-

The data showed significantly lower-than-expected job creation (+49,000).

-

The unemployment rate fell (4.2%), but at the expense of lower labour force participation (61.5%).

-

Wage growth increased (3.5%), but came out negative in real terms (-0.7%) for the second month straight.

-

The World Cup is not providing the expected boost to growth – the largest fall in new jobs was recorded in leisure-related sectors.

-

The report brings a revision to the market’s implied path for Fed interest rates.

-

The dollar is weakening by 0.6% against the euro today.

-

The data showed significantly lower-than-expected job creation (+49,000).

-

The unemployment rate fell (4.2%), but at the expense of lower labour force participation (61.5%).

-

Wage growth increased (3.5%), but came out negative in real terms (-0.7%) for the second month straight.

-

The World Cup is not providing the expected boost to growth – the largest fall in new jobs was recorded in leisure-related sectors.

-

The report brings a revision to the market’s implied path for Fed interest rates.

-

The dollar is weakening by 0.6% against the euro today.

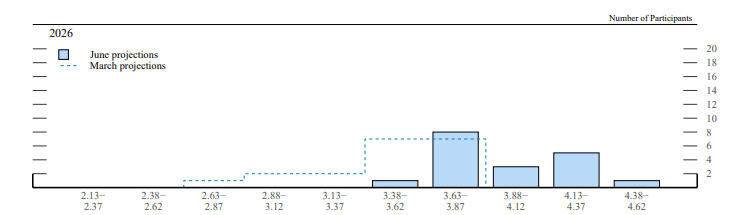

A little over a fortnight ago, robust US economic data and mounting inflationary concerns prompted FOMC policymakers to significantly revise the projections contained within the Dot Plot. Market expectations regarding interest rate hikes rose instantly, and the consensus shifted towards two upward moves before the end of the year. This led to a significant strengthening of the dollar, which reached its highest level against the euro in over a year.

Figure 1: Change in the FOMC Dot Plot [June vs March] (2026)

Source: FOMC, 02.07.2026

Today's reading significantly alters the narrative, especially as expectations for the June report were set high, influenced by, amongst others, statements from Treasury Secretary Scott Bessent.

