- Rheinmetall shares came under heavy pressure after Germany withdrew from the F126 frigate programme and opted for smaller TKMS vessels.

- The market reaction was sharp. The stock lost as much as 20% in a single session, extending the persistent downtrend of recent months.

- Losing this project does not fundamentally change the company’s long term revenue and profit trajectory.

- Rheinmetall shares fell sharply after Berlin’s decision on the F126 programme

- Rheinmetall remains one of the key pillars of Europe’s defence industry

- Rheinmetall shares came under heavy pressure after Germany withdrew from the F126 frigate programme and opted for smaller TKMS vessels.

- The market reaction was sharp. The stock lost as much as 20% in a single session, extending the persistent downtrend of recent months.

- Losing this project does not fundamentally change the company’s long term revenue and profit trajectory.

- Rheinmetall shares fell sharply after Berlin’s decision on the F126 programme

- Rheinmetall remains one of the key pillars of Europe’s defence industry

The market is pricing in not only the lost contract, but also the risk that Europe’s defence commitments will be less durable than previously assumed. That interpretation may be too pessimistic

At first glance, Rheinmetall’s decline looks like a classic reaction to losing a major order. Germany cancelled the six ship F126 frigate programme, and over time the federal government changed course and decided on smaller vessels: the Meko A 200 from TKMS.

For Rheinmetall, this is a meaningful blow, because after acquiring NVL the company had ambitions to capture a share of the naval operations market. The contract mattered for those ambitions, but it was not the core of the investment thesis for Rheinmetall.

The market did not punish the company solely for the loss of revenue from a single project. Rheinmetall was expected to gain around EUR 2 billion from frigate construction over the next three years, which is only a few percent of the revenue projected for the coming years. It is also worth noting that the project was cancelled before the company signed contracts or recognised any revenue related to it.

A decline that reached around 20% during the session wiped out value far greater than the realistic profit Rheinmetall could have generated from this contract, or even from a series of similar orders.

This is not entirely irrational. Rheinmetall was one of the biggest stock market winners of the war in Ukraine and Europe’s strategic shift. After extremely strong valuation gains, market expectations grew to sky high levels, and tolerance for disappointment fell to zero.

The company is not free of risks, including:

- Margin pressure

- Order execution issues

- Capital expenditure

- The geopolitical premium (or the lack of it)

All of these are real risks to earnings and valuation. That suggests investors have begun to price in a broader issue: the risk that Europe’s political declarations on rearmament will not always translate into rapid multi billion euro orders.

Even taking into account the full set of risks, threats and pressures facing the company, one can start asking whether the correction has not already gone too far.

Solid fundamentals and fragile valuations

Rheinmetall is not a company whose fundamentals justify a 50% drop in six months.

In 2025, the group increased sales by 29% to EUR 9.9 billion, and operating profit rose by 33% to EUR 1.84 billion.

The operating margin climbed to 18.5%, and the order backlog reached a record level. For 2026, management still expects sales growth to EUR 14.0 to 14.5 billion and an operating margin close to 19%.

Q1 2026 did not meet market expectations on the revenue line.

Sales increased, but came in below consensus, which for a stock previously priced with a significant premium had to trigger a reaction.

However, operating profit and margin still improved year on year, and the company explained the weaker start to the year as delivery shifts rather than cancellations, while also signalling an acceleration in the following quarters, in line with a pattern the company repeats almost every year.

