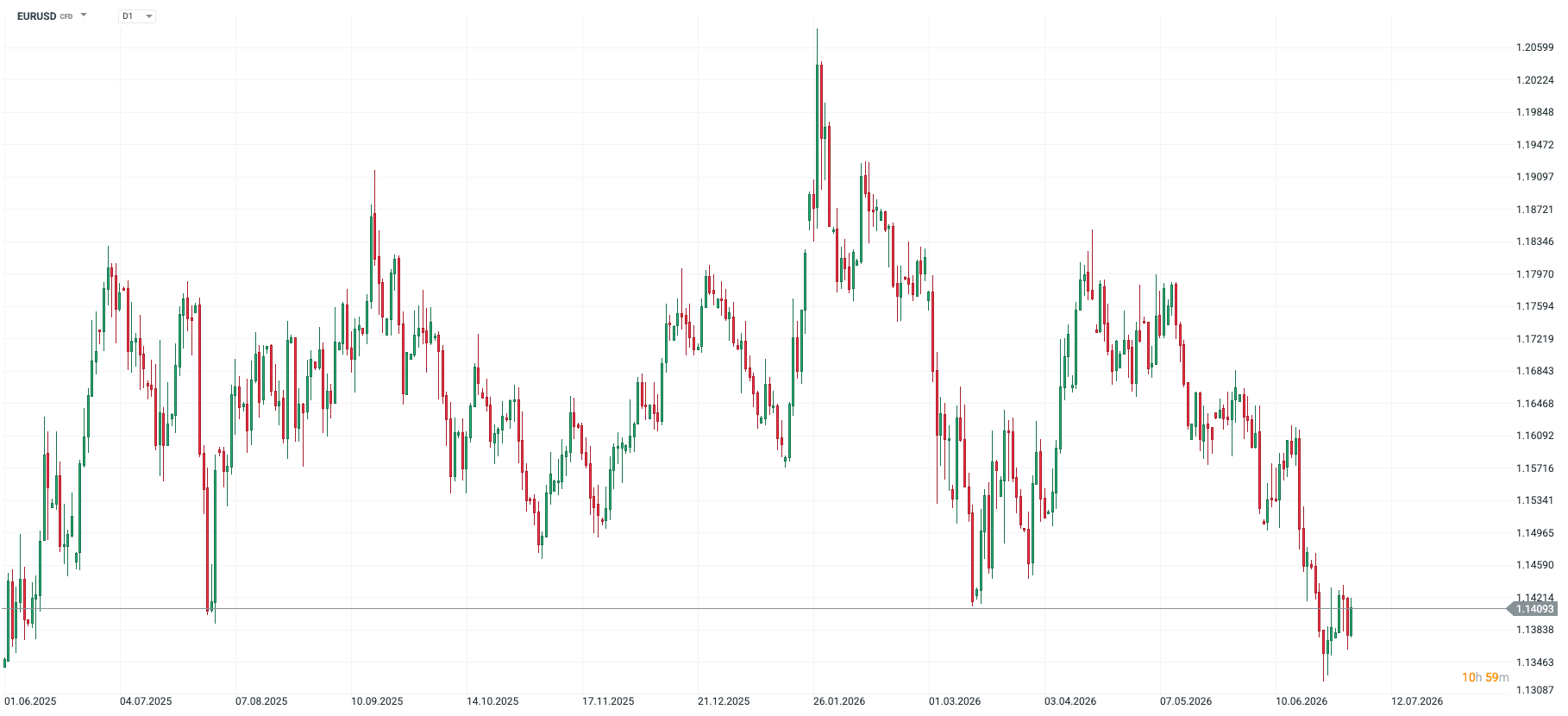

The recent FOMC meeting stirred significant emotions. The hawkish Dot Plot, the committee members' interest rate projection, led to a considerable strengthening of the dollar. Consequently, the EURUSD pair fell to its lowest level in over a year.