Job creation slows

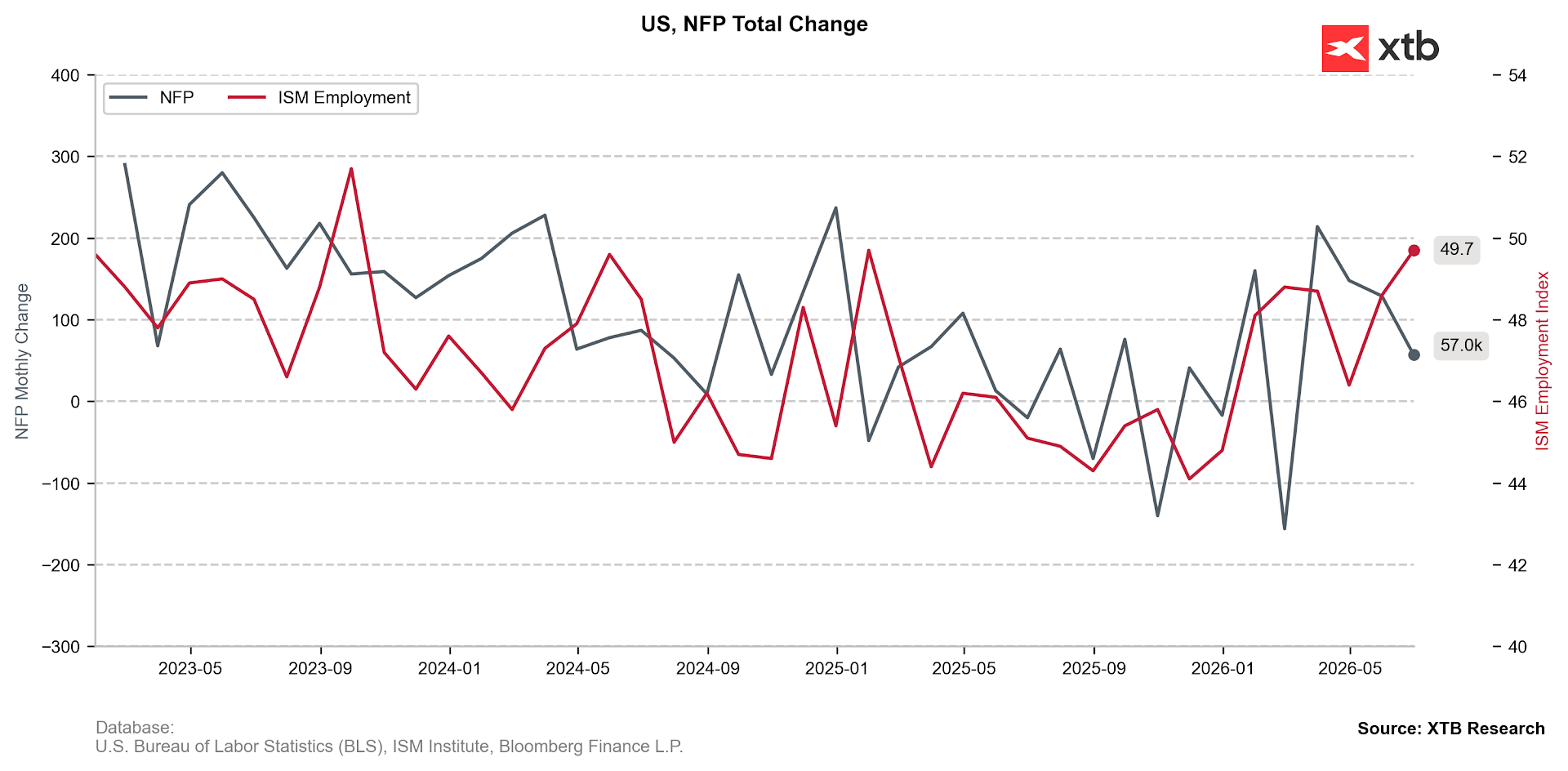

Data revealed significantly lower-than-expected job creation (+49k vs +107k) alongside a substantial downward revision of figures for the preceding two months (-74k). It is worth noting, however, that the three-month average remains at a healthy level (+111k) due to strong readings from April and May, suggesting that the June decline is not necessarily a harbinger of a cooling US labour market.

Figure 2: Change in Non-Farm Payrolls (NFP) and the ISM PMI Employment Sub-Component (2023 - 2026)

