Global markets are set to begin the week with inflation data and central bank decisions firmly in focus. Following Friday’s stronger-than-expected US labour market report, the US dollar strengthened considerably, reducing expectations for near-term Federal Reserve rate cuts. However, investors will receive another round of key economic releases in the coming days that could either reinforce or challenge this narrative. Attention will centre on Wednesday’s US CPI report, Thursday’s European Central Bank decision, and Friday’s University of Michigan consumer sentiment survey. Against this backdrop, traders should pay particular attention to US100, GOLD, and EURUSD, as well as the highly anticipated stock market debut of Elon Musk’s SpaceX.

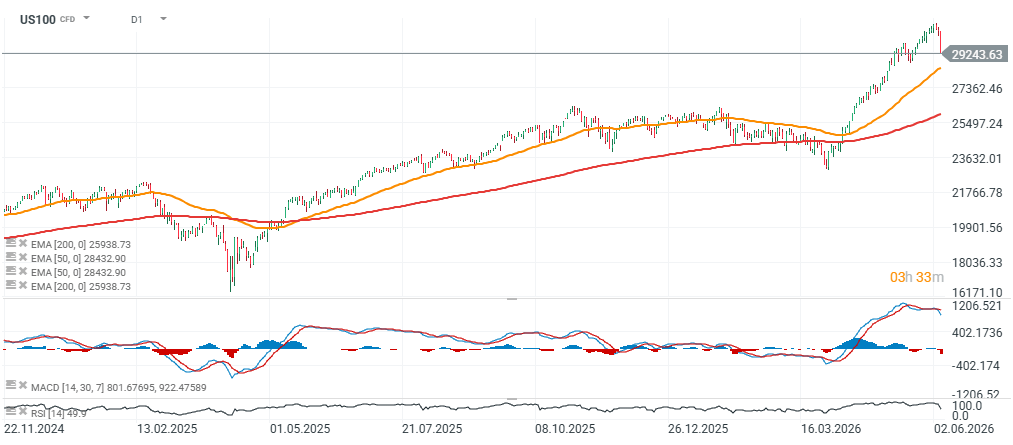

US100

The Nasdaq is set to begin the week after retreating from record highs. Momentum surrounding artificial intelligence has cooled, at least temporarily, although expectations for continued earnings growth among major technology companies remain supported by substantial hyperscaler capital expenditure plans. Valuations across the sector remain demanding, meaning that even modest shifts in monetary policy expectations could trigger elevated volatility.

The key event of the week will be Wednesday’s US CPI inflation report. Following the exceptionally strong Non-Farm Payrolls release, markets have scaled back expectations for the extent of Fed rate cuts this year. If core inflation once again proves sticky, US Treasury yields could move higher, traditionally posing a challenge for growth-oriented sectors represented by US100. Conversely, a softer CPI print could revive hopes for a more dovish Federal Reserve and provide support for technology stocks.

Another major event attracting investor attention will be the planned SpaceX market debut. The June 12 IPO, expected to be the largest in market history, could become another important test of risk appetite and investor demand for high-growth companies.

Source: xStation5

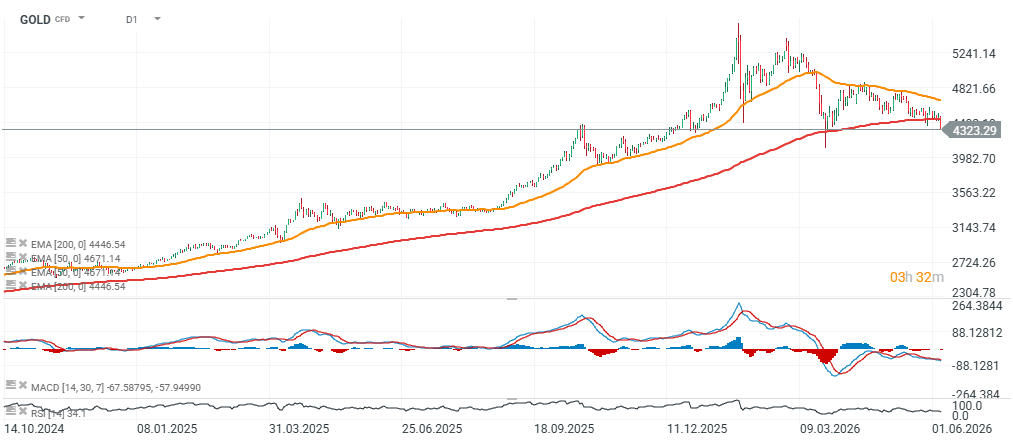

GOLD

Gold ended the previous week under pressure from a stronger US dollar and rising Treasury yields. The robust NFP report served as a reminder that the US economy remains resilient, reducing the likelihood of near-term monetary easing by the Federal Reserve.