Figure 1: EURUSD (2025 - 2026)

Source: xStation, 02.07.2026

Source: xStation, 02.07.2026

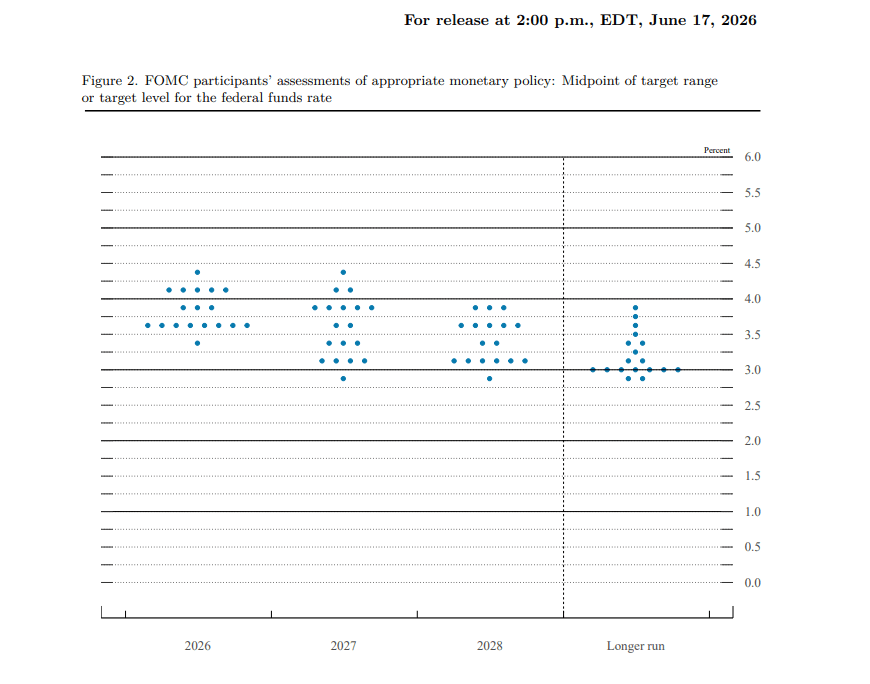

Half of the policymakers indicated a rate hike before the end of the year, expressing concern about the inflationary situation and placing faith in the strength of the labour market. Today's NFP data release, scheduled for 1:30 PM, will be a significant test for this narrative.

Figure 2: FOMC Dot Plot (2026 - 2028+)

Source: FOMC, 02.07.2026

Source: FOMC, 02.07.2026

What do we already know about the US labour market?

