The world’s largest publicly traded company will report its results on Wednesday after the close of trading in the U.S. What are expectations, and what do they say about where markets stand?

A phenomenon observed repeatedly during earnings season has been the market’s anticipation of Nvidia’s results, which, simplified but broadly accurately, serve as a barometer of the strength of valuation expansion driven by the AI wave. This time is no different. However, the market is beginning to doubt not so much the investment thesis itself, but is bending under the pressure of the macroeconomic backdrop.

The massive CAPEX outlays that are a necessary condition for delivering the profits investors expect are now being questioned in light of rising bond yields.

Expectations for the results are conservative by the standards investors and technology leaders have grown accustomed to.

- Revenue is expected to be around $78.8 billion for Q1 2026, representing approximately 78% YoY growth.

- EPS is expected to come in at about $1.75, implying 127% YoY growth.

- This is expected to translate into an operating margin of 75% and a net margin of 55%.

It’s also likely that more important than headline revenue will be the growth rates of individual segments.

- While the compute segment (about 80% of revenue) is expected to grow "only" 78%, the networking segment is expected to grow by more than 150%.

Chance of Success

Despite the complexity of the financial and technical issues involved in investing in AI or semiconductor companies, and despite the many uncertainties around the quality and durability of growth in this sector, Nvidia is an unusually predictable player within it.

More than half of Nvidia’s revenue comes from just five companies: Microsoft, Amazon, SMC, Meta and Google, with Microsoft and Amazon alone accounting for 36% of revenue. In a typical market context, this would be a significant risk, but in Nvidia’s specific case it works in its favor. All of these companies continue to raise their CAPEX budgets, which they allocate largely to purchases from Nvidia. As long as their CAPEX continues to rise, Nvidia’s revenue should rise as well.

Is the Peak Behind Us?

While one should not expect Nvidia’s profits to decline in the near future - or even the growth rate of those profits - many figures suggest the company’s best period may already be behind it. Why?

