Headlines about successive layoffs, carried out or planned, mostly in the US and mostly in technology-related sectors, have become a kind of folklore, omnipresent across most media focused on the economy or business.

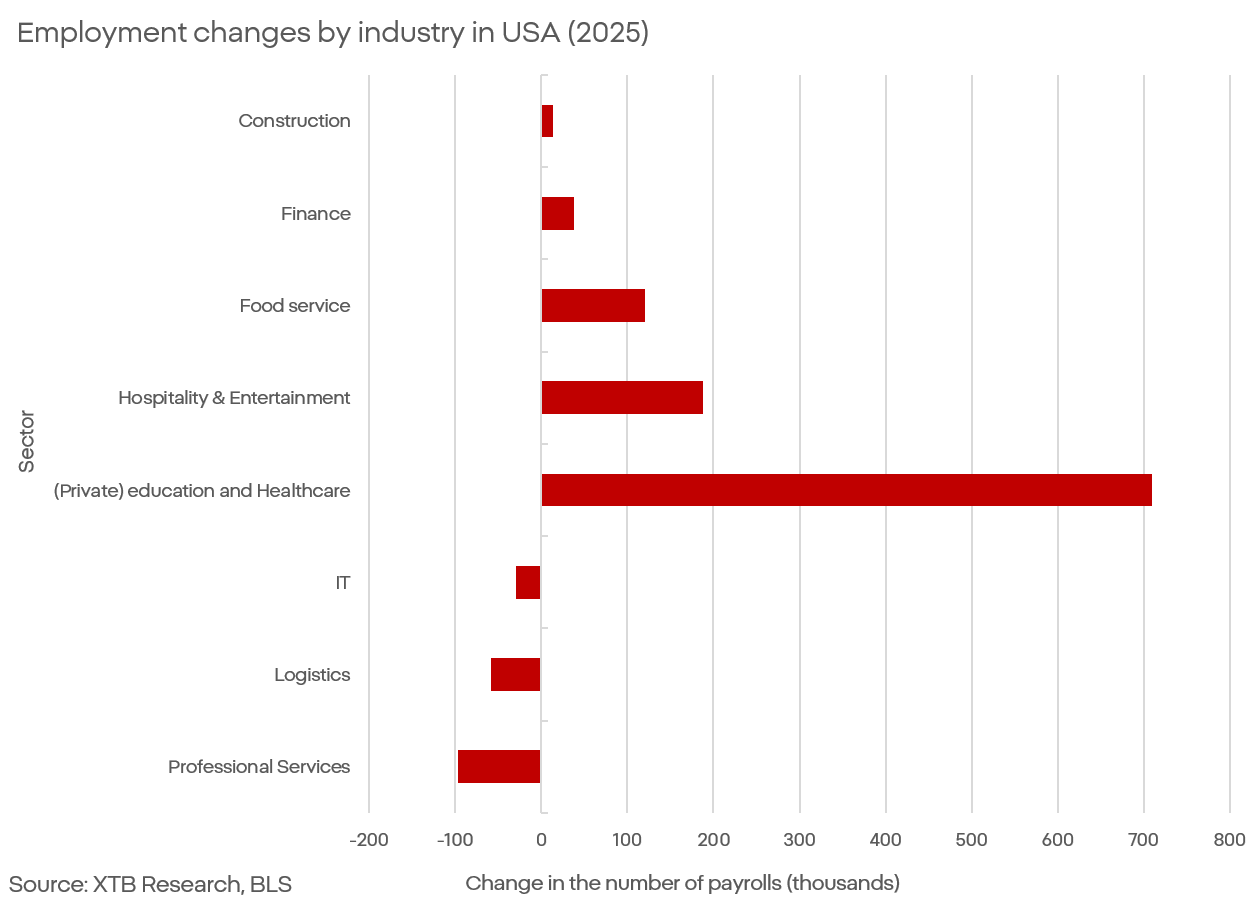

Public sentiment toward the labor market, especially among young people and recent graduates, is becoming increasingly grim. This view is only partially confirmed by the underlying data for 2025. Looking at individual industries, employment in many sectors, particularly those key for “white-collar” workers and young people, has clearly declined. The overall picture, however, still shows a distinct net increase.

What requires particular attention is that employment growth is very heavily concentrated in healthcare and education. Yet the question that should be asked more loudly in the context of the labor market is not whether it is actually deteriorating, but to what extent current trends are truly being driven by AI.

Aggregating official communications from US companies about layoffs, the outlook appears very bleak and pessimistic for people considering changing jobs or finding employment, especially in the technology sector. And perhaps it is, but the data show something different.

