Investors on Wall Street are cautiously optimistic, reacting to a mix of weaker-than-expected economic data and renewed hopes for two interest rate cuts by the end of 2025. Big cap indices are trading in the green (S&P500: +0.18%, Nasdaq: +0.2%, DJIA: +0.2%), while small caps are underperforming due to discouraging outlooks from the latest ISM reports (Russell 2000: 0.13%).

Adding to the cautious sentiment, the ADP employment report showed a sharp slowdown in job creation. Only 37,000 new private-sector jobs were added in May—well below the expected 110,000 and nearly 50% lower than April’s figure. This signals weakening hiring activity amid uncertain economic growth.

Meanwhile, the ISM Services Index also pointed to a cooling economy. The index fell to 49.9 in May, below the expected 52, indicating contraction in the services sector. Price pressures continue to mount, largely due to the unsettling tariff expectations.

Together, these data points have increased market bets that the Federal Reserve may intervene with interest rate cuts to avoid a potential recession. This sentiment is echoed in bond markets, where the yield on the 10-year U.S. Treasury has fallen by 1.6%.

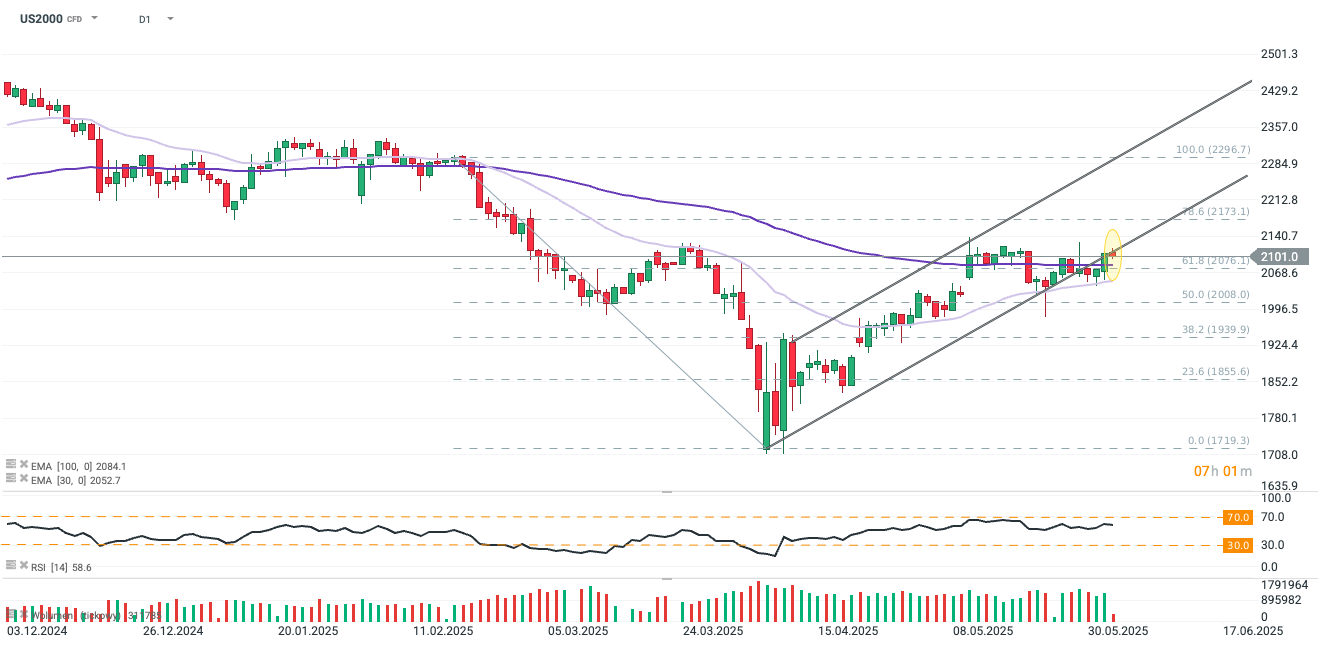

US2000 (D1)

Small-cap stocks are under pressure today, dragged down by disappointing ISM data. The Russell 2000 stands out as the only major index in the red, reflecting investor concerns over the economic outlook for smaller companies.

Despite a strong start to the day, the index failed to hold its gains and slipped back to the 2,100 level—a key resistance point previously tested in late March and mid-May. Ongoing producer price pressures and uncertainty surrounding tariffs are weighing heavily on smaller firms. These headwinds are now being reflected technically, with the exponential moving averages (EMAs) for the index showing signs of flattening—an indicator of weakening momentum.

Source: xStation5

Company news:

-

AnaptysBio shares are down 12% in spite of premarket gains fueled by the news that Phase 2b trial data showed its drug rosnilimab delivered JAK-like efficacy in moderate-to-severe rheumatoid arthritis. Patients achieved low disease activity, remission on the CDAI, and ACR70 responses over six months, with effects lasting two months off treatment.

-

Chart Industries (GTLS.US) and Flowserve (FLS.US) agreed to an all-stock merger valuing the combined company at ~$19B. Chart holders will get 3.165 Flowserve shares per share owned and hold 53.5% of the merged firm. The deal promises $300M in synergies and EPS accretion in year one, with closing expected in Q4. Nevertheless both stocks are currently losing around 4%.

-

Couchbase is up 4,3% despite issuing a rather cautious Q2 outlook despite strong Q1 results. Annual recurring revenue grew 21% to $252.1M, beating estimates, and driven by Capella cloud adoption and strategic wins. While Q1 revenue and earnings topped forecasts, guidance for Q2 revenue was soft, reflecting prudence amid macro uncertainty.

-

Guidewire (GWRE.US) shares surged 19% after raising full-year revenue guidance above estimates, driven by strong cloud migration execution, new deals, and cost management. Q3 revenue rose 22% YoY to $293.5M, with adjusted EPS beating at 88c vs. 46c expected. Analysts praised its growing market share among large carriers and raised price targets amid a robust sales pipeline.

-

Hewlett Packard Enterprise (HPE.US) shares rose 0.3% following Q2 results that topped expectations with broad-based strength. Revenue rose 5.9% to $7.63B, led by solid growth in Servers (+5.6%), Hybrid Cloud (+13%), and Intelligent Edge (+7%). The company raised the low end of its full-year EPS forecast and sees continued revenue growth of 7–9% in constant currency. Despite modest AI-related revenue and mixed guidance, analysts noted improved server execution and solid margin performance, with Q2 EPS beating consensus at $0.38 vs. $0.33 expected.

-

Snowflake (SNOW.US) shares are up 0.5% premarket after its Summit event showcased a robust AI-driven product roadmap, including advancements in core analytics, support for unstructured workloads, and accelerated AI capabilities. Analysts noted strong enterprise interest, streamlined go-to-market strategies, and hiring momentum as signs of durable growth. They were also positive on the entire data investment cycle.

Daily Summary - Powerful NFP report could delay Fed rate cuts

BREAKING: Massive increase in US oil reserves!

Palo Alto acquires CyberArk. A new leader in cybersecurity!

US OPEN: Blowout Payrolls Signal Slower Path for Rate Cuts?

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.