-

Record Highs and Supply Crunch: Copper has breached the $14,000/t mark driven by the Strait of Hormuz blockade—which disrupted sulphur supplies vital for refining—and significant production slumps in Chile.

-

AI and Defense as Structural Drivers: The exponential expansion of AI data centers and increased NATO defense spending (5% GDP targets) are creating a long-term copper deficit that current 10-20 year mining cycles cannot meet.

-

Inventory Paradox and Financialization: While US stockpiles appear high due to strategic reserves (Project Vault), physical exchange liquidity remains tight as investors increasingly trade copper as a high-growth "proxy" for the AI tech sector.

-

Record Highs and Supply Crunch: Copper has breached the $14,000/t mark driven by the Strait of Hormuz blockade—which disrupted sulphur supplies vital for refining—and significant production slumps in Chile.

-

AI and Defense as Structural Drivers: The exponential expansion of AI data centers and increased NATO defense spending (5% GDP targets) are creating a long-term copper deficit that current 10-20 year mining cycles cannot meet.

-

Inventory Paradox and Financialization: While US stockpiles appear high due to strategic reserves (Project Vault), physical exchange liquidity remains tight as investors increasingly trade copper as a high-growth "proxy" for the AI tech sector.

The current situation in the global copper market, as observed in May 2026, constitutes another example of the convergence of several major factors leading to the emergence of a powerful new upward impulse. Copper prices on the London market have exceeded the level of $14,000 per tonne. Although these are not yet the highest intra-day prices, for several days we have been recording the highest historical closes. Will geopolitical factors and long-term trends related to technological development be sufficient to maintain prices at such a high level? Are the current increases fundamentally justified, or do they result from short-term factors? What should be expected next from the copper market?

The Strait of Hormuz crisis and its non-obvious implications

The blockade of the Strait of Hormuz obviously affects the prices of energy commodities, such as oil and gas, which ultimately impacts transport costs. However, it must be remembered that the Persian Gulf countries are responsible not only for the production of energy commodities; primarily due to their access to cheap energy, they are important producers of goods that require high energy input or are derived from petroleum refining. One of the by-products of oil and gas refining is sulphur, which is a key factor in the production of sulphuric acid—essential in the production processes of refined copper. These processes include heap leaching, solvent extraction, and electrowinning (SX-EW). These processes account for as much as one-fifth of the entire world's refined copper production.

The transmission mechanism of the sulphur crisis to the copper market

The Persian Gulf region accounts for nearly 25% of the world's sulphur supply and approximately half of the seaborne trade in sulphuric acid. Consequently, countries that have so far been importers of sulphur or sulphuric acid currently face a significant problem with its availability, particularly in light of the export ban that has emerged in China.

-

Rise in sulphur prices: Sulphur prices on world markets have reached record levels, exceeding $1,200 per metric tonne, which is confirmed by the financial reports of giants such as the Mosaic Company.

-

Logistical paralysis: Due to the corrosive nature of sulphuric acid, its land transport as an alternative to the blocked sea routes in the Strait of Hormuz is impractical and economically unjustified on a large scale. Consequently, the use of alternative routes is nearly impossible.

-

China’s export restrictions: The situation was worsened by Beijing's introduction, as of May 1, 2026, of strict restrictions on the export of sulphuric acid, aimed at securing domestic phosphate fertilizer production and food security.

-

Impact on mining costs: Analyses indicate that every 10% increase in oil prices raises the direct costs of copper mining by approximately 3.5%. With oil prices sustained above $100 per barrel, the marginal cost of producing a new unit of copper has increased by approximately 16%. This is very significant information in the context of planning future mine investments, where the process from finding deposits to starting industrial mining can last from 10 to even 20 years, introducing enormous uncertainty regarding the profitability of such ventures.

Regional consequences of reagent shortages

The sulphuric acid crisis has hit key mining regions asymmetrically, leading to measurable losses in metal supply.

-

Chile: As the world's largest importer of sulphuric acid, Chile experienced a doubling of the price of this raw material in just seven weeks (to $380 per tonne). This resulted in a drop in copper production in the country by 6% in the first quarter of 2026. Metal production amounted to 1.21 million tonnes. Long-term plans in Chile—a key producing country—indicate a desire to increase annual mining to 5.54 million tonnes by 2034.

-

Democratic Republic of the Congo (DRC) and Zambia: In Africa, where 50-60% of production is based on sulphuric acid, sulphur prices reached astronomical levels of $1,000–$1,400 per tonne.

-

Global supply forecasts: The International Copper Study Group (ICSG) lowered its mining growth forecast for 2026 from 2.3% to 1.6%, pointing to disruptions in Chile, Indonesia, and the DRC.

