Today's European session has been characterized by stabilization. Major indices are posting modest gains, but without any signs of euphoria. Investors are attempting to recover from the earlier deterioration in sentiment on Wall Street and from rising geopolitical tensions surrounding the Middle East and the Strait of Hormuz.

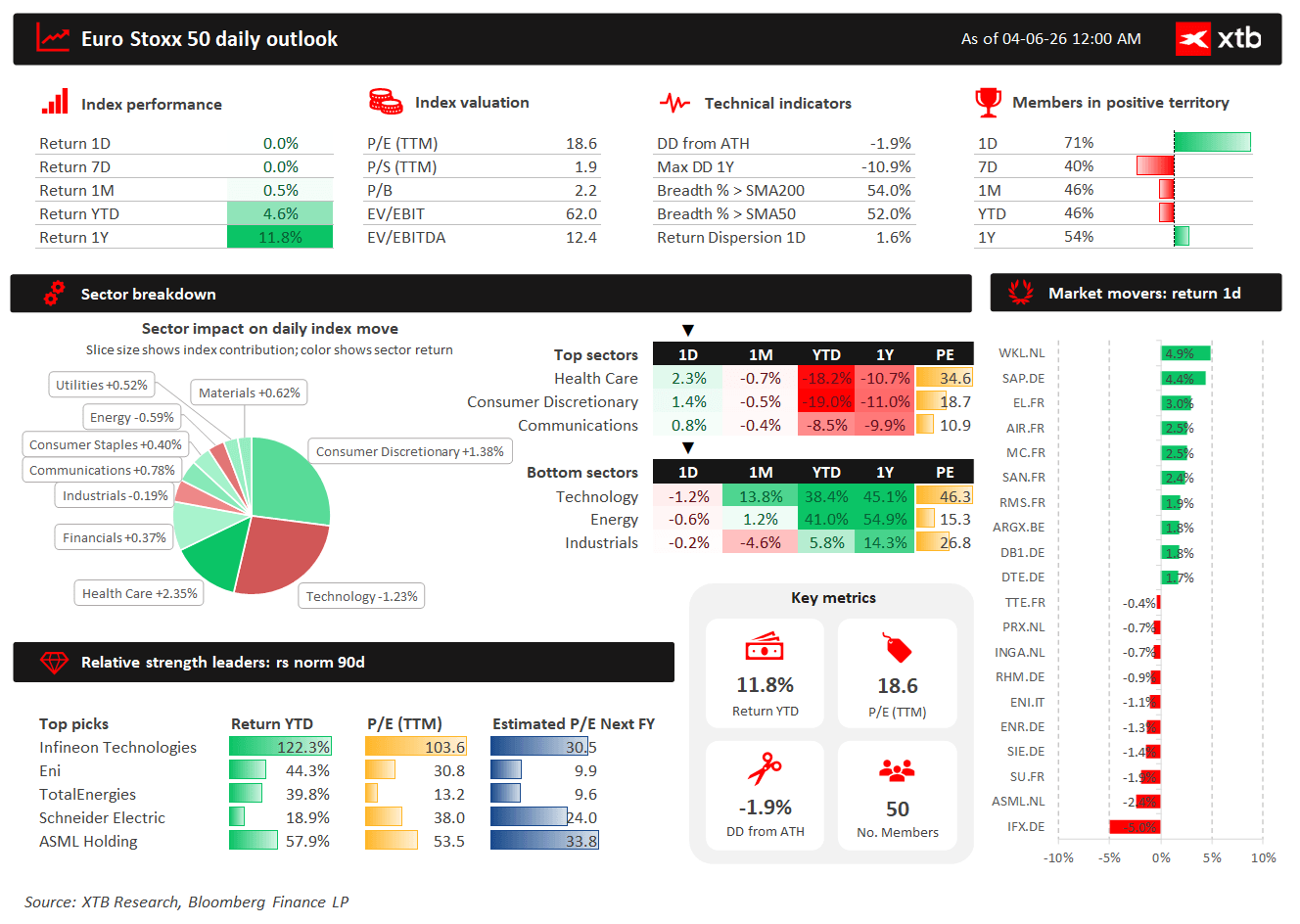

The key takeaway from the Euro Stoxx 50 is that the index itself remains essentially flat, but market breadth looks encouraging — as many as 71% of constituents are trading higher. The main challenge, however, has been weakness among several large technology stocks, particularly Infineon and ASML, which weighed on the broader index.

Major European Indices

- STOXX 600 gains around 0.2%, indicating a moderate improvement in risk appetite across Europe.

- DAX is up 0.9%. The German market continues to be weighed down by weak construction-sector data.

- FRA40 gains 1.3%, supported by stronger performance from luxury, consumer, and retail-related stocks.

- UK100 has recovered its initial losses and is now trading slightly higher, supported by banks and real estate-related companies.