The most important test for precious metals this week will come from Wednesday’s CPI release and Thursday’s US Producer Price Index (PPI) report. Should inflation exceed expectations, markets may once again push back the timing of the first Fed rate cut, supporting the dollar and putting further pressure on gold prices. Such a scenario would be particularly unfavourable for the precious metal, which offers no yield and typically struggles to compete with higher-yielding assets.

On the other hand, softer inflation readings could quickly reverse some of gold’s recent losses. Investors remain aware that despite short-term pressure, the metal continues to enjoy structural support from central bank purchases and persistent uncertainty surrounding the global growth outlook. As a result, the coming week may determine whether the recent correction marks the beginning of a deeper decline or merely a temporary reaction to stronger US employment data.

Source: xStation5

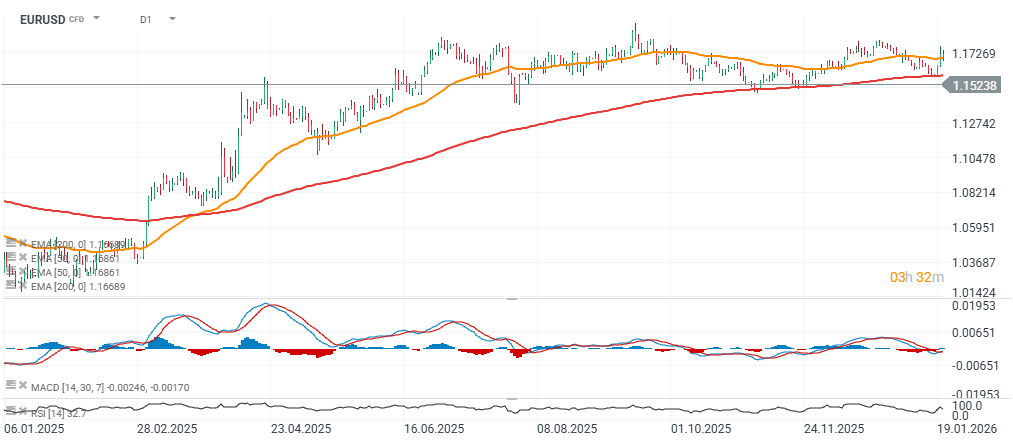

EURUSD

The most important event of the week for the world's most traded currency pair will be Thursday’s European Central Bank policy decision and Christine Lagarde’s press conference. The rate decision itself is unlikely to surprise markets, as investors largely view a 25-basis-point hike as the most probable outcome. Even more important, however, may be the ECB’s forward guidance and updated macroeconomic projections.

In recent weeks, ECB policymakers have increasingly highlighted inflation risks while simultaneously acknowledging that the Eurozone economy continues to face significant challenges, particularly within energy markets. Weak growth prospects and a cautious approach towards further monetary tightening mean that investors will be highly sensitive to any dovish signals emerging during Lagarde’s press conference.

At the same time, the direction of EURUSD will also depend heavily on US inflation data. If US CPI surprises to the upside once again, the divergence between Fed and ECB policy expectations could work in favour of the dollar. Conversely, weaker US inflation data combined with a more neutral ECB tone could allow the euro to recover some of the losses suffered following the strong NFP release. As a result, EURUSD remains one of the instruments most exposed to elevated volatility in the week ahead.

Source: xStation5

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

Wheat extends correction, falls to its lowest level since July 10 🚩 Drought, El Niño and the Black Sea in focus

📉 Natural gas tumbles as US EIA inventories rise

Oil climbs back above $80 per barrel 🔼

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.