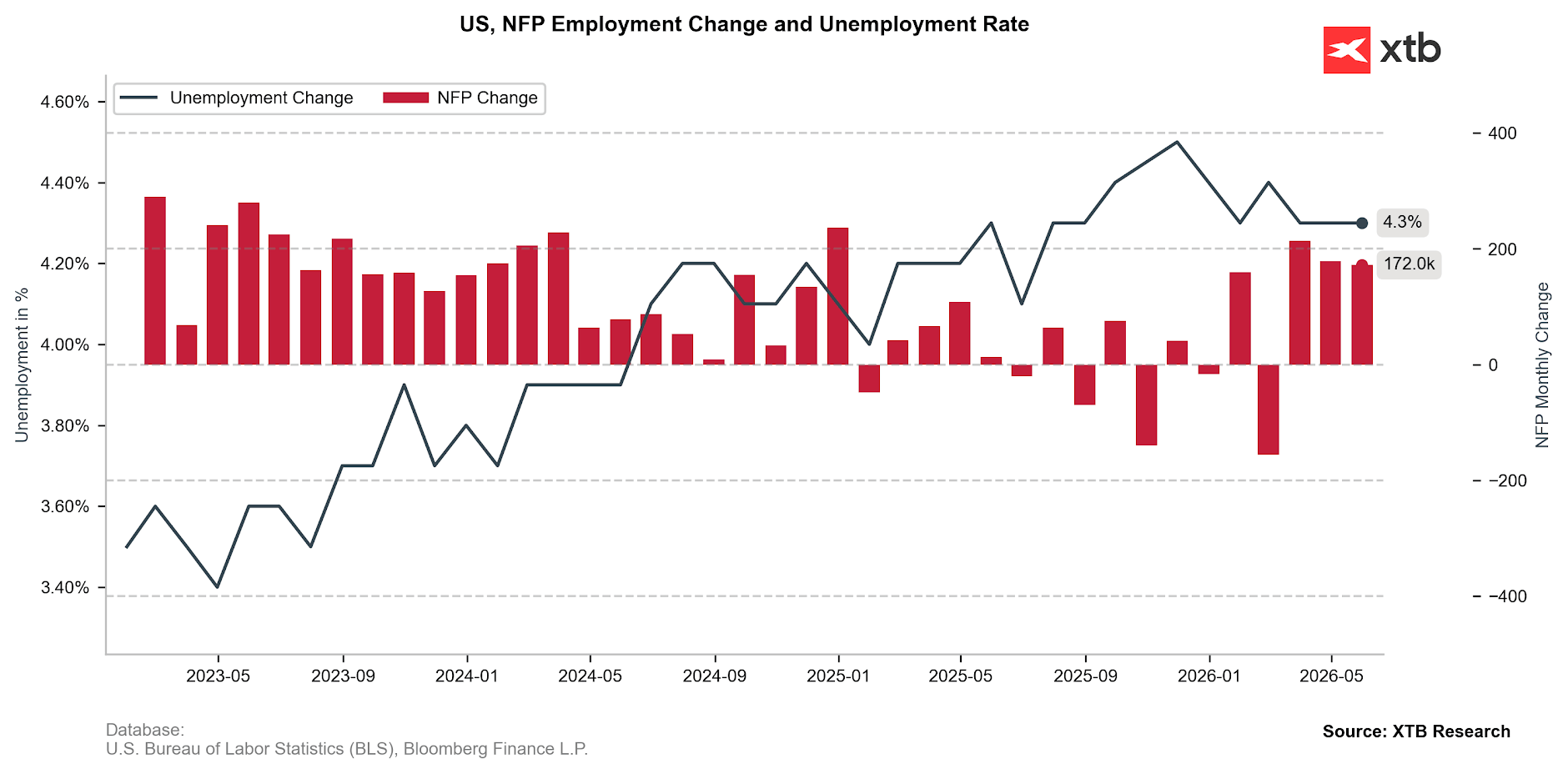

The latest NFP reading

In May, the number of jobs in the US labour market increased by 172k. This result was not just better than the consensus (86k), but significantly exceeds even the most optimistic forecasts (125k). Data for the two previous months (March and April) were also revised upwards. Since the Bureau of Labour Statistics has accustomed us to significant downward revisions, this was an exceptionally large surprise. At the same time, the unemployment rate remained unchanged (4.3%).

Figure 3: Change in Non-Farm Payrolls (NFP) and the US Unemployment Rate (2023 - 2026)

Source: XTB Research, 02.07.2026

Source: XTB Research, 02.07.2026

ADP

Although the data published yesterday was an unpleasant surprise for the markets, it still showed at least decent job creation (+98k).

- We see a significant disparity between the services sector (+96k) and the industrial sector.

- This was largely driven by the education and healthcare sector (+48k).

- Trade/logistics (+15k) and finance (+14k) also performed well.

- Weakness was observed once again in the leisure and hospitality industry (+2k), despite the World Cup taking place in the US.

- The situation in mining also does not look great (-5k).

Wage growth for those deciding to stay with their current employer reached 4.4%, and 6.6% for those changing jobs.

- Employees in the financial sector (5.1%) and industry (4.9%) could count on the highest raises.

- We saw a significant disparity between micro-enterprises employing fewer than 20 people (+2.9%) and companies with 50 or more employees contracted (+4.7%-4.8%).

The pace of job creation is slowing, but it is consistent with the "soft landing" narrative. In many sectors, finding employment takes longer than previously (the average unemployment duration has extended to 26 weeks), but this is not a comprehensive picture. In key industries, employers still encounter problems finding the right hands to work.

JOLTS

The JOLTS data, it is worth noting at the start, is delayed by one month relative to other readings. Therefore, it does not present as current a picture of the situation currently prevailing in the American economy. Especially in a period of such dynamic changes on the geopolitical front and the volatility of key energy commodity prices.