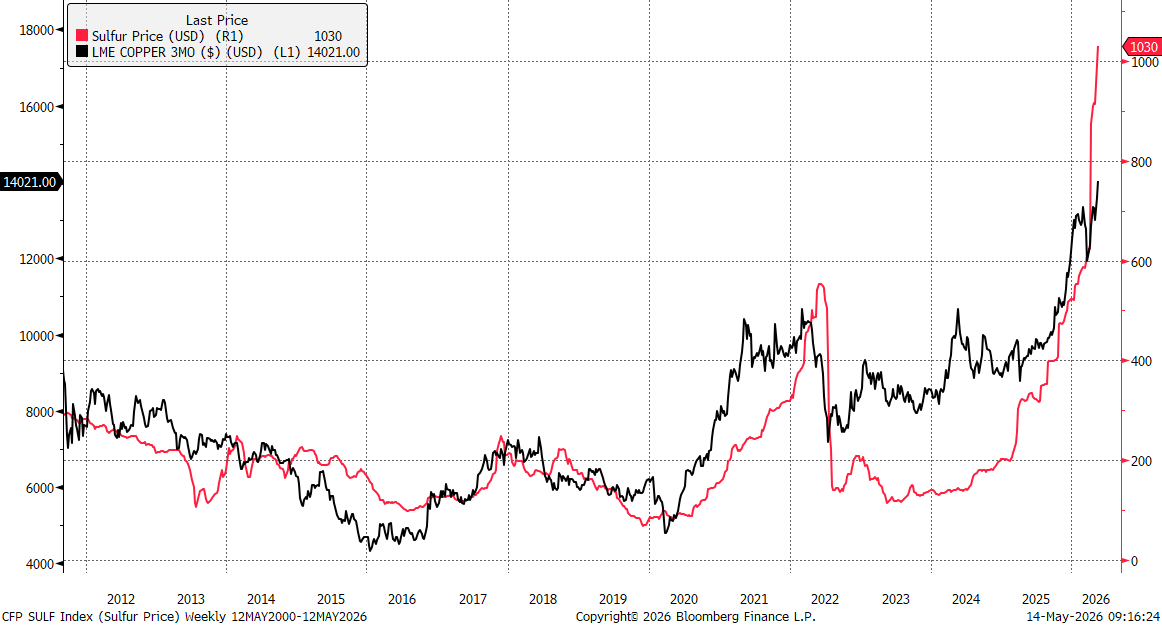

The price of copper reached $14,000 per tonne, while sulphur prices in China rose this year from around $500 per tonne to over $1,000 per tonne. It is worth noting that the price increase in 2022 also stimulated copper prices to set the then-peak above $10,000 per tonne. Source: Bloomberg Finance LP, XTB

The price of copper reached $14,000 per tonne, while sulphur prices in China rose this year from around $500 per tonne to over $1,000 per tonne. It is worth noting that the price increase in 2022 also stimulated copper prices to set the then-peak above $10,000 per tonne. Source: Bloomberg Finance LP, XTB

AI as a new foundation for structural demand

While supply problems build the basis for maintaining prices at high levels relative to history, the development of AI infrastructure has become a key driver of expectations regarding future copper prices. Although copper is still mainly used in the construction of infrastructure and up to 50% of demand is generated in China, the metal is beginning to change its character from a cyclical metal to a strategic metal for the entire technology sector.

Intensity of copper use in AI data centres

Analysis of modern hyperscale data centres indicates a sharp increase in copper demand compared to traditional IT facilities.

-

Unit consumption: It is estimated that for every megawatt (MW) of installed capacity in an AI data centre, there are between 27 and 33 tonnes of copper. In the case of the largest centres with a capacity of 100 MW, the demand can reach several thousand tonnes of metal per single facility.

-

Critical applications: Copper is irreplaceable in transformers, switchgear, emergency power systems, and in increasingly advanced liquid cooling systems, which are essential for high-density GPUs.

-

Supporting infrastructure: Beyond direct consumption in server rooms, copper is crucial for the modernization of power grids supplying power to these facilities. The Chinese operator State Grid announced investments of the order of 4 trillion yuan by 2030, which represents an increase of 40% compared to previous plans.

Copper is also recognized as a metal that can largely replace silver in the construction of modern photovoltaic panels. Although significantly more copper is needed when building a panel, at current silver prices—which reach $88 per ounce, or approximately $2.8 million per tonne—the price of copper at the level of $14,000 per tonne is extremely low.

The scale of demand from new technologies in 2026

Forecasts indicate that the demand for copper from data centres will reach a level of 475,000 tonnes per year in 2026 (JP Morgan). This is demand with low price elasticity, as investments in AI infrastructure, conducted by companies such as Microsoft, Google, or Amazon, are key to their competitive advantage, which makes them willing to accept higher raw material prices.

While new data centres can be commissioned within a dozen or so months, the investment cycle in copper mines (from discovery to production) lasts on average from 10 to 20 years. This mismatched response time of supply to a sudden surge in technological demand constitutes the main argument for proponents of the theory of a permanent structural deficit.