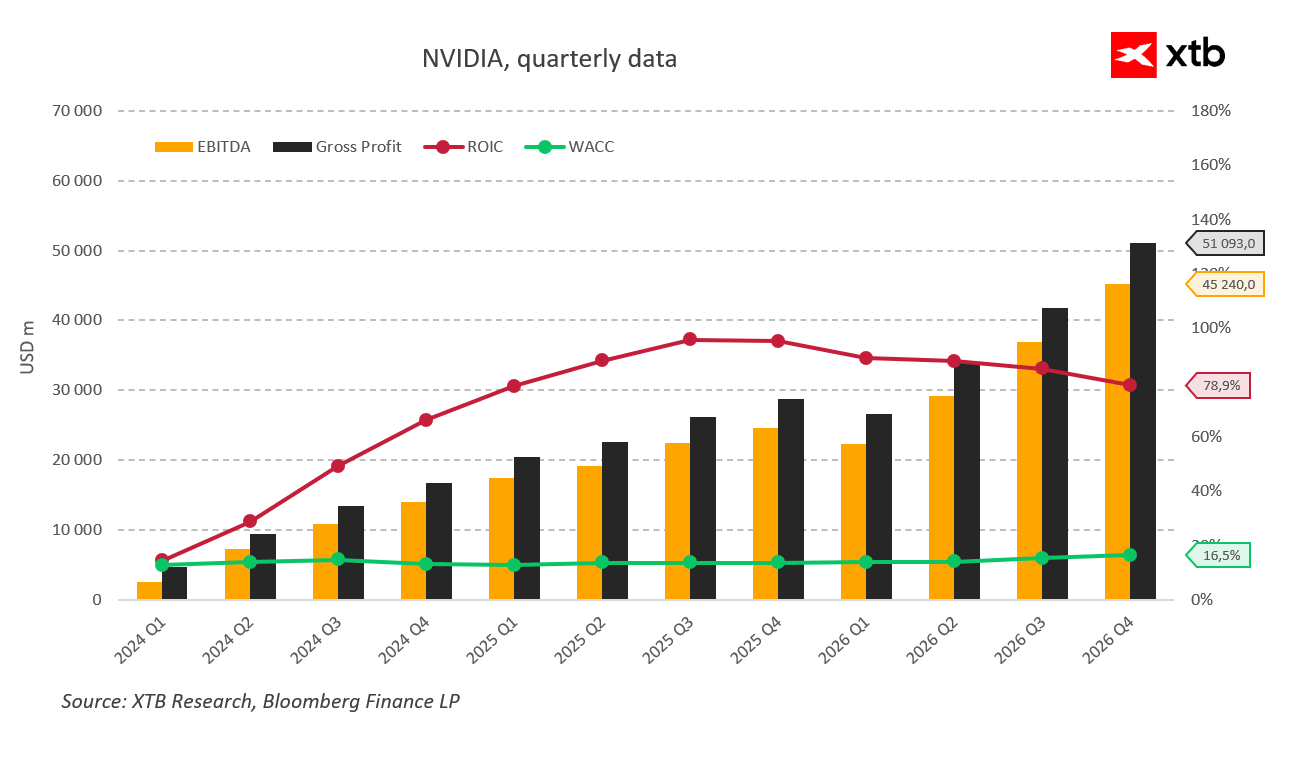

The key signposts are ROIC and WACC.

- Return on invested capital (ROIC) peaked in mid-2024 (fiscal Q3 2025) at 95%. Since then, it has been steadily declining to 78.9%. That is still an impressive level, but it is a clear signal that the segment Nvidia operates in has likely passed its most dynamic growth phase - even if it remains highly profitable versus the broader market.

- Financing conditions also matter. The weighted average cost of capital (WACC) rose over the last four quarters from 13.8% to 16.5%. This happened despite falling interest rates. It clearly indicates that excess liquidity in the market is fading. Nvidia itself is not under the same direct CAPEX financing pressure as hyperscalers are, but those hyperscalers are its main customers. Pressure on CAPEX is pressure on Nvidia’s results. A further rise in WACC could signal growing pessimism among lenders and investors, and the larger that increase, the greater that pessimism.

- But why would a company earning $42 billion in net profit quarterly need additional financing at all? Because to justify its valuation, it must simultaneously maintain its share buyback program while investing more and more.