Nevertheless, the data for May does not give us major reasons for concern.

- The number of new vacancies grew at a pace similar to April's (and at that time we recorded a very significant improvement, which was perceived by many as temporary).

- The number of job quits remained at a low, albeit stable, level (3.1m). Only 1.9% of employees decided to voluntarily resign from their current position, which indicates a certain mistrust regarding the possibility of quickly finding a new vacancy.

- However, layoffs also remain at a low level – 1.7m, or 1.1%.

- The ratio of unemployed people actively looking for work to new vacancies remains around 1, which also does not raise major concern.

The data shows a picture of a stable labour market with little employee turnover. A clear reluctance to take the risk of resigning from the current position is visible. At the same time, however, employers are not inclined to mass layoffs.

Weekly jobless claims

The jobless claims data published last week also provide proof of this. These fell to 215k, remaining close to multi-year lows.

- The 4-week moving average also remains at a low level (224k).

- Continued claims (1.8m) remain below several-year averages but show a clear upward trend.

PMI Indicators

ISM: The sub-component for employment (49.7) still indicates a cut in vacancies in the industrial sector. And this is despite the increase in production and new orders, which may indicate cost-cutting in the face of rising expenses. However, the reduction in employment is clearly slowing down, and the trend is positive.

S&P: The picture outlined by S&P data looks much less positive. The data indicates the strongest reduction in vacancies since May 2020, i.e., the peak of pandemic lockdowns. Crucial in this respect is the increase in the prices of production components and raw materials.

What will investors pay attention to today?

Apart from the main reading, which will show the change in the number of people employed in non-farm sectors (consensus: 113k), we will look towards:

- Revision of data for the last two months.

- Unemployment rate (consensus: 4.3%).

- Wage growth, both annually and monthly (consensus: 3.5%; 0.3%).