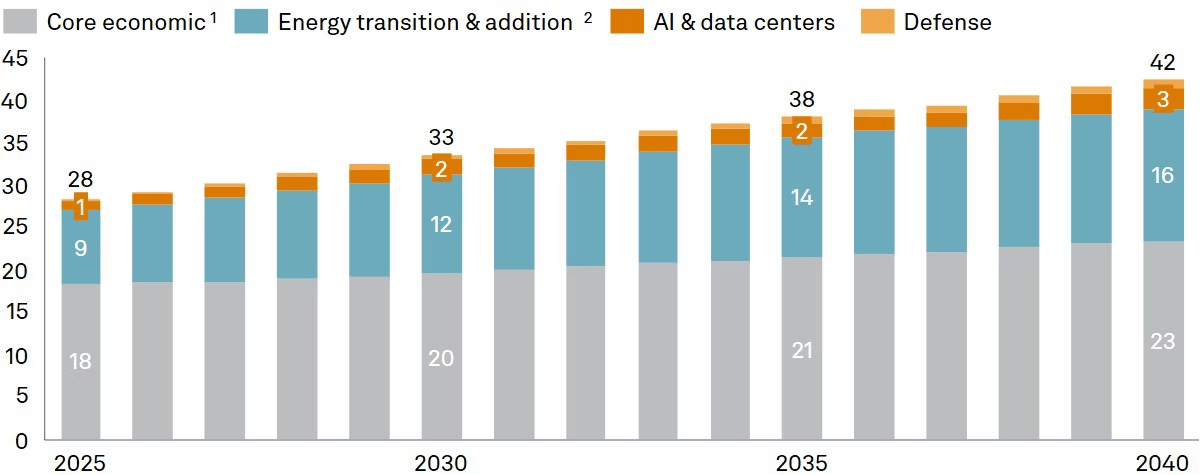

S&P indicates that the demand for copper will grow from around 28 million tonnes in 2025 to 42 million tonnes in 2040. Taking into account the fact that a large part of copper will be locked into technological infrastructure and will not increase the potential supply for recovery, long-term trends point to a structural deficit in the copper market.

Although AI does not seem to be a large piece of the pie in the entire structure of copper demand (the factor related to energy transformation has a much larger impact), given the problems with supply development, even 2 million tonnes of additional demand at the current level of 28 million tonnes makes a significant difference. Source: S&P Global

Although AI does not seem to be a large piece of the pie in the entire structure of copper demand (the factor related to energy transformation has a much larger impact), given the problems with supply development, even 2 million tonnes of additional demand at the current level of 28 million tonnes makes a significant difference. Source: S&P Global

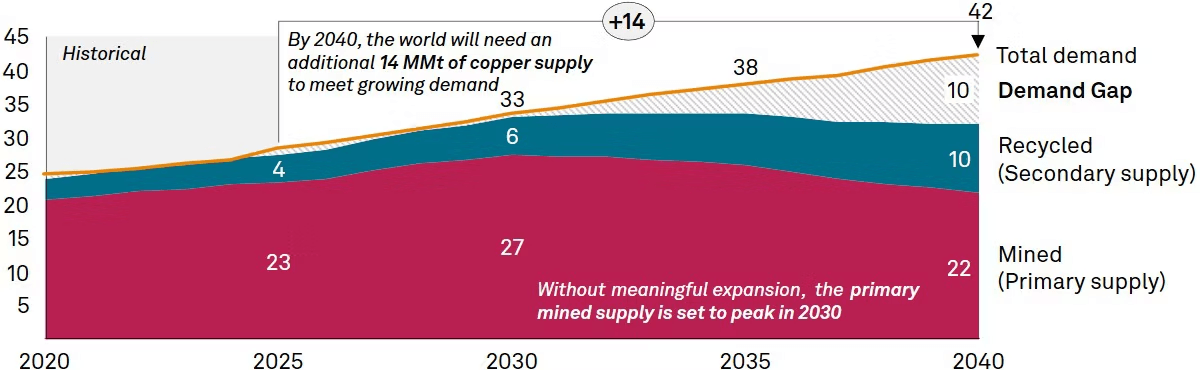

At the same time, supply forecasts do not look encouraging. We are already observing a deficit and a lack of strong growth in access to copper from recycling, even at significantly higher prices than a few years ago. Nevertheless, it is worth noting that the predicted supply "hole" is expected to appear after 2030. By that year, new mining capacities will most likely be opened, although without a major influx of new projects. Source: S&P Global

At the same time, supply forecasts do not look encouraging. We are already observing a deficit and a lack of strong growth in access to copper from recycling, even at significantly higher prices than a few years ago. Nevertheless, it is worth noting that the predicted supply "hole" is expected to appear after 2030. By that year, new mining capacities will most likely be opened, although without a major influx of new projects. Source: S&P Global

Analysis of market fundamentals: AI hype or real change?

Despite record prices, the fundamental picture of the copper market in May 2026 is ambiguous and contains a number of contradictions that require an in-depth analysis of inventories and the behavior of institutional investors.

