American chipmaker Advanced Micro Devices (AMD.US) warned investors of a revenue decline in Q3 2022 due to weaker PC market demand and worsening supply chain problems. The company lowered forecasts, with shares already down nearly 6% before the open:

- Q3 revenue will be roughly $5.6 billion vs. earlier forecasts of around $6.7 billion

- Revenue from the client market fell 40% year-over-year to about $1 billion

- AMD reported a non-GAAP gross margin of close to 50%, versus a previous expectation of 54%

- Gaming (14% y/y) and Data Center (45% y/y) revenues increased

- The acquisition of Xilinx earlier in the year proved to be a hit for AMD, generating $1.3 billion in revenue for the company

AMD during Q2 assumed a maximum of $200 million deviation in further revenue estimates, the difference of nearly 1 billion is also a surprise for the company, according to the company, there is currently a significant inventory correction taking place in the overall computer market. It is worth adding that even AMD's previous forecasts, which have not been 'proven', looked quite pessimistic, and their update affects the already weak sentiment of the semiconductor market. If AMD's quarterly sales come in at $5.6 billion, it will still represent almost 29% growth compared to Q3 2021, but will shake the quarterly revenue growth rate. The market has been expecting AMD to keep beating earnings forecasts and maintain a steady pace of growth through which the stock has particularly suffered recently due to its exorbitant P/E valuation.

- Stacy Rasgon, a semiconductor market analyst at Bernstein, warned investors of a deteriorating semiconductor market picture in which the stock prices of chipmakers Intel, TaiwanSemiconductors, AMD and Korea's Samsung are suffering.

