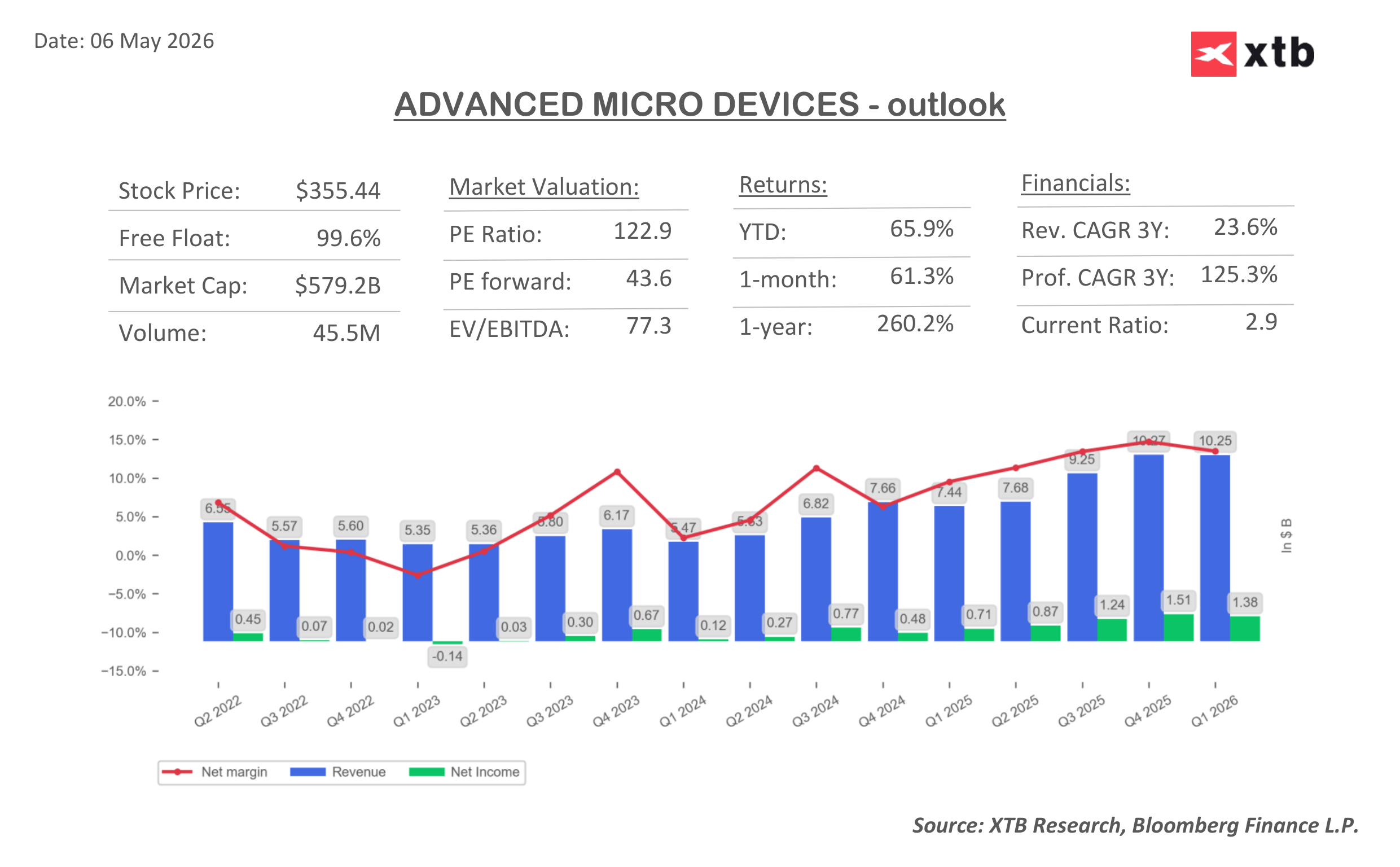

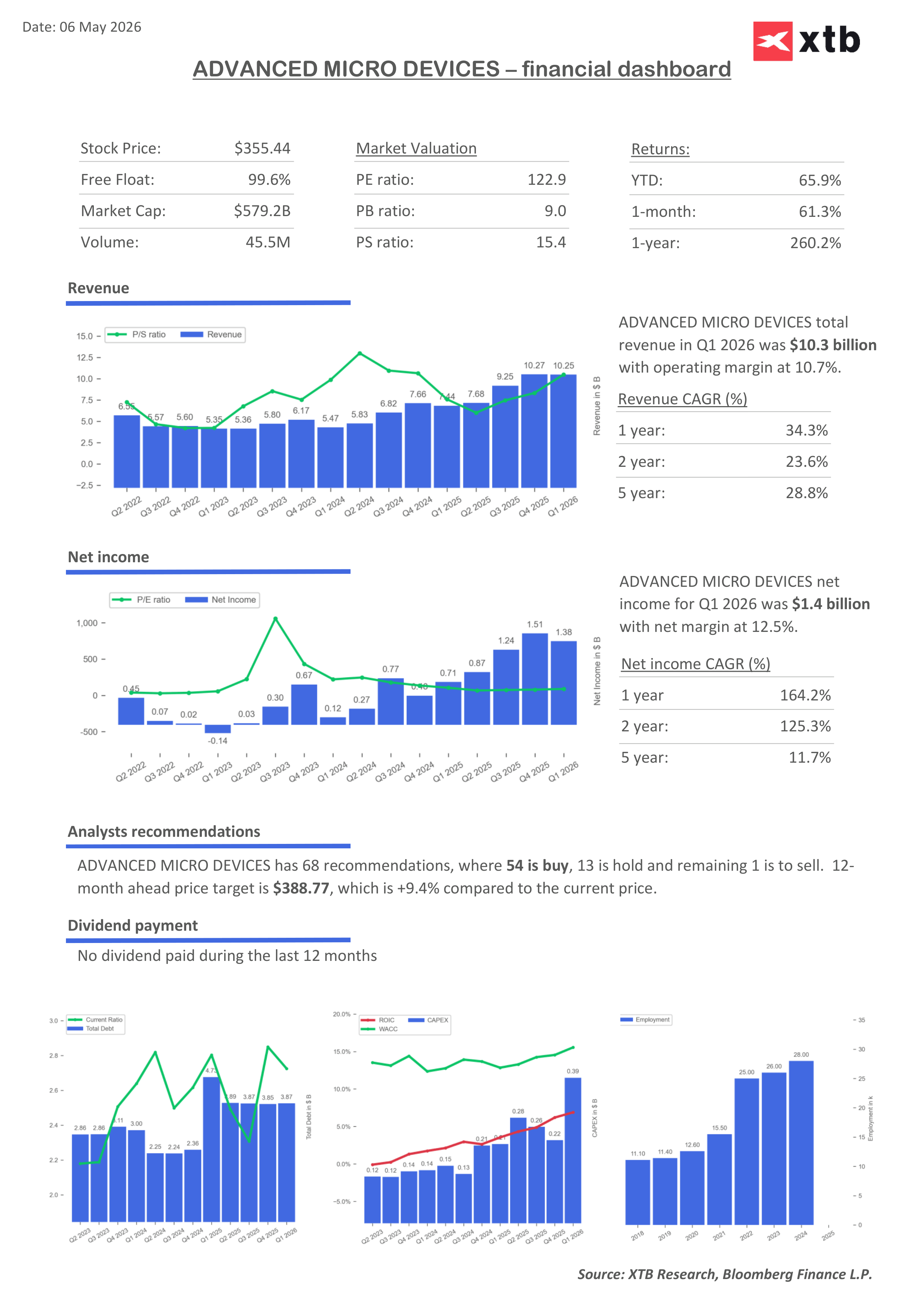

The results of Advanced Micro Devices for the first quarter of 2026 highlight the scale of the transformation the company has undergone in recent years. This is no longer a story of gradual recovery, but of a company that has become one of the key beneficiaries of the global boom in artificial intelligence infrastructure.

AMD clearly exceeded market expectations, delivering revenue of $10.25 billion and earnings per share of $1.37. The growth dynamic remains impressive, but more importantly, it is accompanied by a clear improvement in business quality. The company is not only growing faster, but doing so in an increasingly profitable way, as reflected in expanding margins and strong cash flow generation.

Key financial highlights for the first quarter

-

Revenue $10.25 billion versus expectations of around $9.9 billion, up 38% year over year

-

Earnings per share $1.37 above market consensus

-

Data Center segment $5.78 billion, up 57% year over year

-

Gross margin around 55% with further upside potential

-

Operating margin 25%, improving year over year

-

Free cash flow $2.57 billion, significantly higher than a year ago

At the core of this story is the Data Center segment, which is not only the fastest-growing part of the business but is also redefining the company’s overall profile. A 57% year over year increase is difficult to view as a one-off spike. Instead, it reflects a structural trend in which demand for AI-driven compute power is growing faster than the market previously anticipated. AMD is benefiting both from the expansion of AI accelerators and from its strong position in server CPUs, which are experiencing a clear resurgence.

Against this backdrop, the outlook is particularly important. The company expects second-quarter revenue of around $11.2 billion, above market expectations. This signals that demand remains robust and that the sales pipeline is well supported in the coming months. At the same time, AMD anticipates further improvement in gross margin, suggesting a growing contribution from higher-value, higher-margin products.

Market perception is also evolving. AMD is increasingly seen as more than just an alternative to Nvidia. The scale and growth rate of the AI market leave ample room for multiple major players, and AMD is steadily establishing its position by building a more complete and competitive ecosystem of solutions.

