- First Citizens BancShares reached fresh all-time highs

- Bank reported Q1 2023 earnings on Wednesday

- $9.8 billion gain made on SVB acquisition

- Common equity Tier 1 ratio is one of highest among peers

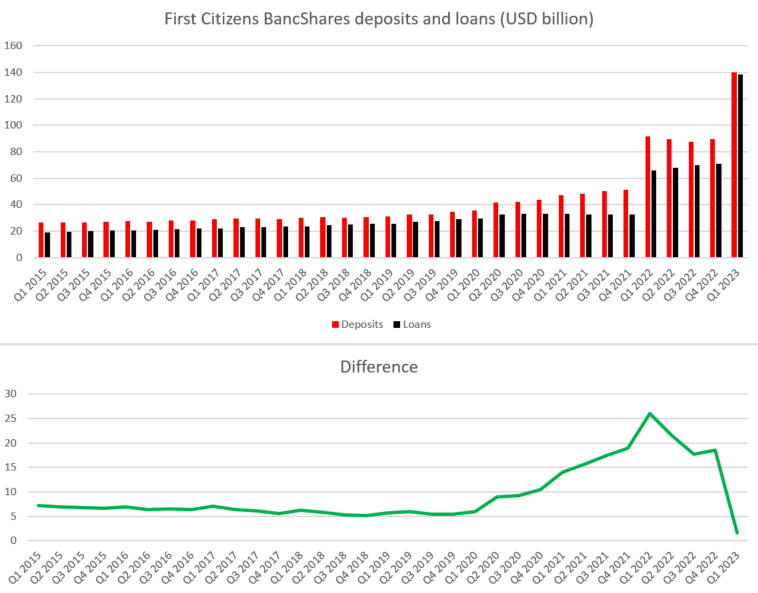

- Excess of deposits over loans at lowest level since Q3 2000

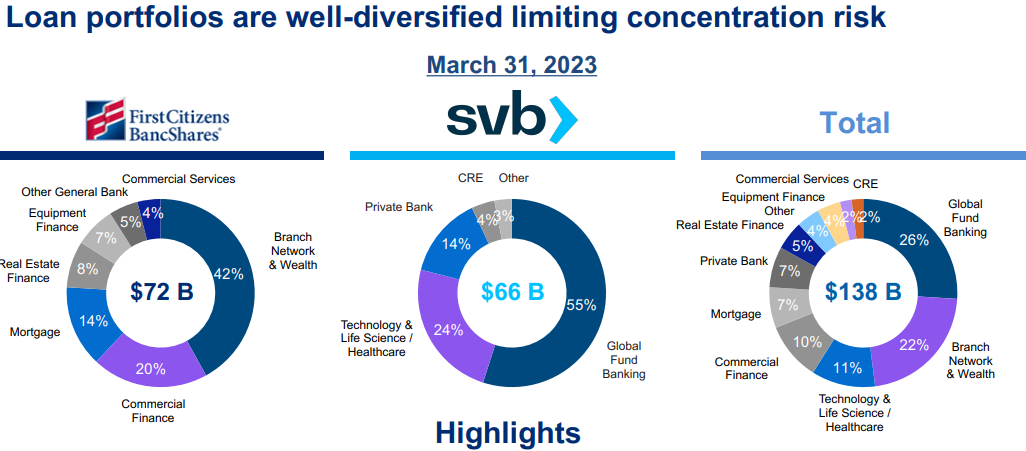

- SVB acquisition allowed for loan portfolio diversification

- First Citizens expects loans and deposits to drop later into the year

While the majority of US bank stocks still lick their wounds after a recent turmoil in the banking sector, especially regional banks, there is one US bank that has just reached a fresh all-time highs - First Citizens BancShares (FCNCA.US). This Bank has been enjoying an upbeat sentiment since the second half of March, when it acquired loans and deposits of a collapsed Silicon Valley Bank. Shares of First Citizens leaped higher this week again after the bank published a Q1 earnings report that included details of SVB acquisition.

First Citizens reports massive increase in deposit and loans for Q1 2023

First Citizens BancShares reported Q1 2023 earnings on Wednesday before opening of US markets. Report turned out to be much better than expected by analysts. Bank reported a massive 57% QoQ increase in deposits and 95% QoQ jump in loans. However, such a massive increase in deposit and loans was driven by a one-off event that occurred at the very end of the quarter - acquisition of loans and deposits from collapsed SVB on March 27, 2023. Company reported a $9.82 billion gain on SVB acquisition. After accounting for increased provisions for credit losses, the company's total net income reached $9.51 billion, making First Citizens BancShares the second most profitable US bank during the quarter (trailing only behemoth JPMorgan which earned $12.6 billion).

A point to note is that the reported Q1 2023 Common Equity Tier 1 ratio at 12.5% is one of the highest among peers, highlighting the quality of asset base of the combined entity.