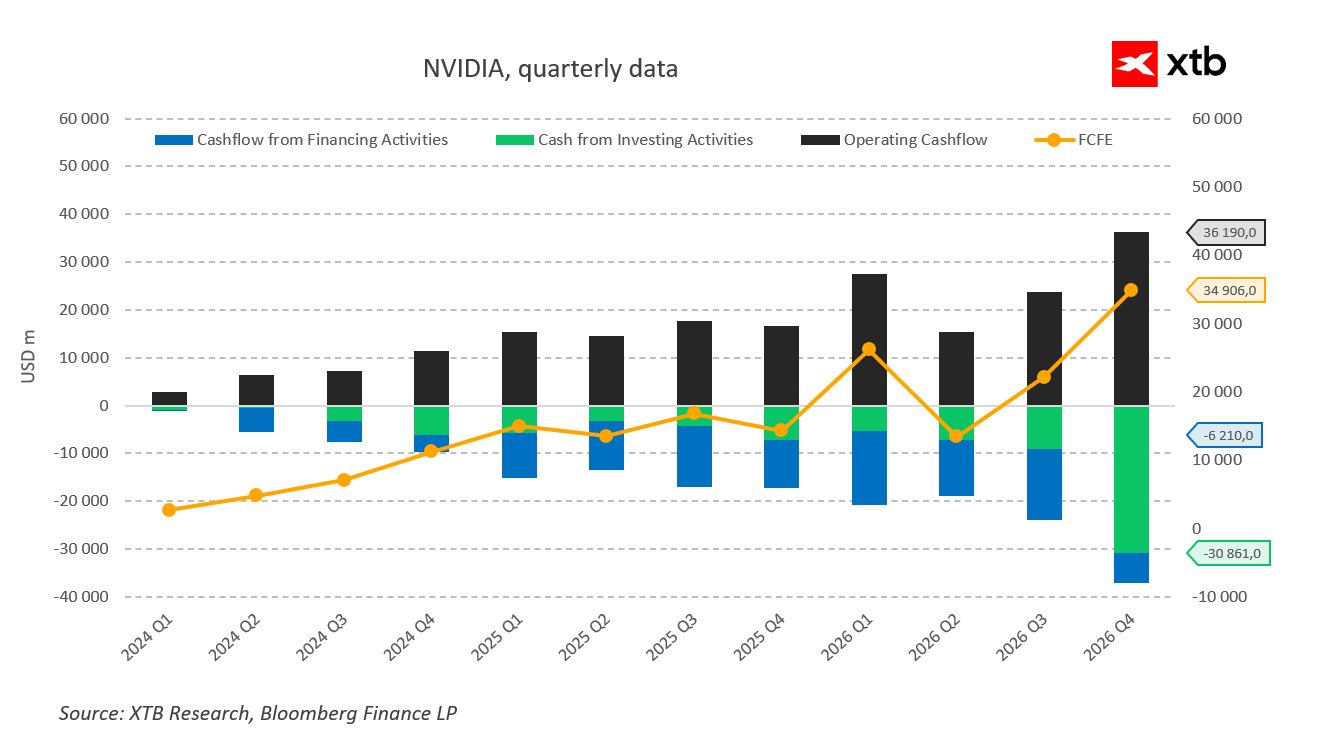

- Negative cash flows in the “Other” investing category increased from $3.6 billion at the start of last year to $16.4 billion in the previous quarter - an increase of 450%.

- At the same time, share repurchases slowed from $13.7 billion to $3.8 billion. This is a clear sign of shifting priorities - from rewarding shareholders to investing. Investments that are becoming less and less profitable.

Conclusion

Historically, Nvidia’s growth remains phenomenal, and the company is still extremely profitable. Significant declines or disappointments in upcoming earnings calls should not be expected, although they are not impossible. However, regardless of delivered results and beats versus consensus, cracks are appearing in the background—cracks the market will likely ignore until the last moment. At the same time, earnings growth alone will not be enough to meaningfully lift already high valuations; optimistic guidance and new growth channels would be required - something for which there is currently no evidence.