The inventory paradox and "Project Vault"

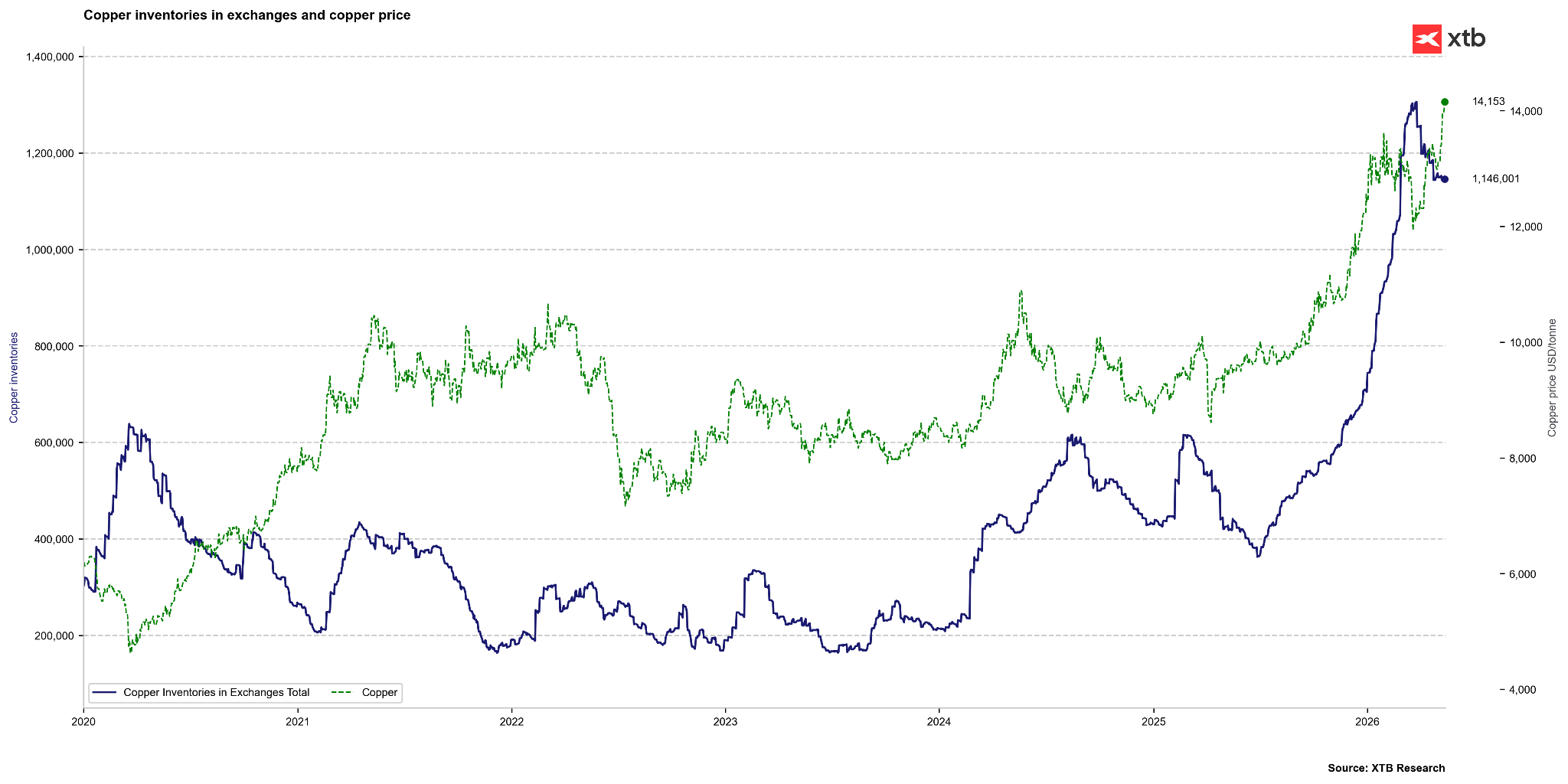

Observed copper inventories on global exchanges (LME, Comex, SHFE) have exceeded the level of 1 million tonnes, which is the highest reading since 2003. In normal conditions, such high inventories would suggest oversupply and pressure for price declines. However, the current situation is distorted by strategic and political factors.

-

Accumulation in the USA: Over 50% of world observed inventories are currently in the warehouses of the Comex exchange in the United States. This is the result of mass imports (1.7 million tonnes in 2025) driven by fears of the introduction of tariffs on refined copper by the Trump administration. At this point, tariff rates of 50% apply to semi-finished copper products, not refined copper itself. However, it is worth emphasizing that Trump suggested the entry into force of new tariffs on a wider spectrum as early as 2027. Nevertheless, the difference between the price on COMEX and LME has fallen significantly compared to the situation a year ago.

-

"Vault" Strategic Reserve: The US government has launched the $12 billion Project Vault program aimed at creating strategic reserves of critical minerals. This means that a significant portion of reported inventories is not de facto available to the commercial market, creating a false sense of abundance.

-

Physical availability: Although total inventories account for over 15 days of global consumption (compared to a historical average of 7 days), the copper realistically available on the LME and SHFE exchanges is sufficient for only 7.5 days, which is a level consistent with the norm and justifies the persisting tension in the physical market.