Q1 2023 results

- Deposits: $140.05 billion vs $118.98 billion expected (+57% QoQ)

- Loans and leases: $138.29 billion vs $85.45 billion expected (+95% QoQ)

- Net Interest Income: $850 million vs $838.2 million expected (+6% QoQ)

- Net Interest Margin: 3.41% vs 3.36% expected

- Common equity Tier 1 ratio: 12.5% vs 9.9% expected

- EPS: $653.64 vs $16.70 in Q1 2022

- Provisions for Credit Losses: $783 million

- Net Income: $9.51 billion

- Gain on SVB acquisition: $9.82 billion

- Adjusted EPS: $20.09

- Adjusted Provisions for Credit Losses: $63 million vs $63 million expected

- Adjusted Net Income: $292 million vs $292.8 million expected ($306 million in Q1 2022)

First Citizens BancShares experienced a massive jump in deposit and loans in Q1 2023, thanks to acquisition of SVB. A big jump in both measures in 2022 was driven by CIT acquisition. However, it should be noted that the difference between deposits and loans dropped to just $1.67 billion - the lowest level since Q3 2000 when First Citizens had only $8.7 billion in total deposits (compared to $140 billion now). Source: Bloomberg, XTB

First Citizens BancShares experienced a massive jump in deposit and loans in Q1 2023, thanks to acquisition of SVB. A big jump in both measures in 2022 was driven by CIT acquisition. However, it should be noted that the difference between deposits and loans dropped to just $1.67 billion - the lowest level since Q3 2000 when First Citizens had only $8.7 billion in total deposits (compared to $140 billion now). Source: Bloomberg, XTB

SVB acquisition

First Citizens BancShares assumed loans and deposits of Silicon Valley Bank on March 27, 2023. As we have already said earlier, the company acknowledged that the massive increase in deposits and loans was driven by SVB acquisition. More precisely, First Citizens acquired a $66 billion loan portfolio from SVB as well as assumed $49.26 billion in SVB deposits. Gain on the acquisition was reported at $9.82 billion, thanks to loan portfolio being purchased at around-20% discount. First Citizens also entered into a loss-sharing agreement with Federal Deposit Insurance Corporation (FDIC) under which FDIC will reimburse 50% of losses in excess of $5 billion over covered assets. The agreement is said to cover an estimated $60 billion in commercial loans.

As a result of acquisition, assets of First Citizens jumped above $200 billion, making it one of 15 largest US banks. Also, the combination of First Citizens and SVB created a banking entity with a much more diversified loan portfolio than either of the two had prior to the acquisition. However, while deposit and loan gains from SVB acquisition were massive, First Citizens may struggle to maintain SVB's clients as it will need to convince them that it is proficient enough and has enough expertise to properly serve clients from tech and life science industries, which were the focus of SVB. The same can be said about SVB employees, it was already reported that HSBC hired over 40 former SVB bankers who worked at First Citizens.

Source: First Citizens BancShares

First Citizens expects deposit outflow later into the year

While First Citizens BancShares, adjusted for effects of SVB acquisition, had a decent first quarter of the year - $1.3 billion QoQ increase in loans and $1.26 billion QoQ increase in deposits - company expects things to deteriorate later. Deposits are said to be down 4% through April and the company expects deposits at the end of Q2 2023 as well as at the end of 2023 to be in the $132-137 billion range - a decline from $140 billion reported for the end Q1 2023. Loans are also seen dropping during the remainder of 2023 and reach $132-135 billion at year's end ($138.3 billion at end-Q1).

Speaking about more precise actions, First Citizens plans to limit origination of new general office loans as the commercial real estate sector is struggling. Commercial real estate loans accounted for almost 12% of First Citizens' $138 billion loan portfolio with 2.1% of all loans being general office loans.

Q2 2023 forecast

- Deposits: $132-137 billion

- Loans and leases: $133-136 billion

- Net Interest Income: $1.8-1.9 billion

Full-2023 forecast

- Deposits: $132-137 billion (exp. $119 billion)

- Loans and leases: $132-135 billion

- Net Interest Income: $6.2-6.5 billion (exp. $4.02 billion)

First Citizens BancShares outperforms broad banking sector

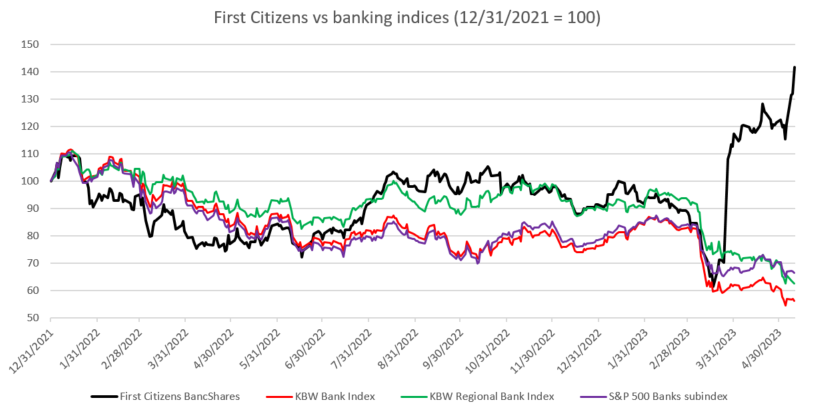

First Citizens BancShares have been performing more or less in-line with the broader banking sector ahead of US banking turmoil in March this year as well as during it. However, things changed after it was announced that First Citizens will acquire SVB. Announcement triggered a massive rally on the company's shares and allowed it to more than recover from previous sell-off. First Citizens continued to move higher afterwards with this week's earnings release triggering another share price spike. As a result, stock reached fresh all-time highs and is trading 40% above end-2021 levels while major US banking sector indices trade 30-40% below end-2021 levels.

First Citizens BancShares began to rally after SVB acquisition while broad banking sector indices continued to struggle. Source: Bloomberg, XTB

First Citizens BancShares (FCNCA.US) at W1 interval. Source: xStation5

First Citizens BancShares (FCNCA.US) at W1 interval. Source: xStation5

Reggeli összefoglaló: A Wall Street újra támadásba lendül, miközben a Palantir tovább erősíti a mesterséges intelligencia iránti optimizmust

Talpra Tréder - 2026.08.03.

Gazdasági naptár: Mi befolyásolhatja a piacot ezen a héten? (2026.03.08.)

XTB eredményjelentés - Netflix

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.