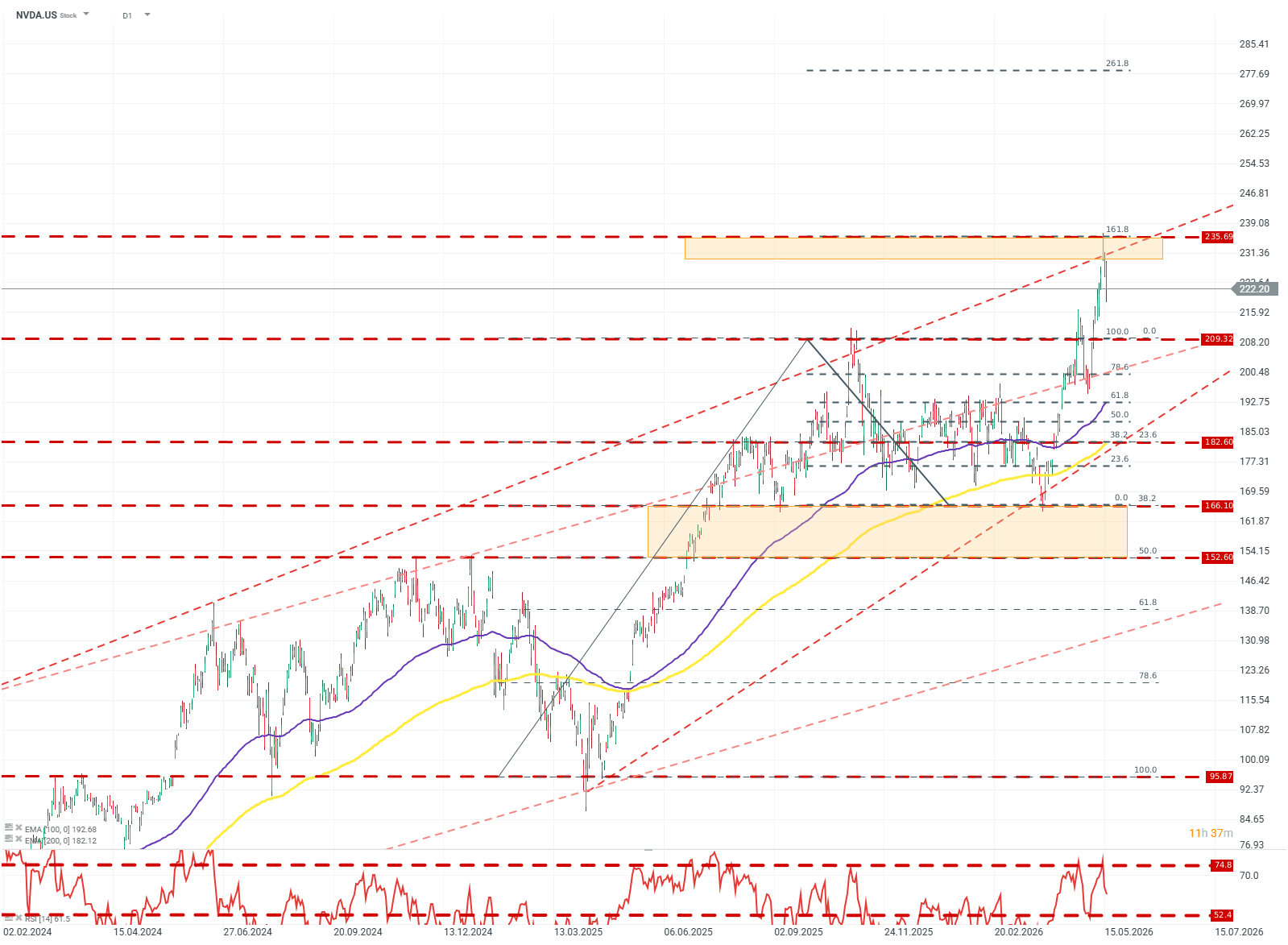

NVDA.US (D1)

The price broke out of a broad consolidation channel between $209 and $156, moving at the same time above the upper boundary of the 2024 uptrend line. After the breakout, the stock rapidly lost momentum after RSI crossed 74 and price reached resistance at the 161.8 Fibonacci level. At present, based on reactions at Fibonacci levels and the structure of moving averages, the base case would be consolidation in the $209–$235 range, with the potential for an upside break and a move toward the 261.8 Fibonacci level. Source: xStation5

US OPEN: The market extends losses as investor concerns grow

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

Worse than the Dot-com bubble: IBM stock crash

Daily Summary - Escalation in the Middle East. FOMC fears inflation

The material on this page does not constitute as financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other particular needs.

All the information provided, including opinions, market research, mathematical results and technical analyses published on the website or transmitted to you by other means is provided for information purposes only and should in no event be interpreted as an offer of, or solicitation for, a transaction in any financial instrument, nor should the information provided be construed as advice of legal or fiscal nature.

Any investment decisions you make shall be based exclusively on your level of understanding, investment objectives, financial situation or any other particular needs. Any decision to act on information published on the website or transmitted to you by other means is entirely at your own risk. You are solely responsible for such decisions.

If you are in doubt or are not sure that you understand a particular product, instrument, service, or transaction, you should seek professional or legal advice before trading.

Investing in OTC Derivatives carries a high degree of risk, as they are leveraged based products and often small movements in the market could lead to much larger movements in the value of your investment and this could work against you or for you. Please ensure that you fully understand the risks involved, taking into account your investments objectives and level of experience, before trading, and if necessary, seek independent advice.