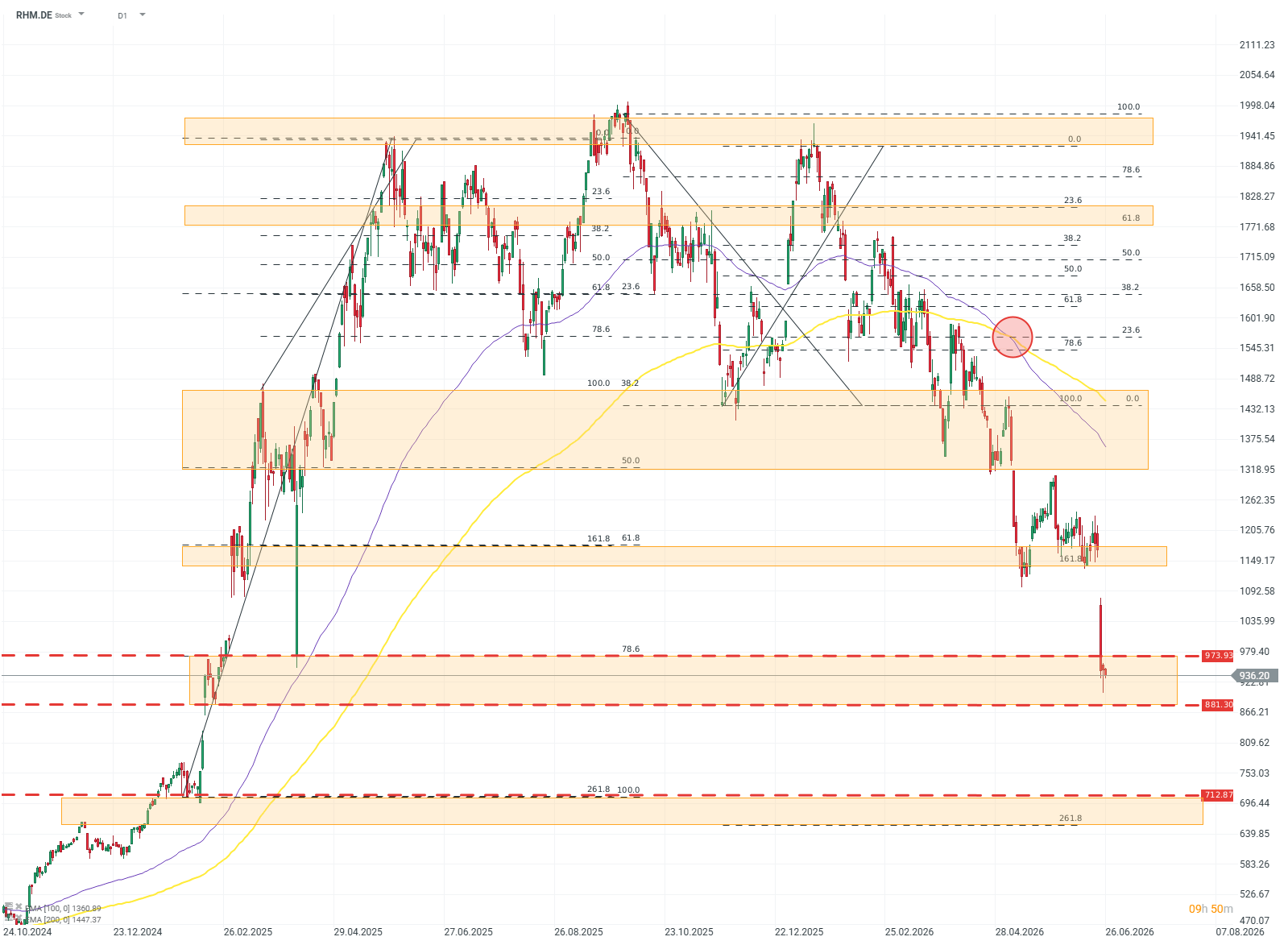

RHM.DE D1

The company’s technical picture is far more ambiguous than its fundamentals. Despite double digit growth in revenue and earnings, the stock has lost almost all of its 2024 to 2025 gains over the past six months. Valuations may be weighed down by a strong bearish signal known as the death cross, the crossover of the EMA100 and EMA200, which indicates strong downside momentum. If the broad support zone between 970 and 880 fails, the next meaningful level is not until around EUR 600. Source: xStation5

Is Europe pulling out of the arms race?

The biggest mistake in the negative interpretation of recent events is the assumption that cancelling F126 signals weakening European determination on defence. Reality is different. Germany’s armed forces are doing something uncharacteristic: abandoning an expensive, delayed and increasingly less rational project in favour of smaller, faster and more efficient programmes.

The gap between the market’s interpretation and political reality is fundamental. European defence budgets are rising despite fiscal pressure, high debt costs and political tensions. That shows the relentless determination of almost the entire continent to change the status quo.

EU member state defence spending is already an order of magnitude higher than before Russia’s full scale invasion of Ukraine in 2022. The share of funds earmarked for purchasing brand new equipment is also increasing.

The F126 decision may therefore signal not the end of the rearmament cycle, but its maturation. Europe will spend more, but it will not necessarily accept every cost and every delay.

For Rheinmetall, this is more of a signal and context, but not a risk. Why?

A weak link or a pillar of Europe’s defence industry?