Global inventories in the copper market remain very high. Source: Bloomberg Finance LP, XTB

Global inventories in the copper market remain very high. Source: Bloomberg Finance LP, XTB

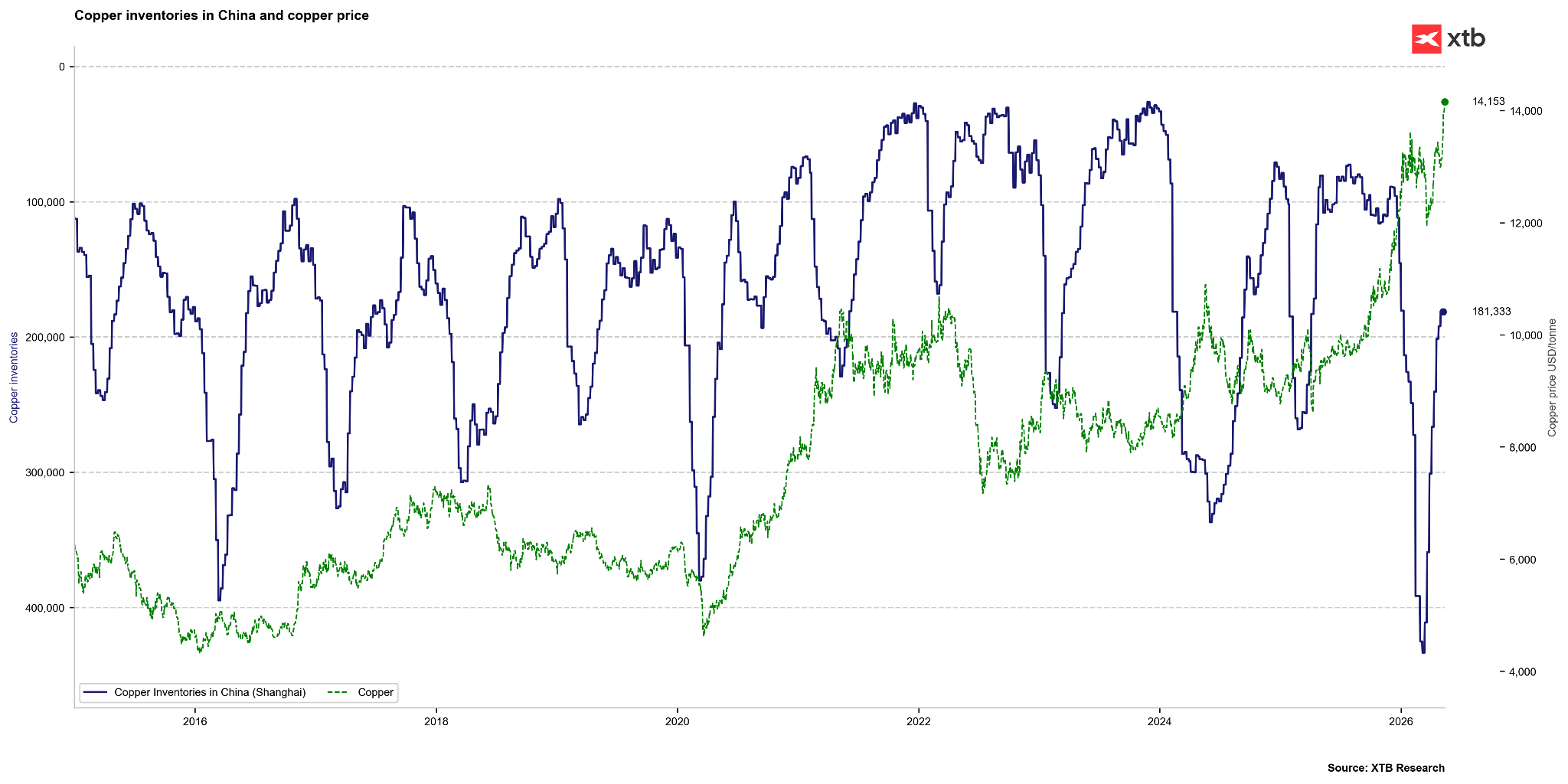

On the other hand, inventories in China on the Shanghai exchange have fallen quite significantly this year from over 400,000 tonnes to approximately 180,000 tonnes. In this chart, the axis for inventories is inverted. Although the drop in inventories in China is extreme, their level is not as low as it was in 2021, 2022, or 2024. Source: Bloomberg Finance LP

On the other hand, inventories in China on the Shanghai exchange have fallen quite significantly this year from over 400,000 tonnes to approximately 180,000 tonnes. In this chart, the axis for inventories is inverted. Although the drop in inventories in China is extreme, their level is not as low as it was in 2021, 2022, or 2024. Source: Bloomberg Finance LP

Market valuation vs. fair value models

Analysis of econometric models indicates a significant deviation of market prices from industrial fundamentals.

-

Impact of AI sentiment: Regression models presented by Bloomberg suggest that copper is currently valued more as a "proxy" for the technology sector and risk appetite related to AI than based on current physical demand. According to these models, copper could be perceived as undervalued by nearly 16% if the AI trend maintained its dynamics, suggesting a level of as much as $16,000.

-

Institutions such as Goldman Sachs point to an "overshooting" of fundamentals, estimating the fair value of the metal at approximately $11,500 per tonne. These experts predict a price correction at the end of 2026, when the tariff situation in the USA is clarified, and high prices lead to demand destruction in more sensitive sectors, such as construction.