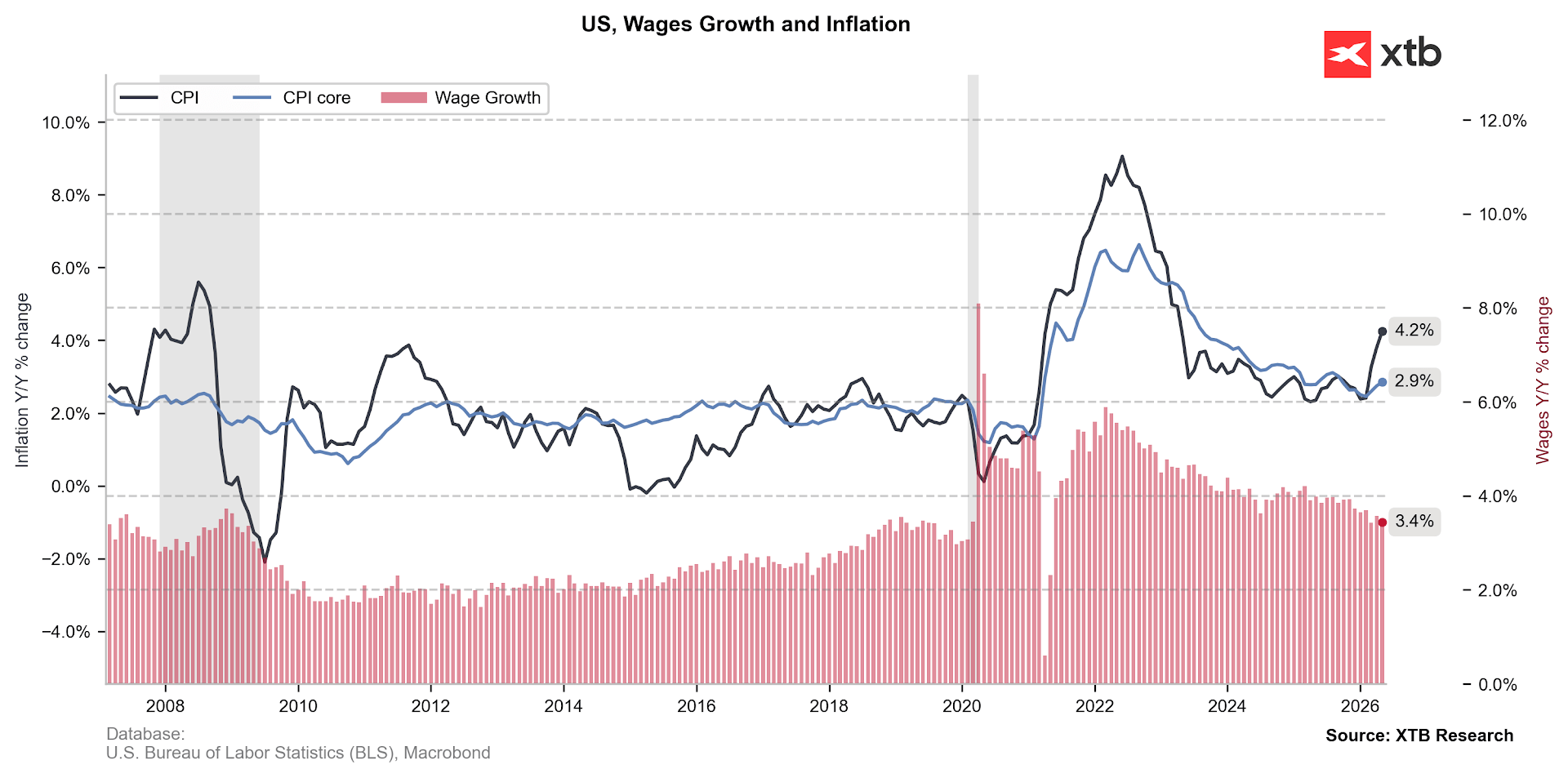

In the face of rising inflationary concerns (inflation at 4.2% and core measure reaching 2.9%), wage growth may draw particular attention. The consensus assumes a reading of 3.5%, which means a drop in earnings in real terms.

Figure 4: CPI inflation and wage growth in the US (2007 - 2026)

Source: XTB Research, 02.07.2026

Source: XTB Research, 02.07.2026

Lower-than-expected data would increase concerns about the American consumer, which are already quite strongly outlined at this moment. Consumption is largely taking place at the expense of savings (the savings rate has fallen to just 3%), and its growth is very uneven. The increase in consumption among the quintile (20%) of the highest earners in the US after accounting for inflation reached 3.8% in Q1. In the remaining part (80% of citizens), it essentially stood still (+0.6%).

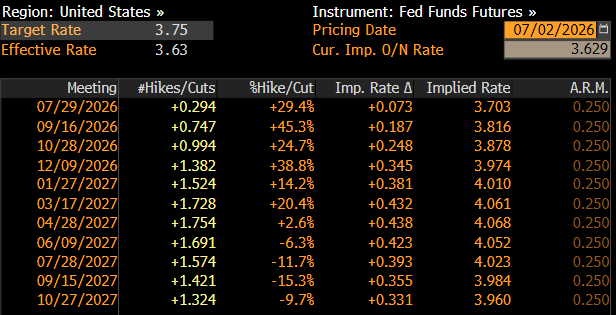

On the other hand, a strong increase in employment may confirm the hawkish FOMC axis in the conviction about the need for interest rate hikes. Maintaining the "low fire-low hire" state should allow policymakers to focus their attention fully on the inflationary pressure, which remains uncomfortably high.

Figure 5: Market-implied interest rate path in the United States (2026 - 2027)

Source: Bloomberg, 02.07.2026

Source: Bloomberg, 02.07.2026

—

Michał Jóźwiak, Financial Markets Analyst at XTB

Daily summary: Gold surges 2%, Nasdaq drags down sentiments on Wall Street

US100 falls almost 2% 🚩 Semiconductor stocks plunge as SanDisk tumbles 13%

NFP triggers a dollar sell-off – key takeaways from the June report

US Open: Nasdaq surges amid semiconductor rebound 🔼 Tesla shares down despite strong deliveries report

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.