Source: XTB Research, 02.07.2026

Source: XTB Research, 02.07.2026

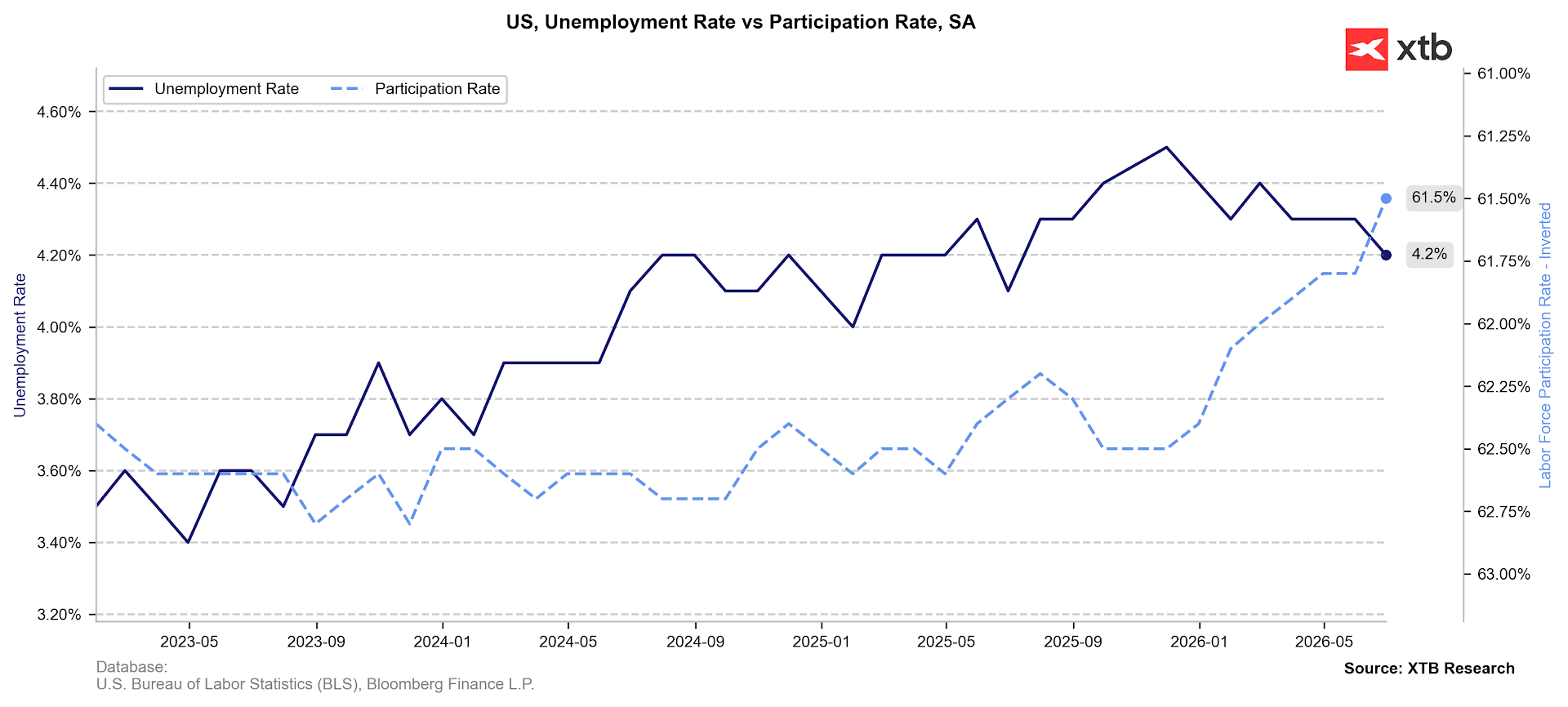

Unemployment rate falls at the expense of labour force participation

The unemployment rate fell to 4.2%, which would be a cause for optimism were it not for the significant decline in the labour force participation rate (61.5%). It was last at such low levels during the pandemic period.

Figure 3: US Unemployment Rate and Labour Force Participation Rate (2023 - 2026)