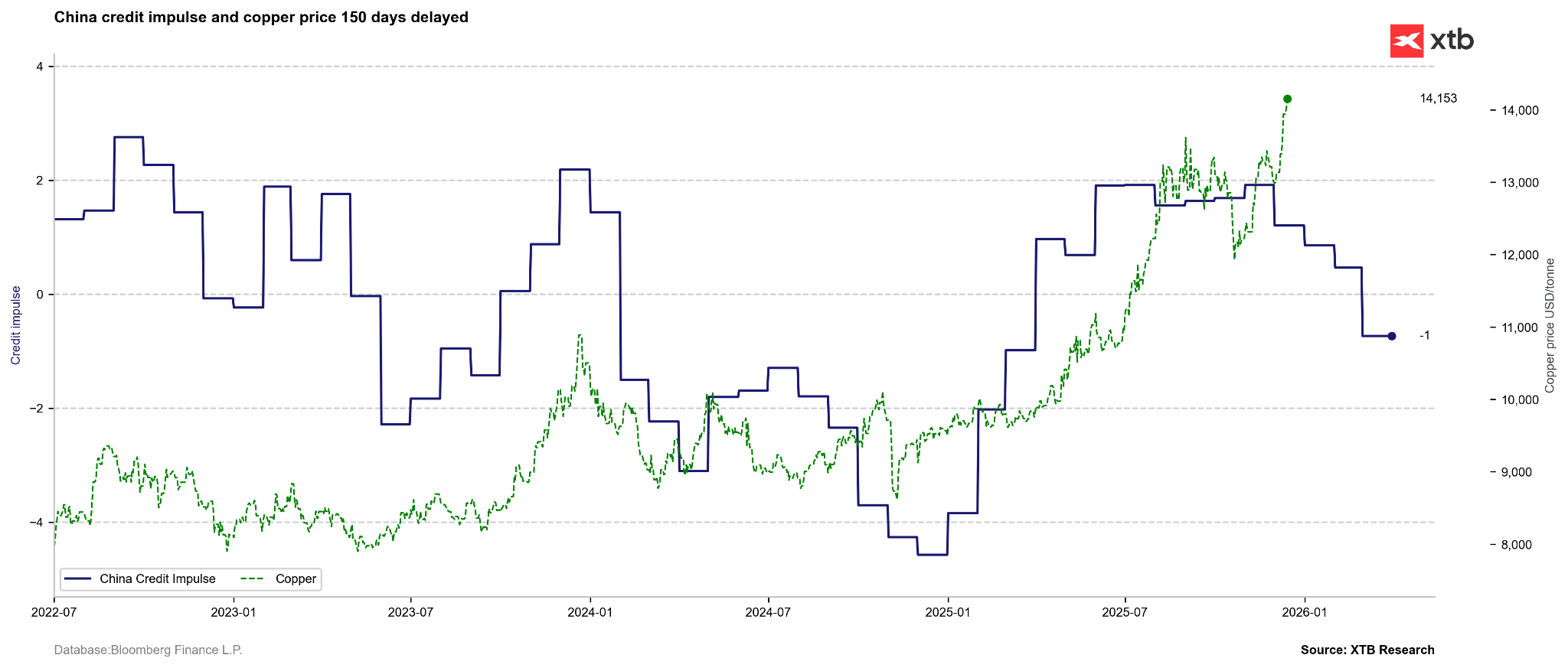

Although energy and AI currently constitute promising long-term demand for copper, the basis of copper demand is still infrastructure, mainly in China. Therefore, a leading indicator for copper may be the credit impulse. This suggests a decoupling of copper prices from key fundamentals, although it is simultaneously worth noting that we observed a similar pullback in the credit impulse indicator from July 2024 to the beginning of 2025. Prices were then in a recovery mode, although at some point a significant correction appeared on the market. Source: Bloomberg Finance LP

Although energy and AI currently constitute promising long-term demand for copper, the basis of copper demand is still infrastructure, mainly in China. Therefore, a leading indicator for copper may be the credit impulse. This suggests a decoupling of copper prices from key fundamentals, although it is simultaneously worth noting that we observed a similar pullback in the credit impulse indicator from July 2024 to the beginning of 2025. Prices were then in a recovery mode, although at some point a significant correction appeared on the market. Source: Bloomberg Finance LP