An interesting and often underappreciated element of this story is the role of CPUs, which are returning to the spotlight alongside the rise of new AI applications. As agent-based models and more complex computing environments gain traction, accelerators alone are no longer sufficient. Efficient CPU and GPU collaboration, workload management, and overall infrastructure optimization are becoming increasingly important. This is an area where AMD has deep expertise and a long-standing competitive advantage. In practice, this means the company is positioned to benefit not only from direct AI demand but also from the growing complexity of the systems that support it.

Overall, this report confirms that AMD has entered a new phase of growth. Strong revenue expansion, improving margins, and raised guidance paint a consistent picture of a business capitalizing on one of the most powerful technological trends of recent years. The key question going forward is no longer whether AMD is growing, but how long it can sustain this pace and to what extent it can translate it into further margin expansion.

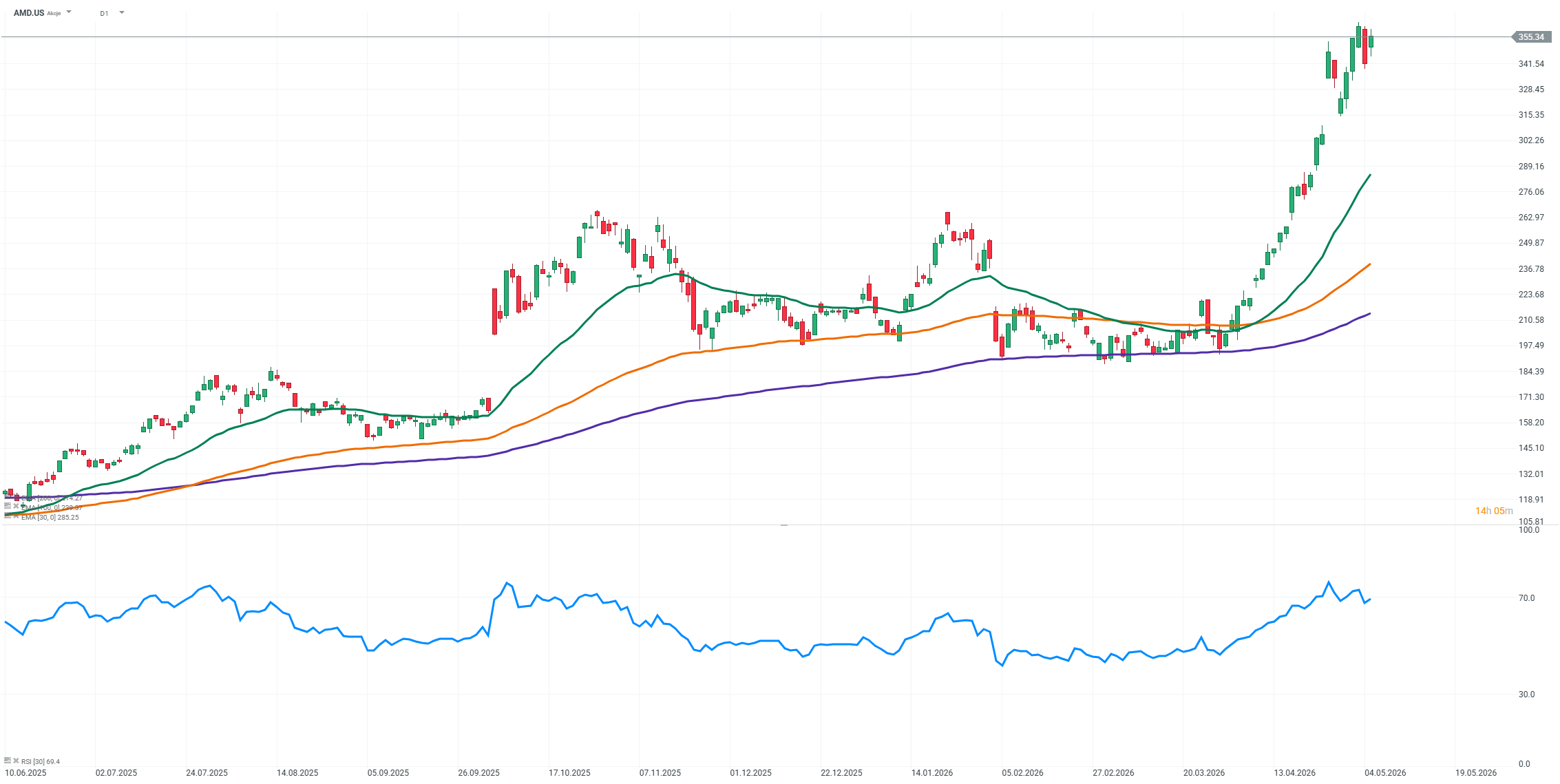

Source: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

Alphabet shares are down 22% from their all-time high 🚩 Is Google ready to resume its bull run?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.