The US stock market has opened slightly lower today, but has recovered since The S&P 500 is up 0.2%, whilst the NASDAQ Composite sees gains of 0.6%. The sentiment has not changed all to massively after the resurgence of inflation fears – today’s PPI inflation reading came in well above expectations. Nvidia is starting the day with a significant gain (2.8%), as its CEO, Jensen Huang, flew with Donald Trump to visit Xi Jinping.

The US President is now in Beijing and will meet with the General Secretary of the Communist Party of China at 3:15 AM UK time. This is by far the most eagerly awaited event of the week. Attention will be focused both on headlines regarding the future of trade relations between the two countries and on any updates on the US-Iran conflict. Although in the short term the closure of the Strait of Hormuz does not pose a major problem for Xi, given the high level of strategic reserves, in the longer term it may prove problematic, as over 55% of China’s oil imports come from the Middle East.

Meanwhile, the representatives of the investment bank Morgan Stanley have shown their optimism about the broader market outlook, raising their price forecasts for the S&P index for the end of 2026.

Macroeconomic data

The Bureau of Labour Statistics has published data on producer price inflation, which surprised the market by coming in significantly higher than the consensus forecast. The headline measure rose by 6% year-on-year – the sharpest increase since December 2022 and well above expectations (4.9%). Perhaps even more significantly, we are seeing substantial increases in the core measure and the so-called “super-core” index, which excludes not only energy and food prices but also trade-related services. The largest increases are, unsurprisingly, seen in the aviation sector – airfares soared by 3% compared to March and by 15% year-on-year.

At 3:30 PM, the data on oil and petrol inventories, relevant within the context of the current market situation, were also published. The decline proved to be more severe than expected (-4.3 million barrels).

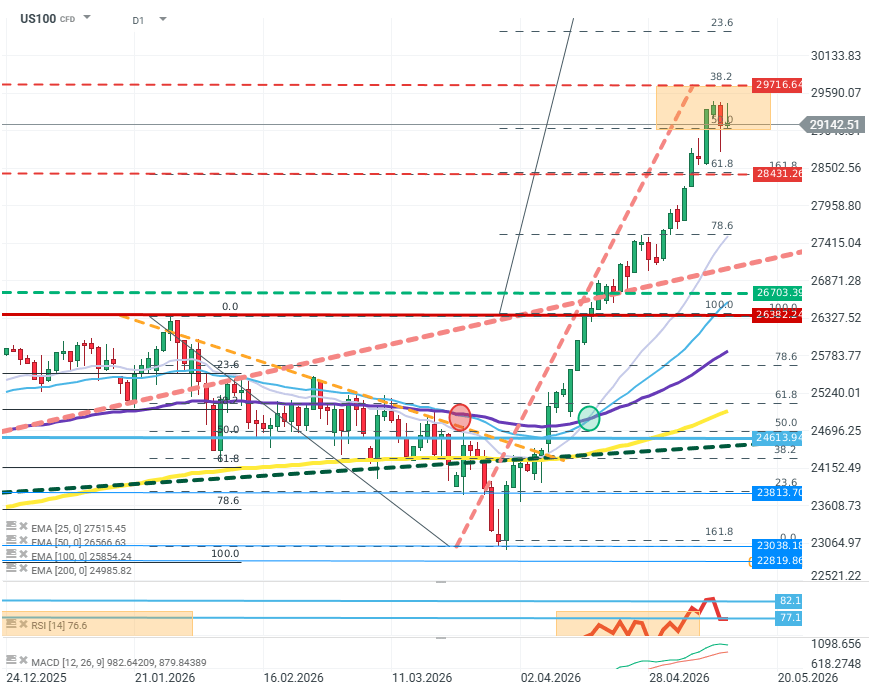

US100 (D1)

Source: xStation, 13.05.2026

Source: xStation, 13.05.2026

The uptrend has maintained its gains around the 29,200-point mark, above the 161.8 FIBO level calculated based on the January-March correction. The EMA momentum remains strongly bullish, but buyer momentum appears to be waning. The potential for a correction is supported primarily by the RSI (14) indicator, which has been signalling overbought levels for several weeks now.

Company news

- Ford (F.US): One of the giants of the US automotive industry has published its results for Q1 2026, surprising investors with a very significant increase in profitability. The company’s EPS rose to $0.66, compared with expectations of less than $0.20. The company’s management has also raised its EBIT forecast to $8.5–10.5 billion by the end of the year. The company’s shares are up by more than 5%.

- Alibaba (BABA.US): The Chinese e-commerce company, which is increasingly involved in AI as well, has published its results for Q1 2026. Despite disappointing revenue growth and profitability, which are under pressure from AI investments, positive sentiment and hopes surrounding the Xi-Trump meeting are supporting the share price, which is up by over 6%.

- Quantum Computing (QUBT.US): One of the leading companies in the quantum computing sector has published its results. Despite positive sentiment ahead of the release and strong revenue growth (partly due to the acquisition of Lumiar Semiconductors), investors are expressing concerns about the company’s ability to cut costs and improve its negative EPS. The share price has fallen by over 6%.

- Arteris (AIP.US): A leading provider of NoC (Network-on-Chip) solutions has risen by over 7% following the release of its Q1 2026 results. Revenue rose by nearly 40% year-on-year, enabling the company to raise its revenue forecast for 2026 to a range of $91–95 million. As much as two-thirds of new orders are currently associated with artificial intelligence chips.

—

Kamil Szczepański & Michał Jóźwiak

Financial Market Analysts at XTB

Daily summary: Wall Street climbs higher as oil falls 📈 SpaceX surges 28%

📈 SpaceX shares surge 20%

Oil slides 2.5% to $88 as Middle East tensions ease 📉 Is the uptrend over?

Wall Street Rebounds as Oil Prices Fall 📈 Adobe Shares Drop 8% After Earnings

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.