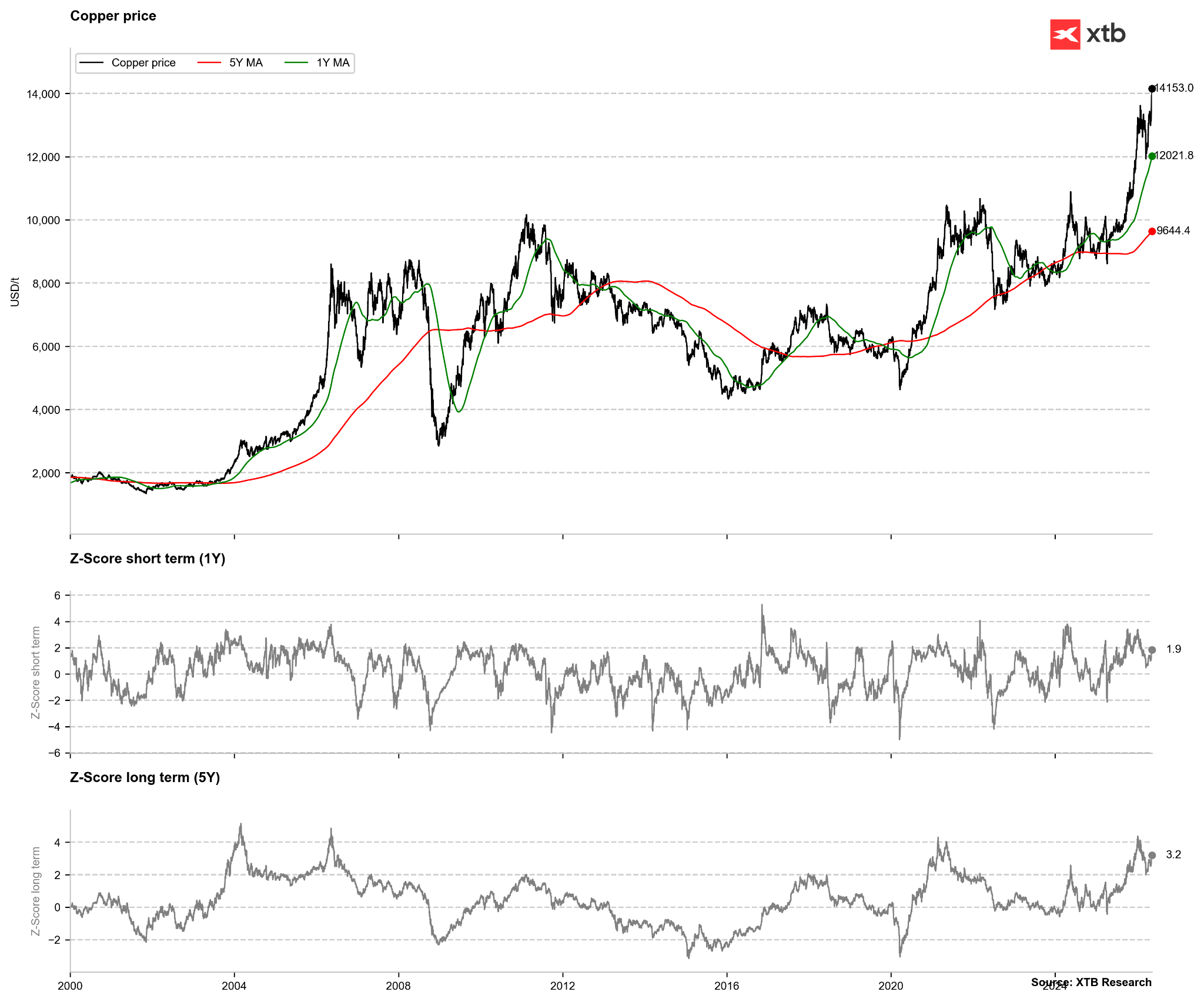

Looking purely technically at copper, one cannot speak of extreme overvaluation. The price is deviated 2-fold from the 1-year average, but after 2020 a 3.5-4-fold deviation from this average was needed to generate a signal. The situation looks similar from the perspective of deviation from the 5-year average. There, a 4-fold deviation is a strong signal. We recently observed such levels, although after the January correction, it was possible to go down to a 2-fold standard deviation. Source: Bloomberg Finance LP

Looking purely technically at copper, one cannot speak of extreme overvaluation. The price is deviated 2-fold from the 1-year average, but after 2020 a 3.5-4-fold deviation from this average was needed to generate a signal. The situation looks similar from the perspective of deviation from the 5-year average. There, a 4-fold deviation is a strong signal. We recently observed such levels, although after the January correction, it was possible to go down to a 2-fold standard deviation. Source: Bloomberg Finance LP

Summary of key copper market parameters

The following summary synthesizes the most important data and trends observed in the current cycle:

-

Copper is brushing against historical records: on the LME exchange, the tonne has exceeded $14,000, which means we are just a fraction away from breaking the all-time high. In the USA, the situation is even more tense, as premiums have breached the $500 barrier.

-

Mining again under pressure. Chile, the world leader, recorded a 6% drop in production in Q1, and we will wait until 2028 for the full restart of the giant Grasberg mine in Indonesia. This blocks about 3% of global supply.

-

Logistics and chemistry are throwing obstacles. China is not only limiting the production of pure metal but has also banned the export of sulphuric acid. Without it, smelters in other parts of the world have a huge problem with technological processes.

-

Artificial Intelligence and armaments are driving the hunger for metal. AI data centres need an additional 110,000 tonnes of copper per year, and at peak, this demand could even exceed 2 million tonnes, while NATO countries, pumping as much as 5% of their GDP into the army, consume huge amounts of the raw material for the production of modern military electronics.

-

Capital is fleeing into commodities. Investors see what is happening, causing the value of ETF funds investing in industrial metals to skyrocket in a year from $37 billion to over $87 billion.

