The U.S. dollar is strengthening against the euro after U.S. inflation showed a lower rate of decline yesterday, and members of the Federal Reserve spoke quite hawkishly, signaling an extended hike cycle. In addition, the leader of the Republicans, McDonell indicated yesterday that the party would not stand in the way of raising the debt limit thus lowering the risk of a US 'default'. A slightly more dovish message from Patrick Harker, head of the Philadelphia Fed, was balanced by hawkish Thomas Williams, head of the New York Fed.

Biden's choice

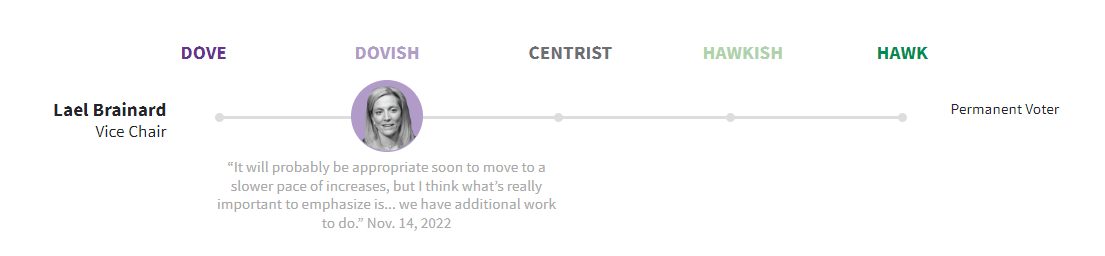

Joe Biden has appointed Jared Bernstein and Lael Brainard to key economic posts. Bernstein, who in the past has leaned toward 'Modern Monetary Theory,' an economic theory that considers near-zero interest rates appropriate, will become the White House's chief economist. Brainard, a Fed deputy governor known for her more dovish stance, will now be the president's chief economic advisor.

In the past, Brainard has emphasized the 'two-sided' risk of rate hikes, and has often focused more on it than on controlling inflation. If nothing changes, we can assume that in view of the slowing economy, Brainard will speak in favor of rate cuts even if inflation does not reach the 2% target. Source: Reuters

Fed Harker

- We need to be cautious about rate hikes during balance sheet reduction but should maintain the path of 25 bps rate hikes;

- The Fed is not yet finished with the hike cycle but is probably close. Deciding in March is not yet a foregone conclusion;

- How much rates will rise above 5% will depend on the data. I see little evidence of a serious slowdown in the labor market but I think unemployment will rise above 4% this year

- The inflation report showed that inflation has stopped falling rapidly. I forecast core inflation around 3.5% this year, 25% next year and 2% in 2025

- I forecast 1% real GDP growth this year before the economy returns to 2% growth in 2024 and 2025. I do not forecast a recession

Fed Williams

- There is a possibility that the Fed will have to raise rates higher than I predict, and inflation will still remain higher;

- I remain confident that the 2% inflation target will be achieved but the struggle to do so may take several years;

- I expect core PCE inflation to be 3% this year. Perhaps the Fed will cut rates in 2024 and 2025 but only if it is prompted by low inflation;

- The main concern is that high inflation is rooted in social expectations. Higher global growth and constrained supply chains are pro-inflationary - supply and demand imbalances drive inflation;

- The Fed may have a long way to go when it comes to controlling price pressures. Lower growth and higher unemployment will result from lower inflation this year. I estimate that unemployment will rise to 4-5%;

- Recent data support the case for additional rate hikes and show improvement in underlying economic strength. Labor market remains exceptionally strong

EURUSD broke the trend line, the pair settled below the 100 and 200 session averages (black and red line) on the H4 interval, signaling a possible further weakening of the European currency against the dollar.

Source: xStation5

Reggeli összefoglaló: Az olaj ára ismét emelkedik (07.08.2026)

Gazdasági naptár: A vártnál gyengébb foglalkoztatási adatok nyomást gyakorolhatnak-e a Fed-re a kamatemelésre?

Reggeli összefoglaló: A részvények nyomás alá kerültek, miután a Wall Streeten nyereségrealizálásra került sor; a devizapiacok stagnálnak (2026.08.06.)

A nap chartja: Az USDJPY árfolyam 160 alá esett, de a jenre nehezedő nyomás továbbra is fennáll

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.