A sell-off with a spin-off

Iran Escalation: What to Watch and What to Expect

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

Fed Chair Kevin Warsh’s Q&A from Congress Testimony: Inflation stability is a key

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.