Target Hospitality is a niche company that provides accommodation for workers in remote parts of the United States. So far, the company’s business has been based mainly on building and operating temporary housing facilities for, among others, the extractive and construction industries.

The company has just held an interesting earnings call.

- Revenue fell again, to USD 72.8 million, representing a roughly 20% quarter-over-quarter decline.

- EPS looks even worse: the company has reported losses for five consecutive quarters. The loss in Q1 2026 came in worse than expected, reaching -USD 0.13 versus the expected level of around -USD 0.10.

- Adjusted EBITDA looked better, coming in at USD 9.94 million versus expectations of USD 8.5 million. However, given the rest of the data, it is fair to ask to what extent the strong adjusted EBITDA reflects operational efficiency rather than, for example, accounting effects.

After the results, the stock is up as much as 14% - it likely would not have risen that much while showing a widening loss. Investor optimism stems from a massive contract the company reportedly won, expected to bring in USD 750 million over the “next few years.”

This contract allowed the company to raise profitability forecasts by more than a dozen percent as early as year-end 2026.

Management increased its year-end revenue target to USD 375 million (vs. USD 325 million) and its EBITDA target to approximately USD 80 million (versus prior estimates of around USD 73 million).

This is not the first such contract recently. In April, the company announced another contract worth USD 550 million. The first question that arises in light of this information is: who is paying hundreds of millions of dollars for modular housing containers and mobile toilets?

Of course, both contracts relate to supporting the construction and operation of AI data centers, and the company emphasizes the strategic nature of this shift and its reorientation toward that segment. From the company’s perspective, it’s a home run: it keeps its existing business model unchanged—only the customer changes, to one whose enormous CAPEX budgets can support higher margins. From an investor’s perspective, however, it may be worth asking how durable such growth and margin improvement really are.

This leads to a second question. It is important to add context: Target Hospitality reached its peak in revenue and profitability in 2023 and has been on a downward trajectory since then. From this perspective, the company’s rebound looks like a temporary attempt to latch onto a broader market trend that has stopped asking hard questions about the durability of solutions, the rationality of growth, or the cost of investment.

Some investment firms also appear optimistic, raising their price targets on the stock.

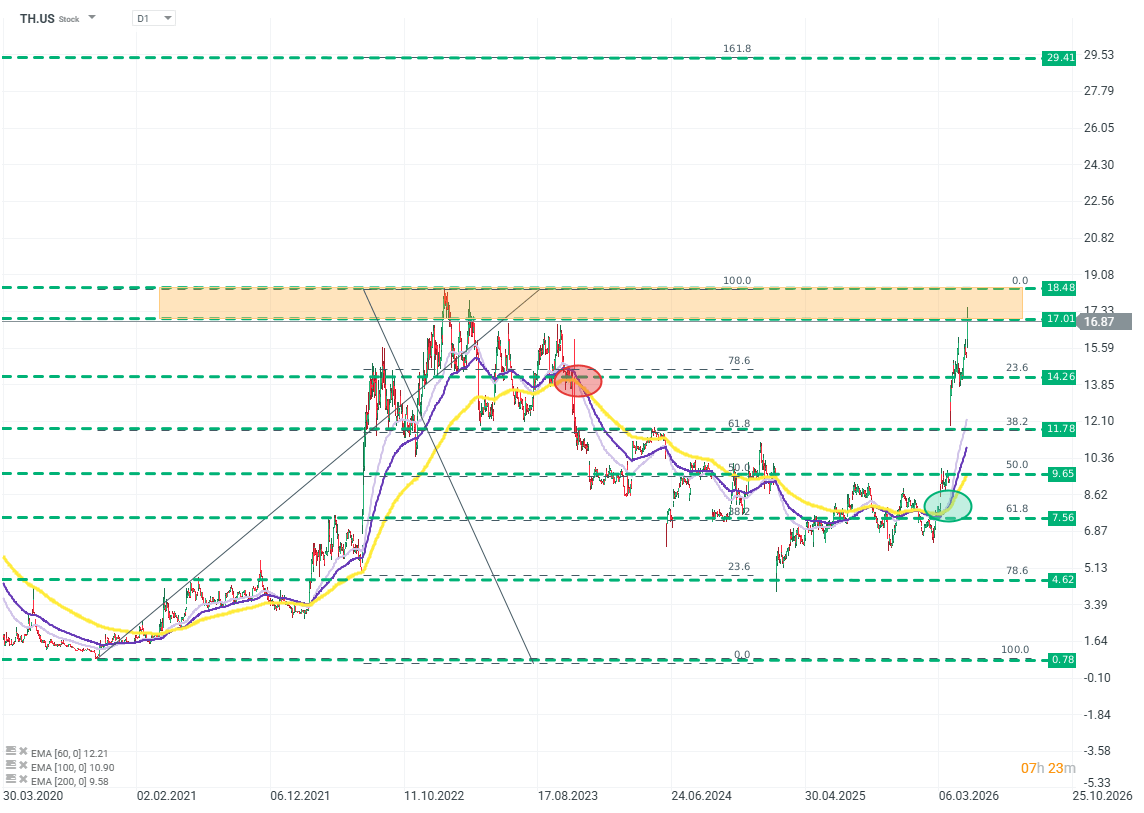

TH.US (D1)

The price increase reacts much more quickly, discounting future benefits from new contracts. The company has risen ~130% in the last three months, reversing over two years of losses. This reflects the broader market sentiment toward entities associated with the "AI boom." Source: xStation5

OpenAI heads into a price war ahead of an IPO?

US OPEN: A recovery after declines, Trump threatens to resume fighting with Iran

Daily Summary- Return of the Sell-off on Wall Street⬇️

🔴US100 drops nearly 4%

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.