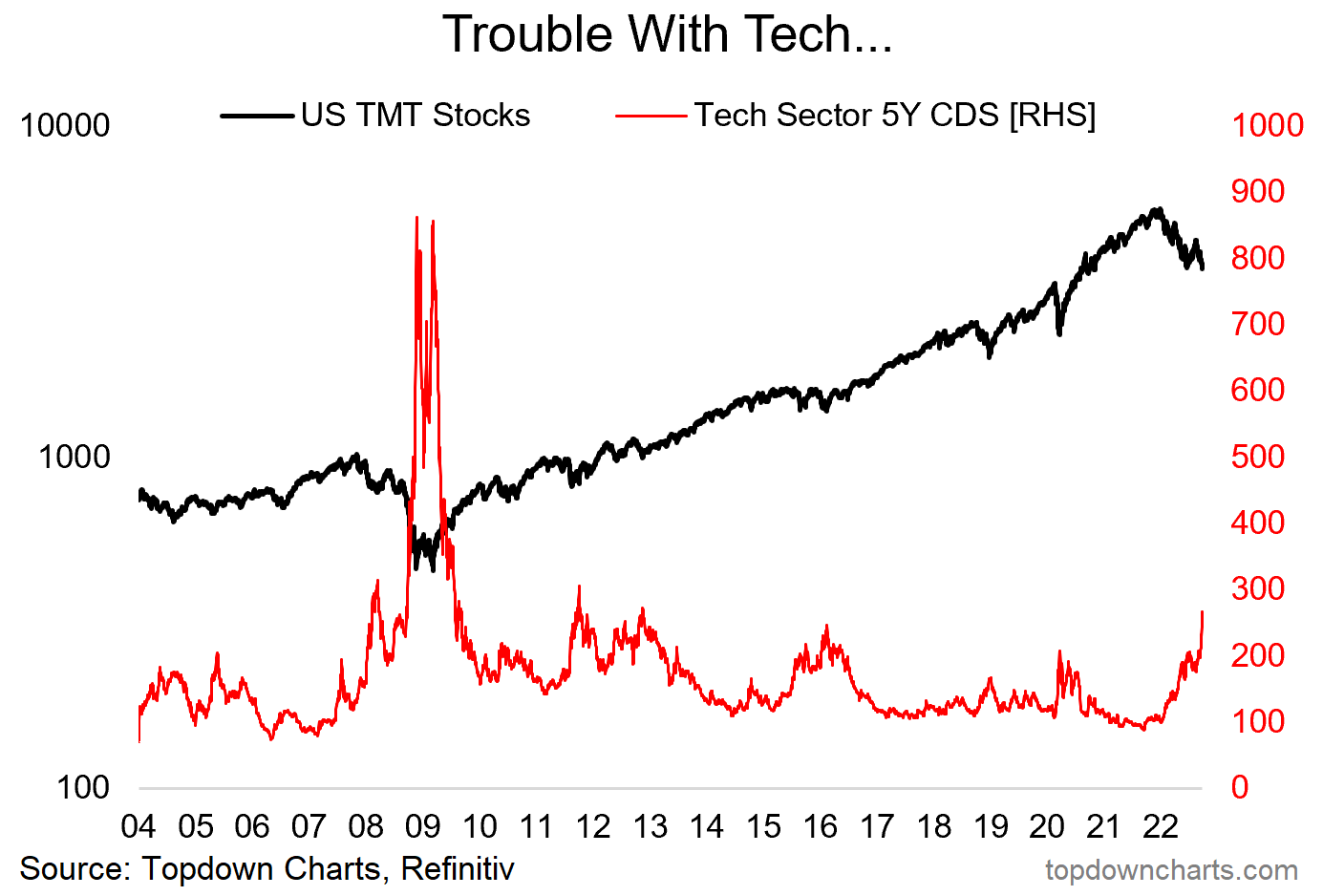

The chart shows an increase in 5-year CDS spreads (credit default swap) for tech companies, illustrating the priced-in increase in bond default risk and financial instability among US tech stocks. We saw a similarly rapid rise during the 2008 - 2009 financial crisis. Source: Refinitv, Topdowncharts

The chart shows an increase in 5-year CDS spreads (credit default swap) for tech companies, illustrating the priced-in increase in bond default risk and financial instability among US tech stocks. We saw a similarly rapid rise during the 2008 - 2009 financial crisis. Source: Refinitv, Topdowncharts

- In pre-opening trade, shares of Intel (INTC.US), Taiwan Semiconductors (TSMC.US) and Nvidia (NVDA.US) are falling, having already reported up to $400 million in quarterly losses due to U.S. sanctions on China's tech market that include a ban on technology exports and restrictive licensing. Dell (DELL.US) and HP (HPQ.US) are also losing stock.

- Samsung also lost, showing its first drop in quarterly earnings since 2019. The forecast cuts look worrisome in the context of the upcoming earnings season. The Korean giant's profit surprised analysts, falling 31.7% year-on-year amid inflation hitting demand for smartphones, home appliances and chips;

- The United States plans to move some semiconductor production from Taiwan to Phoenix, Arizona. The May 2020 Taiwan Semiconductors deal, initially valued at $12 billion, is now being widely discussed in the U.S., which has faced the logistical challenge of diversifying its critical technology supply chain and recreating domestic production;

- Increased recession risk, still-high inflation and a strong dollar are eroding technology sector margins and driving up financing costs; stocks of companies driven by debt and venture capital and private equity fund inflows may be particularly vulnerable during this period, likely to cut spending and reduce risk exposure.

Advanced Micro Devices (AMD.US) shares. The price of the stock has encountered strong resistance in the form of the 200-session SMA200 average running around $70, the opening near $64 indicates further downside potential although the stock market may be supported by a possible weaker NFP reading at 2:30 p.m. The company's fundamental valuation has cooled dramatically, with the P/E ratio settling around 19 points and P/B ratio reaching 2, making the valuation appear to be within the index average. The PEG Ratio (the stock's valuation relative to expected revenue growth rate and expected earnings per share) has cooled tremendously, at 0.67, which may encourage contrarian investors to take an interest in the company's stock. Source: xStation5

SAP eredmények: A felhőalapú szolgáltatások iránti kereslet erős, a haszonkulcsok továbbra is nyomás alatt vannak

Reggeli összefoglaló: Visszapattan-e a piac a csütörtöki eladási hullám után❓

US Open: Az Alphabet és a Tesla nyomást gyakorol a Wall Streetre, miközben az olajárak újra aggodalmat keltenek a befektetők körében

A Lockheed Martin és az RTX felfelé módosította az előrejelzését 🚀 A védelmi szektor részvényei emelkednek

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.