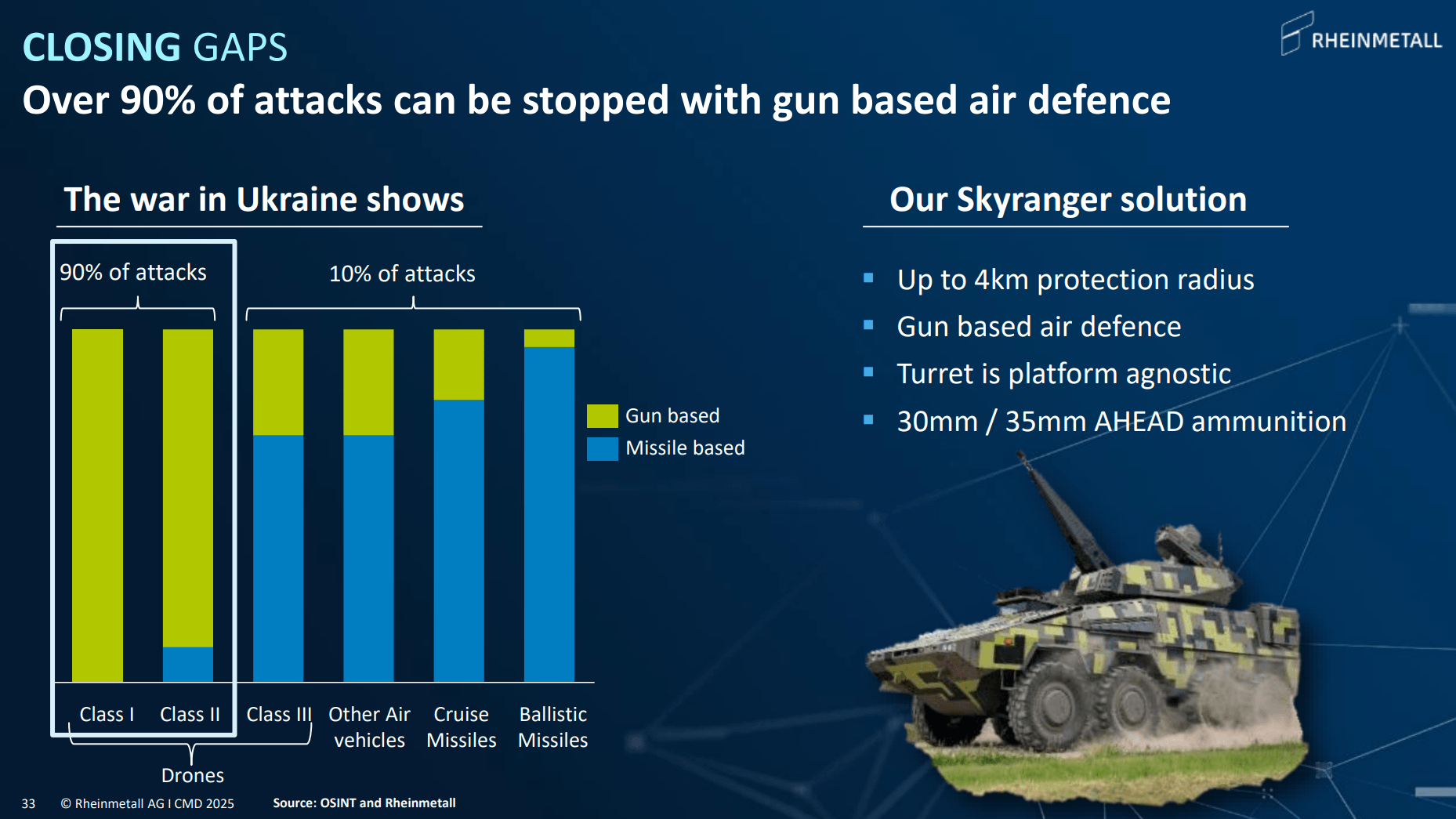

Rheinmetall’s strongest position is not in the frigate programme, but in segments that address the most urgent needs of European armies: ammunition, infantry fighting vehicles, land systems, and air defence, especially short range.

This last area is becoming increasingly important given the growing presence of drones on the battlefield.

Source: Rheinmetall

Skyranger and Skynex systems are filling a gap Europe must close quickly: countering drones and cruise missiles.

Rheinmetall’s advantage here comes not only from technology, but also from industrial capacity. It is important to remember Rheinmetall is not a small company. Despite what may seem like a modest market capitalisation by today’s standards, it currently produces more artillery ammunition than the entire United States. In weapons markets, beyond quality and price, delivery timelines and production capacity matter. On that front, Rheinmetall is among the top players not only in Europe, but globally.

Summary

Rheinmetall lost more than a potential contract. The market lost confidence in the people and organisations in Europe that determine the pace and scale of rearmament. However, given recent price action and sentiment across the defence sector in recent months, the market is clearly looking for threats where there are none.

Positive sentiment isn't limited to stock market analysts valuing the company. Despite the deepening declines, board members continue to make private share purchases. Yesterday (June 25, 2026), the company's CEO purchased another stake, this time for €3 million.

Even using conservative free cash flow valuations for the coming years, Rheinmetall appears very cheaply valued today. The current valuation does not reflect the position of a leader in Europe’s defence industry, but instead already prices in every conceivable risk for the company and then some.

Kamil Szczepański

Financial Markets Analysts, XTB

Daily Summary- Wall Street Holds Firm While Commodities Plunge on Hawkish Fed

Super El Niño Strikes: How to Secure Your Portfolio and Profit from Global Climate Changes?

Daily Summary: Time for a Correction (23.05.2026)

Morning Wrap - De-escalation in Hormuz, SpaceX drop fuels Big Tech decline (23.06.2026)

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.