Source: XTB Research, 02.07.2026

Source: XTB Research, 02.07.2026

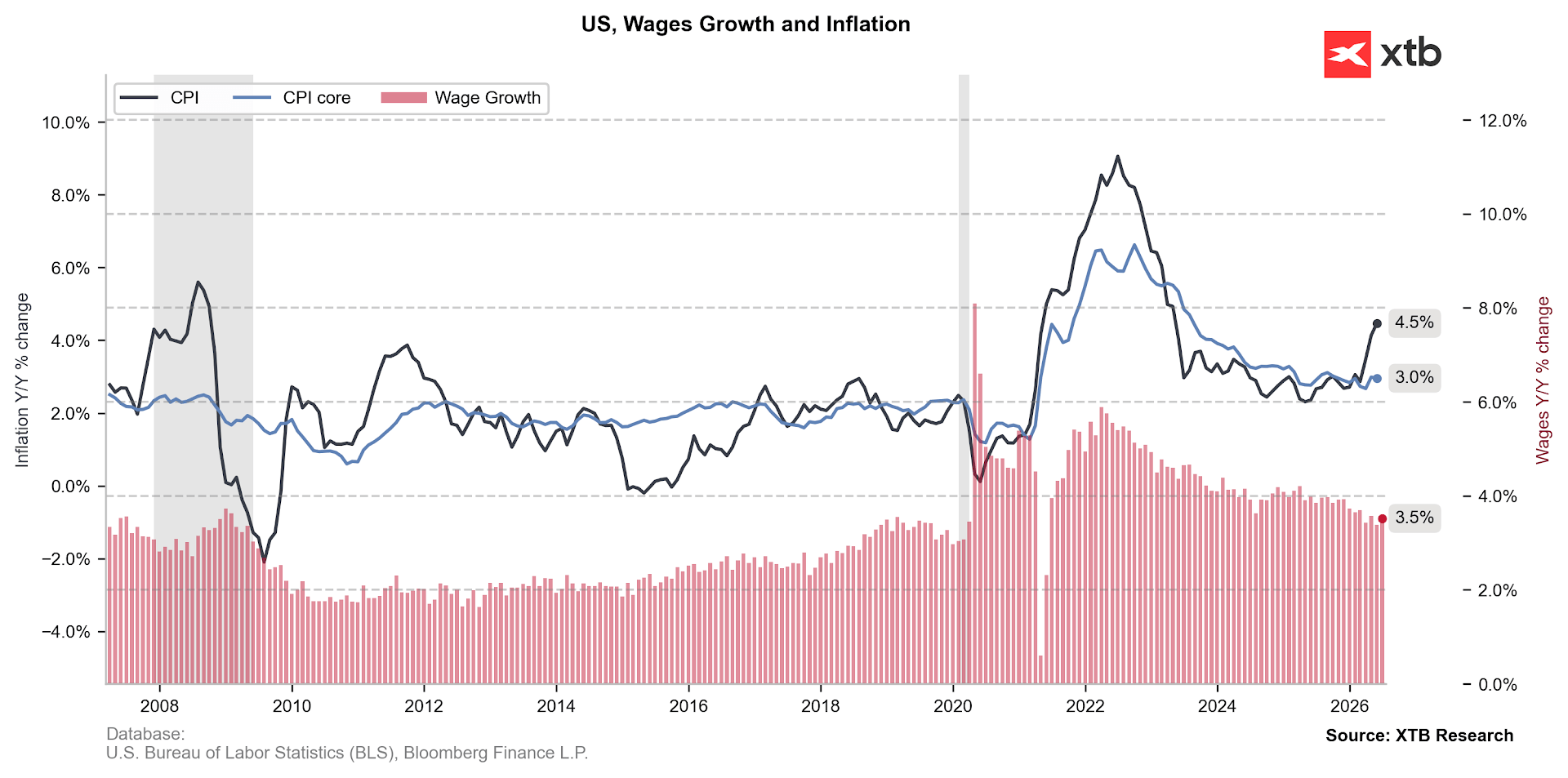

Wage growth will not drive consumption

Wage growth (3.5%) did not surprise, yet it turned negative in real terms (-0.7%) after adjusting for inflation. This is significant as US consumption is currently largely sustained at the expense of savings (the savings rate has plummeted to a mere 3%). We are also observing a vast disparity between the top income quintile (20%), where Q1 inflation-adjusted consumption growth reached 3.8%, and the remaining 80% of citizens, where real-term consumption was essentially stagnant (+0.6%).

Figure 4: US CPI Inflation and Wage Growth (2006 - 2026)

Source: XTB Research, 02.07.2026

Source: XTB Research, 02.07.2026

This implies that although inflation remains elevated (4.2% nominal, 2.9% core), the factors that could sustain it at such levels in the future are becoming increasingly scarce. The threat of significant second-round effects appears low, and the prices of key energy commodities have fallen by over 35% from their May peaks.

Furthermore, the trimmed mean remains at low levels (2.4%), a measure that the new Fed Chair, Kevin Warsh, has previously presented as a valuable alternative to the core PCE measure, which he famously characterised as "scientific tea-leaf reading". During his inaugural press conference, he mentioned repeatedly that the committee utilises "obsolete data" and that he remains open to alternative sources.

Labour market remains in a "low fire-low hire" state

The number of layoffs is declining (3.28 million), but the number of individuals voluntarily opting to leave their current employment is also trending downwards (0.78 million). This is consistent with recent ADP and JOLTS readings. The latter showed a very low volume of layoffs in May (1.7 million, or 1.1% of all employed) and a modest number of quits (3.1 million, or 1.9% of all employed).

This is no cause for panic, though it may be a source of muted concern. The growing apprehension amongst employees regarding the ability to swiftly find a vacancy with a new employer is not without merit. The average duration of unemployment is lengthening, currently standing at approximately 26 weeks. The number of people who have been unemployed for 27 weeks or more (currently 1.94 million) has also been rising in recent months.

The World Cup fails to provide the expected growth stimulus?

June was marked by the commencement of the FIFA World Cup, hosted this year across the US, Mexico, and Canada. Despite this, the largest drop in new job numbers was recorded within the leisure sectors (down by as much as 61k). It is difficult to attribute this to a high base, as total vacancy growth in the April-May period was only 33k following data revisions. Whilst it is too early for definitive conclusions, the year's biggest sporting event currently appears to be falling short of providing the expected economic stimulus (which was already projected to be modest, at around 0.1 pp of additional GDP growth).