-

The search for savings by force begins. Copper has become as much as 4.5 times more expensive than aluminium. Due to such a drastic difference, car and cooling system manufacturers are desperately trying to replace copper with anything cheaper, although technologically this is a significant challenge. At the same time, copper is also an alternative for more expensive metals like silver or gold.

Summary and Conclusions

Copper is certainly a key metal from the perspective of global development in the fields of energy and artificial intelligence. At the same time, it also constitutes the basis from the perspective of building traditional infrastructure. Supply problems are occurring more and more frequently and are related to factors such as costs, politics, or even weather. Nevertheless, it is worth emphasizing that price increases currently may be related to short-term factors, and additionally, there is a risk of releasing significant supply from the United States if there were no further tariff escalation. That is why it might turn out that copper in the short term is not justified at such high levels, although at the same time, from a long-term perspective, it seems that it is still very cheap. Looking at other key commodity markets, we can see that quite often, in a perspective of several years, it was possible to reach returns at the level of 100 or even 200%. That is why copper, from a long-term perspective, still seems to be an interesting metal.

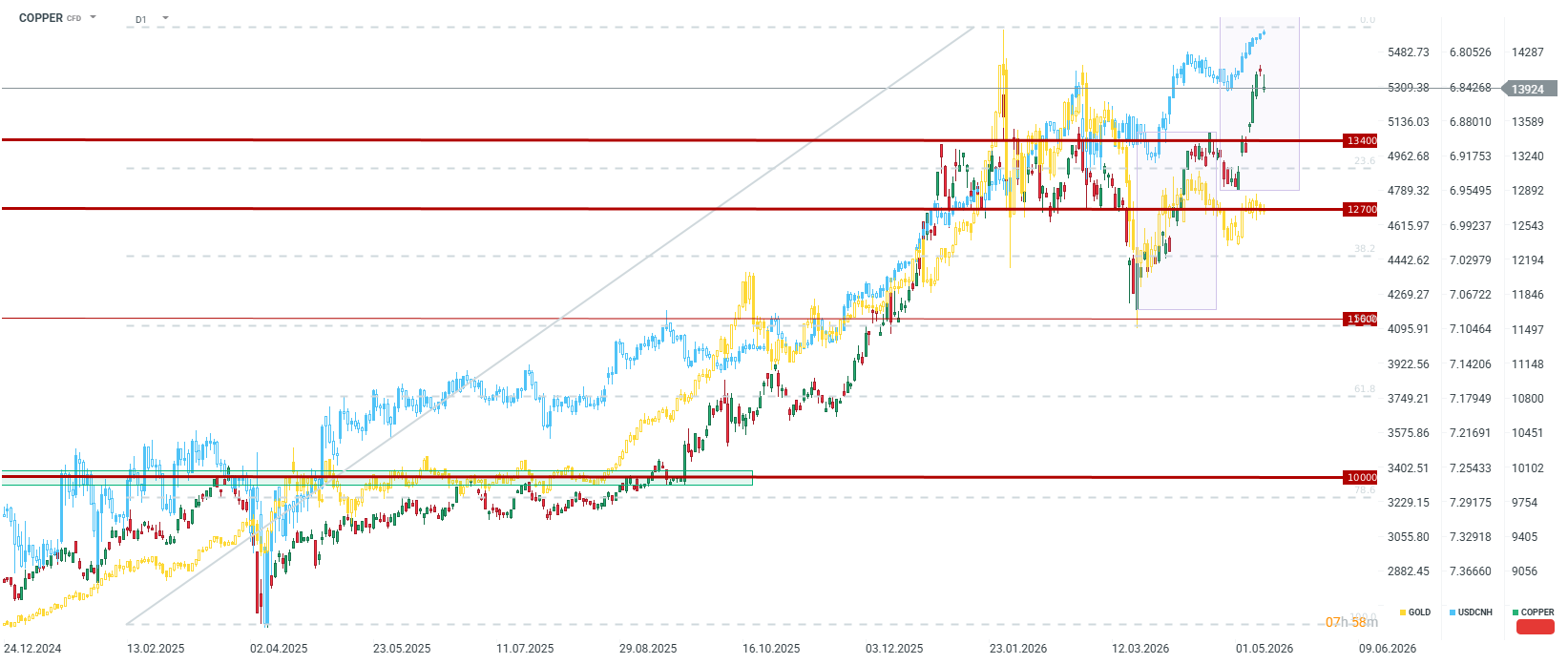

Looking purely technically, comparing the current wave to the one started in March should lead us even to the range of $14,660 per tonne, which would lead to setting new historical peaks in the London price. It can also be seen that copper is very strongly correlated with the Chinese yuan. If the latter continues to strengthen, there is a high probability of continuing the movement in the further medium- and long-term trend. Nevertheless, a sudden strengthening of the dollar, which could occur, for example, in the event of a geopolitical risk, could bring prices down to around $12,700–$13,400 per tonne. At the same time, however, supply problems and hopes related to AI should lead to this range constituting the bottom for the price, at least in the short-term context.

US OPEN: The market extends losses as investor concerns grow

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

Worse than the Dot-com bubble: IBM stock crash

Daily Summary - Escalation in the Middle East. FOMC fears inflation

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.