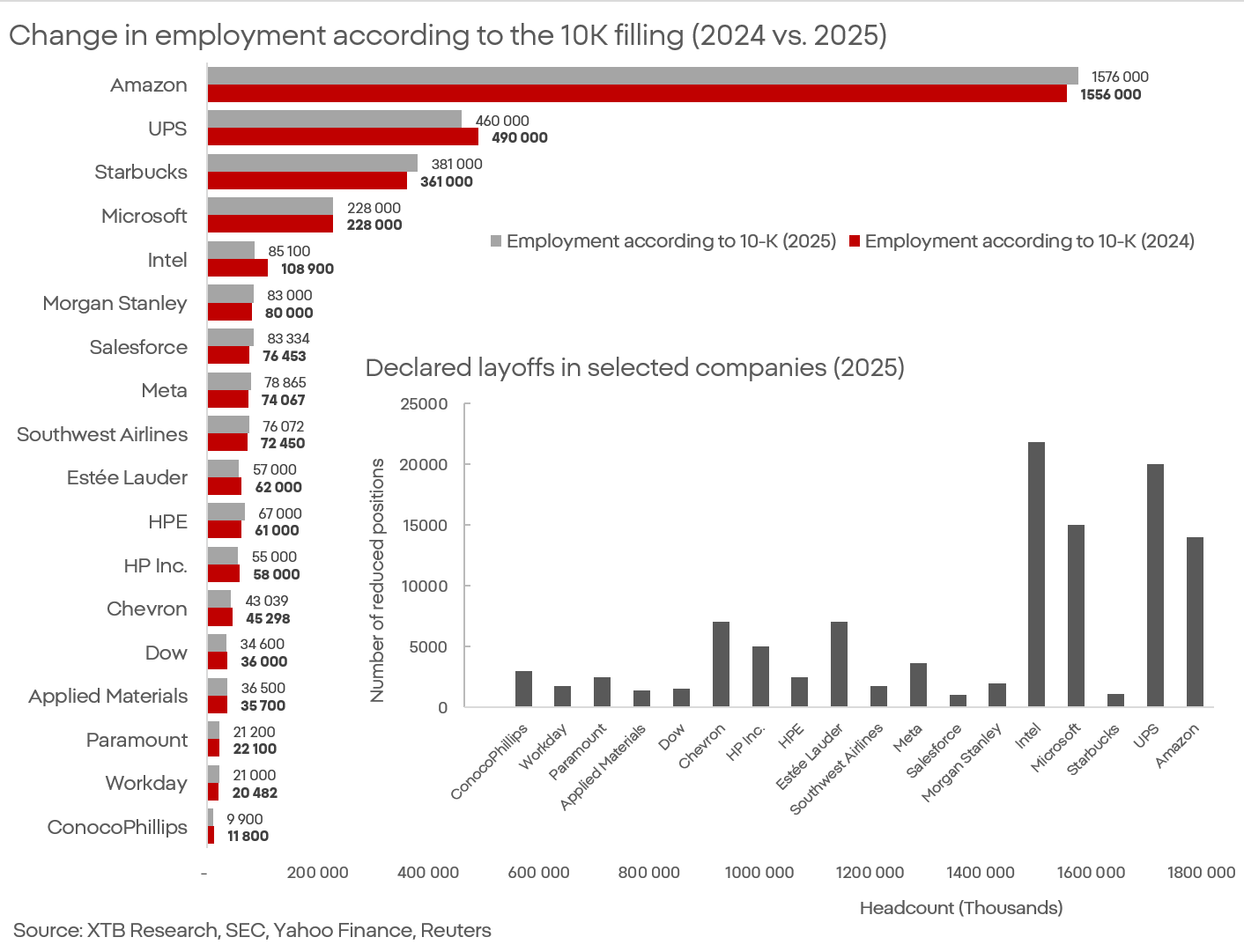

Financial statements or earnings calls rarely, if ever, focus on headcount. US companies do, however, have a regulatory obligation to report the number of employees in their 10‑K filings, and these paint a picture dramatically different from public declarations.

Only a small share of market leaders boasting about workforce reductions actually reported a decline in headcount. Aside from Intel, most decreases are symbolic; increases dominate. Importantly, when comparing these data with trends in financial statements, especially labor costs, you can see a short-term increase that eventually does fall. That indicates cost reductions without changes in headcount, which is characteristic of offshoring.

Why is this dangerous for valuations?

A large part of the stock market gains observed over the last few quarters has been based on the assumption that AI will make companies more efficient. One measure of this efficiency is, among other things, the amount of staff needed. Efficiency has often indeed increased, but the problem is that it rose not because of AI, but because of a mix of offshoring, outsourcing, and changes in hiring practices.

Oracle is an example here. A major story was Oracle laying off as many as 30,000 people; what received less media attention is that the company very quickly hired back 8,000 of the people it had laid off, but through an intermediary and at a lower rate.

We should ask when and by how much valuations would need to be adjusted if we take into account that changes in companies’ employment are not the result of AI implementation. These companies still clearly need employees; only their practices and corporate policy are changing. This is more of a sidestep than a revolution.

Kamil Szczepański

Financial Market Analyst at XTB

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

SK Hynix earnings: Did market over-sold?

France Challenges Palantir, Market Reacts.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.