Home Depot (HD.US) kicked off its 2026 financial year with results which — whilst not spectacular — say more about the market than many a macroeconomic indicator. The company generated revenue of $41.77 billion, representing a 4.8% year-on-year increase and slightly beating consensus estimates. Adjusted earnings per share came in at $3.43 against an expected $3.41 — a modest result, but above the line. In an environment where consumers are tightening their purse strings, every cent above estimates counts.

The key takeaway, however, is not so much the result itself as the fact that the full-year forecast has been confirmed. Home Depot continues to forecast comparable sales growth of 0–2% and EPS growth of 0–4%. This sounds modest, but in an environment of rising interest rates, pressure on the housing market and consumer uncertainty — maintaining guidance is an act of courage and a clear signal to the market. For the sector, this is an optimistic message: the company sees demand stabilising, rather than continuing to collapse.

Behind these figures, however, lies something more significant — a snapshot of the average American. Home Depot is neither a luxury nor a technology company — it is a barometer of the state of the US middle class. When people are renovating their bathrooms, replacing their roofs or modernising their kitchens, it means they have jobs, they have savings and, most importantly, they have confidence in their financial situation. The 2.3% year-on-year increase in the average receipt value (to $92.76) suggests that customers are not shying away from larger purchases, even though the number of transactions fell slightly by 0.9%. In other words: they are buying less frequently, but not cheaper — this is behaviour characteristic of a cautious, not a discouraged, consumer.

Pressure on the property market and mortgage interest rates remain a real burden. CEO Ted Decker openly admitted that the company is feeling the effects of consumer uncertainty and the barrier to housing affordability — which explains why the results were “in line with expectations” rather than spectacular. Comparable sales in the US rose by a mere 0.4%, well below the estimated 0.88%. This is the only blemish on the picture. The property market remains frozen by high interest rates — owners are not selling because they do not want to lose the low interest rates from before 2022, which means that property turnover is low, and with it, demand for renovation is falling.

Nevertheless, taken as a whole, Home Depot’s results paint a picture of an economy that refuses to give in. The company generates over $6 billion in operating cash flow in a single quarter, maintains a gross margin of 33%, pays out $2.32 billion in dividends and plans to open 15 new stores this year.

In short:

KEY FINANCIAL FIGURES FOR THE FIRST QUARTER OF 2026

🔹 Revenue: $41.77 billion (forecast: $41.51 billion) 🟢; +4.8% y/y

🔹 Adjusted earnings per share: $3.43 (forecast: $3.41) 🟢

🔹 Like-for-like sales: +0.6% (forecast +0.9%) 🔴

🔹 US same-store sales: +0.4%

🔹 Net profit: $3.3 billion

Forecast for the 2026 financial year:

🔹 Like-for-like sales growth: from the base level to +2.0% (forecast +1.55%) 🟡

🔹 Sales growth: from +2.5% to +4.5%, confirmed

🔹 Adjusted EPS growth: from base level to +4.0%, confirmed

🔹 New stores: ~15

🔹 Adjusted operating margin: 12.8%–13.0%

Comment:

🔸 “The results for the first quarter were in line with our expectations.”

🔸 “Underlying demand in our sector was broadly similar to that seen throughout the 2025 financial year, despite greater consumer uncertainty and pressures relating to housing availability.”

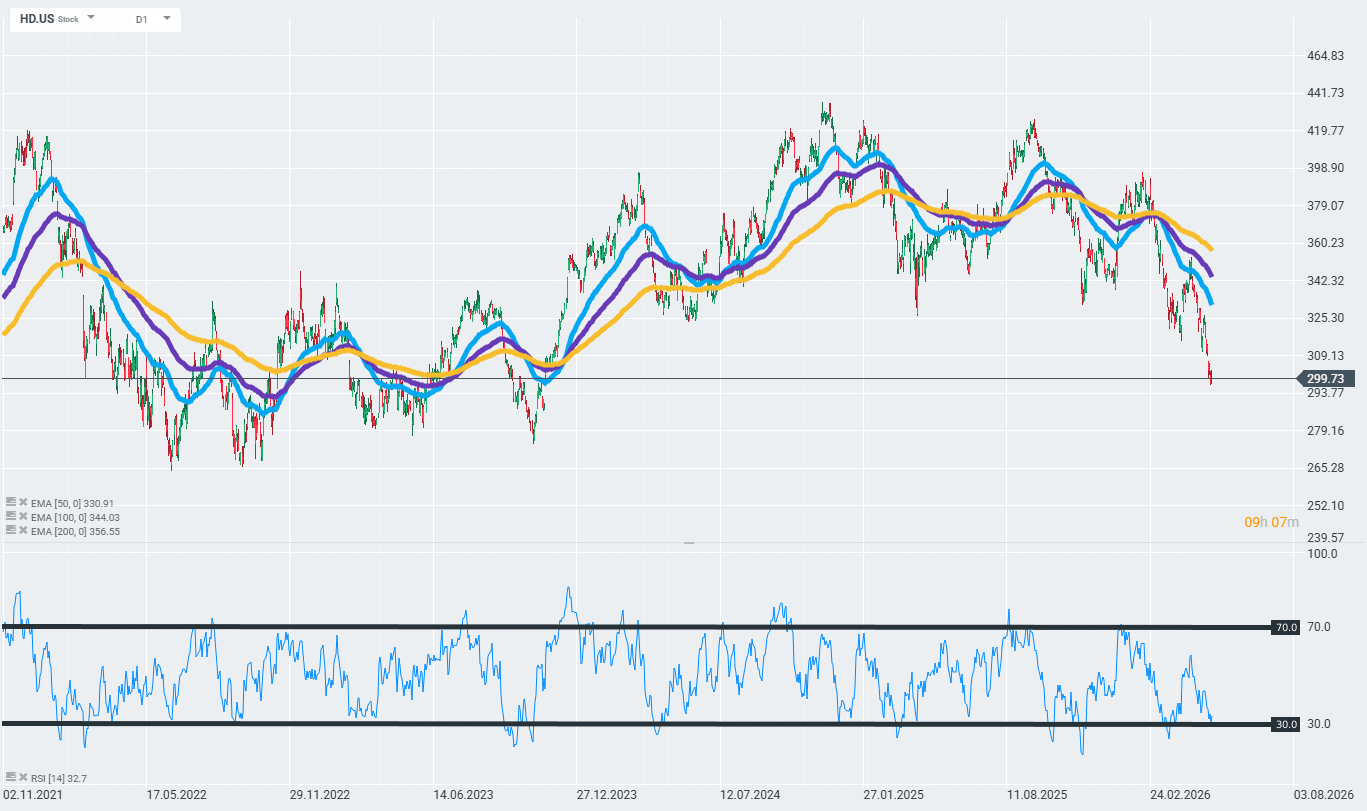

The company’s shares are trading flat in pre-market trading. The initial slight gains have been erased for the time being, and HD shares are now trading around 0.75% below yesterday’s close.

Home Depot is testing a strong support level at around $299–$300. The RSI(14), currently at 32.7, is approaching oversold territory (below 30), although the price remains well below all three EMAs (50/100/200). Source: xStation

US OPEN: The market extends losses as investor concerns grow

Market Wrap: European indices decline amid US - Iran tensions📉 Semiconductors under pressure

Netflix disappoints Wall Street 🚩 Stock drops 9% after disappointing outlook

Morninga Wrap: Wall Street Under Pressure. AI Loses Momentum, Netflix Disappoints, and the Persian Gulf Erupts

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.