EU50: Index Near Flat, but Most Stocks Are Rising

- Euro Stoxx 50 is up 0.5% on the day, with the majority of components remaining in positive territory.

- 71% of constituents are advancing, suggesting that buying activity has been fairly broad-based.

- However, the broader market picture remains weaker over longer timeframes, with the proportion of stocks in positive territory standing at approximately 40% over 7 days, 46% over 1 month, and 46% year-to-date.

- The index remains only about 1.9% below its all-time high.

- Valuations remain moderately elevated, with TTM P/E: 18.6; P/S: 1.9; P/B: 2.2; EV/EBITDA: 12.4

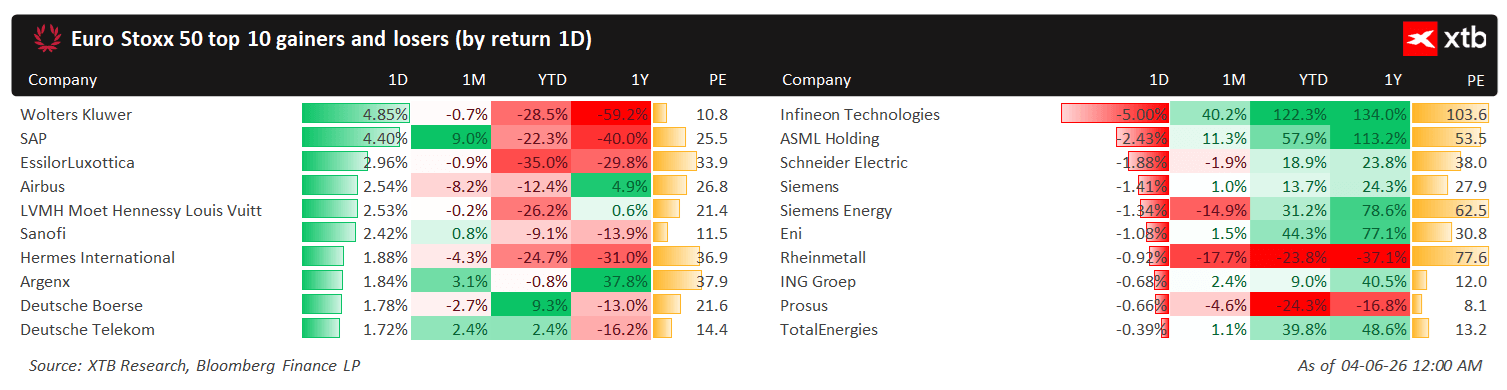

- Health Care (+2.3%) was the strongest sector in the Euro Stoxx 50 and made the largest positive contribution to the index's daily performance. Within healthcare, notable gainers included Sanofi +2.42%, EssilorLuxottica +2.96%, argenx +1.84%, Bayer +1.35%

- Technology (-1.2%) was the largest drag on the index despite a strong performance from SAP. Weakness in technology was concentrated in semiconductors: Infineon -5.0%, ASML -2.4%.

Top Performers in the Euro Stoxx 50

- Wolters Kluwer +4.85% — the strongest stock in the index, benefiting from demand for defensive quality and stable business models.

- SAP +4.40% — a very strong session for German software, partially offsetting weakness elsewhere in European technology.

- EssilorLuxottica +2.96% — strong performance from the consumer-healthcare segment, supporting the French market.

- Airbus +2.54% — a positive contribution from industrials, despite mixed performance across the broader sector.

- LVMH +2.53% — a rebound in luxury goods that also supported the CAC 40.

- Sanofi +2.42% — a strong day for healthcare, the best-performing sector within the Euro Stoxx 50.

- Hermès +1.88% — another luxury name attracting strong demand.

- Deutsche Börse +1.78% and Deutsche Telekom +1.72% also contributed positively to market breadth.

Geopolitics and Oil

- The main factor supporting sentiment was news of a conditional ceasefire between Israel and Lebanon.

- Markets interpreted this as a partial reduction in regional escalation risks, particularly after earlier concerns regarding shipping security through the Strait of Hormuz.

- Brent crude prices fell toward the $92–95 per barrel range, although they remain elevated compared with levels seen before the escalation.

Macro: weak retail sales

- Eurozone retail sales declined by 0.4% month-over-month in April, slightly weaker than the consensus expectation of a 0.3% decline.

- However, March data were revised sharply higher, which helped soften the negative implications of the April reading.

- On an annual basis, retail sales increased 1.0% year-over-year, significantly above market expectations of 0.3%, providing a more encouraging signal for consumer demand across the euro area.

US Open: weaker labor market and AI weigh on Wall Street ❗

US100 runs out of steam above the 30,000 level? 📌

Broadcom beats forecasts, yet shares fall nearly 13% ⚔️

Bitcoin falls 3%, extending the sell-off 📉 Double bottom in sight?

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.