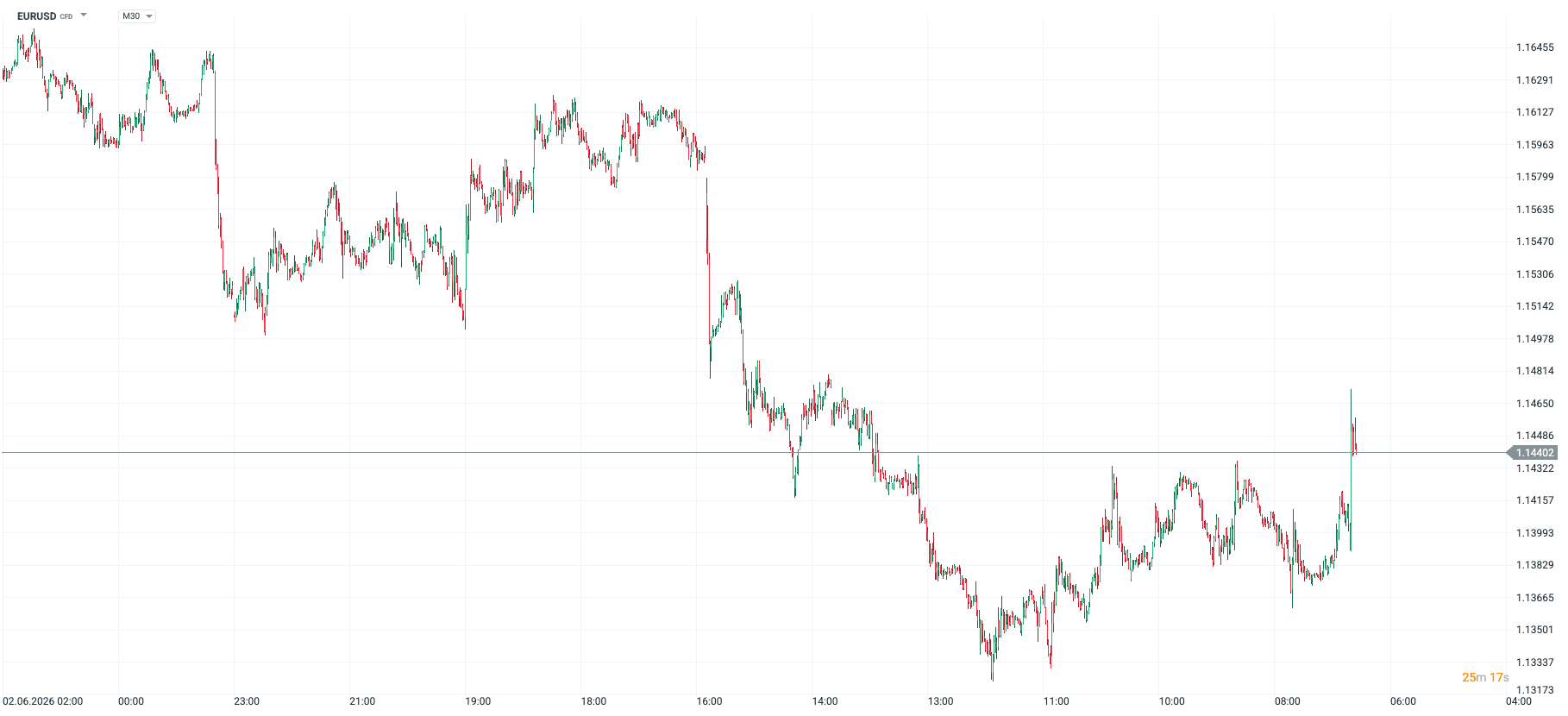

Impact of data on the FX market

The report brings a correction to the market-implied path of Fed interest rates. Investors still fully price in a hike before the end of the year, but they are attributing diminishing odds to such a move occurring at either of the next two meetings. This naturally weighs on the dollar, which is weakening against the euro by 0.6% today.

Figure 5: EURUSD [M30] (02.06.2026 - 02.07.2026)

Source: xStation, 02.07.2026

Source: xStation, 02.07.2026

The EURUSD pair is oscillating around 1.145, awaiting further data and statements that may indicate the Federal Reserve's course of action in the coming months. In the background, the issue of negotiations between the US and Iran remains. A breakdown in these talks would lead to a renewed pivot towards risk-off sentiment, providing support for the dollar.

—

Michał Jóźwiak, Financial Markets Analyst at XTB

Daily summary: Gold surges 2%, Nasdaq drags down sentiments on Wall Street

🟡Gold Regains Luster Thanks to Weak NFP

BREAKING: US NFP report lower than expected 🚩 US100 reacts

NFP: A Key Moment for the Dollar

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.